Vacant lots are both a problem and an opportunity. Every empty pad in your mobile home park is lost income — but filling those lots efficiently is one of the highest-return value-add activities available to operators who build the right partnerships.

Mobile home dealers — licensed businesses that source, sell, and install manufactured homes — are one of the fastest and most cost-effective tools for driving lot occupancy. For operators who invest in these relationships, the dealer channel can dramatically compress the timeline from vacant pad to paying resident.

Here’s a practical guide to making it work.

Why Vacant Lots Drag Down Returns More Than You Think

A vacant lot doesn’t sit harmlessly — it actively suppresses investment performance. Every unoccupied pad represents:

- Lost lot rent revenue — at $400–$700/month per lot, 10 vacant lots on a 100-site mobile home park costs $48,000–$84,000 in annual NOI

- Lower appraised value at exit — cap rate valuation punishes vacancy hard; fewer occupied lots means lower NOI, which compresses your sale price significantly

- Ongoing carrying costs — property taxes, insurance, and infrastructure maintenance on vacant pads continue regardless of occupancy

- Acquisition discount leverage — high vacancy is among the first factors buyers use to push your asking price down

This is why infill — filling vacant lots with new or pre-owned manufactured homes — consistently ranks near the top of mobile home park value-add business plans. Dealer partnerships are one of the most efficient infill channels available, particularly for operators who don’t want to carry home inventory on their own balance sheet.

For a broader look at how operators systematically increase mobile home park value, see our guide to 7 proven value-add strategies for mobile home park investors.

How the Mobile Home Dealer Model Works

Mobile home dealers are state-licensed businesses that buy, sell, and often install manufactured homes. The model is similar to automotive dealerships: they hold or source inventory, arrange financing for buyers through chattel lenders, and earn a margin on each sale.

In a dealer partnership with a mobile home park, the arrangement typically works as follows:

- The dealer sources new or pre-owned HUD-compliant manufactured homes appropriate for the park’s available lots

- The dealer markets homes to qualified buyers, sometimes with co-marketing support from the park operator

- Buyers purchase the home through the dealer — using chattel financing or cash — and execute a lot lease with the park

- Once the home is installed and the resident moves in, the park begins collecting monthly lot rent

The critical benefit for operators: the dealer carries the home inventory and financing risk. You provide the land and the lot lease opportunity. When the structure works well, vacant pads convert to revenue-generating lots without the park needing to purchase a single home — a capital-light path to NOI growth.

How to Find and Vet Mobile Home Dealers

Not all dealers make good partners. Here’s how to identify quality operators:

- Start with your state’s manufactured housing association — most states maintain active dealer directories. In North Carolina, the NC Manufactured Housing Institute is a strong starting point; in Tennessee, the Tennessee Manufactured Housing Association

- Ask other mobile home park operators in your market — experienced operators in your region will often refer dealers they’ve had success with, and will warn you off the ones they haven’t

- Verify state licensing — dealers must hold an active state license in most jurisdictions. Confirm current status through your state’s housing regulatory agency before entering any agreement

- Assess lender relationships — dealers with established relationships with 21st Mortgage, Triad Financial Services, or Cascade Financial will move buyers faster than those lacking chattel lending access

- Evaluate home sourcing capability — can they access new inventory from manufacturers like Clayton, Champion, or Skyline Homes? Pre-owned inventory? What’s their typical lead time from order to installation?

- Ask for references — speak directly with at least two mobile home park operators the dealer has worked with. Ask specifically about timelines, communication quality, home condition, and resident quality

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

What a Dealer Agreement Should Cover

Even informal dealer relationships need to be formalized in writing. A solid dealer agreement typically addresses:

- Home specifications — minimum age, size, and condition standards for homes placed in the park (e.g., no pre-1976 homes; minimum 14-foot width single-wide; no visible structural damage)

- Installation requirements — setup, skirting, anchoring, and tie-downs. In most arrangements, the dealer handles installation at their expense

- Park approval rights — the operator retains the unconditional right to approve or deny any prospective resident, completely separate from the dealer’s sale decision

- Timeline expectations — clear milestones for when a home must be placed and a resident moved in on a designated vacant lot

- No park financial obligation — in a true dealer partnership, the operator does not fund home inventory. The dealer carries that capital risk

- Buyer qualification floor — minimum income verification and background check thresholds for any buyer the dealer presents

Work with an attorney familiar with manufactured housing regulations in your state before executing any dealer agreement. If you’re operating in North Carolina or Tennessee, see our state-specific market guides for regulatory context: Mobile Home Park Investing in North Carolina and Mobile Home Park Investing in Tennessee.

