If you’re evaluating a mobile home park syndication as a passive investor, the numbers you’ll spend the most time analyzing aren’t cap rates or occupancy — they’re the fees. How a sponsor gets paid shapes the entire risk/return profile of the deal. Understand the mobile home park syndication fee structure and you’ll know instantly whether a deal is structured fairly — or built to benefit the sponsor at your expense.

This guide breaks down every major compensation layer: how each fee works, what’s typical, and what should raise a red flag before you commit capital.

Why Sponsor Fees Matter for Passive Investors

In a mobile home park syndication, the sponsor (also called the general partner, or GP) does the heavy lifting: finding the deal, securing financing, managing the asset, and executing the business plan. In exchange, they receive compensation at multiple points throughout the deal lifecycle.

That compensation is fine — expected, even. The question is whether the structure is aligned with investor success or with sponsor extraction. A well-structured deal rewards the sponsor for performance. A poorly structured one pays the sponsor regardless of whether investors make money.

Understanding the difference is one of the most important skills a passive investor can develop. We’ve seen deals where fee layers quietly consumed 4–6% of equity value before the first distribution was ever paid. That’s not necessarily predatory — but you need to know what you’re agreeing to before you wire funds.

The Four Core Sponsor Compensation Layers