Evaluating Dealer Infrastructure When Underwriting a Deal

If you’re buying a mobile home park with significant vacancy, the quality of the local dealer ecosystem is a material input to your value-add thesis. During due diligence, investigate:

- Are there licensed dealers actively operating within 30–50 miles of the property?

- Has the park worked with dealers previously? What were the timelines and outcomes?

- Is chattel financing accessible in this market? Tight lending availability is a frequently overlooked infill bottleneck

- Is there unmet housing demand nearby, or are competing communities operating at high vacancy?

- What’s a realistic per-lot fill timeline given local dealer capacity and buyer demand?

A mobile home park in an isolated rural area with no active dealer presence and limited chattel lending carries meaningfully more execution risk than one located near a growing metro with established dealer infrastructure. This is one reason experienced operators prioritize market quality in their underwriting — see our mobile home park underwriting guide for a full due diligence framework.

Common Mistakes Operators Make with Dealer Relationships

A few patterns that consistently undermine dealer partnerships:

- Surrendering resident approval authority — some dealers will push to streamline the process by bypassing your screening. This is non-negotiable: your right to approve residents is fundamental to managing your community and your liability

- Over-relying on a single dealer — the most effective operators maintain active relationships with 2–3 dealers in a market, creating competition and redundancy if one dealer goes quiet

- Neglecting lot readiness — dealers will deprioritize pads with drainage issues, damaged utility hookups, or access problems. Invest in lot preparation before engaging any dealer

- Focusing exclusively on new homes — pre-owned, HUD-compliant manufactured homes can fill lots just as effectively at lower price points that expand the available buyer pool considerably

- Treating dealer relationships as transactional — dealers who have a great experience at your park will prioritize sending buyers your way. Operators who communicate well and are easy to work with consistently get their lots filled first

What Passive Investors Should Ask Their Sponsor

If you’re evaluating a mobile home park syndication where the business plan includes significant infill, the sponsor’s dealer relationships are a key part of assessing execution credibility. Ask:

- Have you worked with dealers in this specific market before? Which dealers specifically?

- What’s the projected cost per lot filled and the timeline assumption in your underwriting model?

- What’s your contingency plan if dealer-driven infill runs behind schedule?

- Is chattel financing availability in this market confirmed through lender conversations, or assumed?

Sponsors who can answer these questions concretely — with specific dealer names, documented timelines, and contingency plans — demonstrate real operational depth. Business plans that project aggressive infill timelines without an established dealer pipeline are a yellow flag worth pressing on before committing capital.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Conclusion

Mobile home dealer partnerships are a proven but underutilized tool in the mobile home park operator’s playbook. When structured properly — with written agreements, retained resident approval rights, and active relationship management — they can compress lot-fill timelines from many months to just weeks and drive the NOI growth that builds park value at exit.

The operators who consistently outperform on infill treat dealer relationships as a long-term strategic asset. They invest time in finding the right partners, set clear expectations upfront, and show up as easy, reliable operators worth prioritizing. The result is a faster, more capital-efficient path to full occupancy — and a stronger return for everyone in the deal.

Get the top 20 lessons from two decades of mobile home park investing — free.

Frequently Asked Questions

Do I have to pay a mobile home dealer to place homes in my park?

In most dealer partnerships, the dealer earns their compensation through the margin on the home sale — the mobile home park operator doesn’t pay them directly. Some operators offer a one-time incentive such as the first month’s lot rent free to attract buyers. Any incentives should be modeled into your infill cost projections before committing to them.

What is the difference between a dealer partnership and a park-owned home (POH) strategy?

In a dealer partnership, the dealer owns the home inventory and carries the financing risk — the park operator provides the land and lot lease. With park-owned homes (POH), the park purchases the home and rents both the home and the lot. POH generates higher per-unit revenue but requires more capital upfront and more intensive day-to-day management. Dealer partnerships are generally lower-risk for operators new to infill or working in markets with limited capital availability.

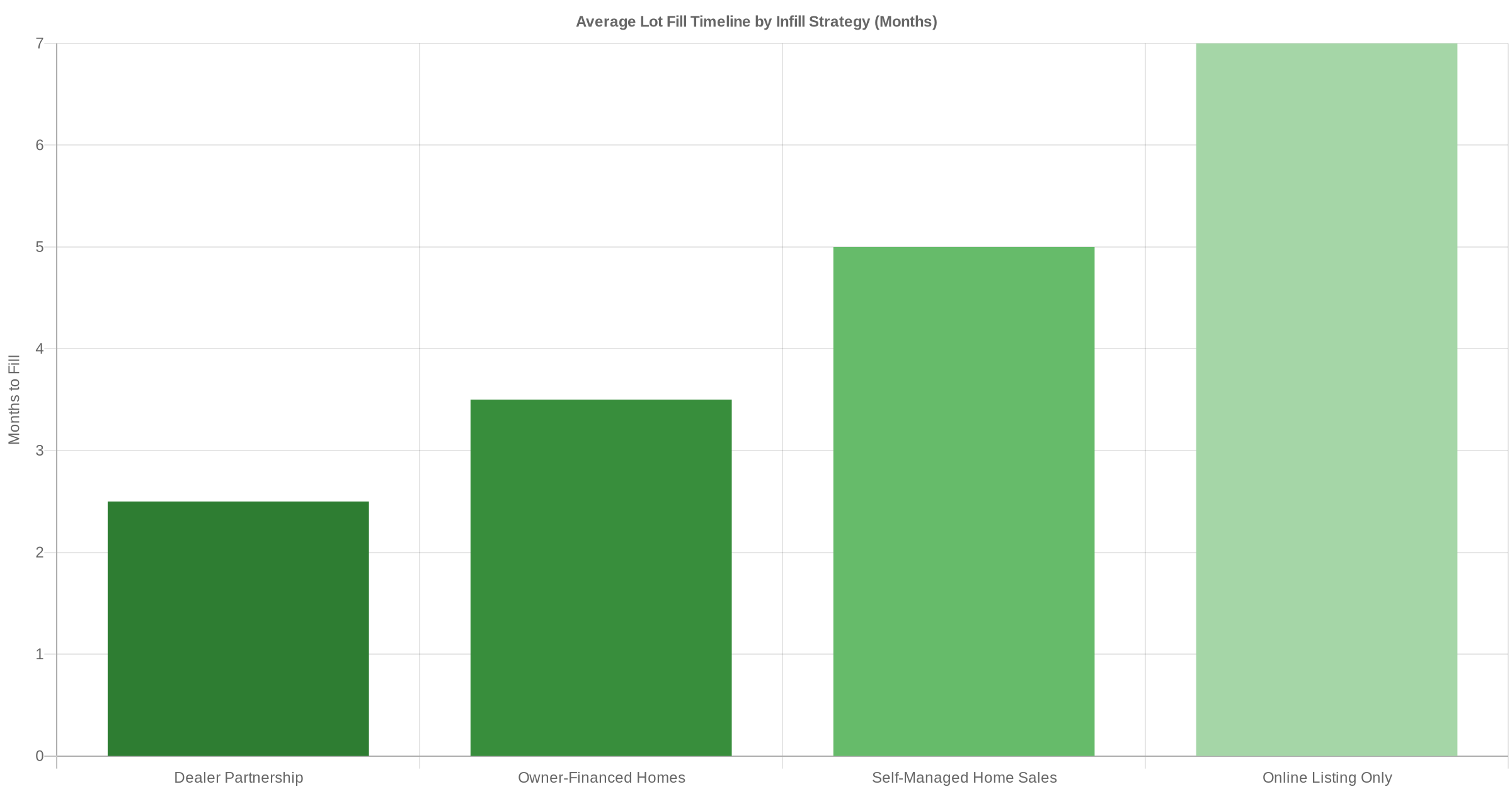

How long does it typically take to fill a vacant lot through a dealer partnership?

In established markets with strong dealer infrastructure, experienced operators typically target 60–120 days from engagement to move-in. In markets with limited dealer activity or constrained chattel lending, timelines can extend to 6–12 months per lot. Conservative underwriting should model the slower end of the range unless you have specific dealer commitments in place before closing.

Can I use dealer partnerships in North Carolina and Tennessee?

Yes — both states have active manufactured housing dealer communities and relatively strong chattel lending environments. North Carolina and Tennessee are among the stronger markets for manufactured housing demand nationally, supported by population growth and significant affordability pressures. Always verify any dealer’s active license status before signing an agreement, as state licensing requirements are enforced.

What happens if a dealer’s buyer doesn’t pass my resident screening?

This is exactly why maintaining unconditional resident approval rights in your dealer agreement is non-negotiable. If a buyer doesn’t meet your income, background, or reference standards, you decline their residency application — and the dealer must find a different buyer for the home. A well-structured agreement makes this clear from the start, so there’s no ambiguity when it happens.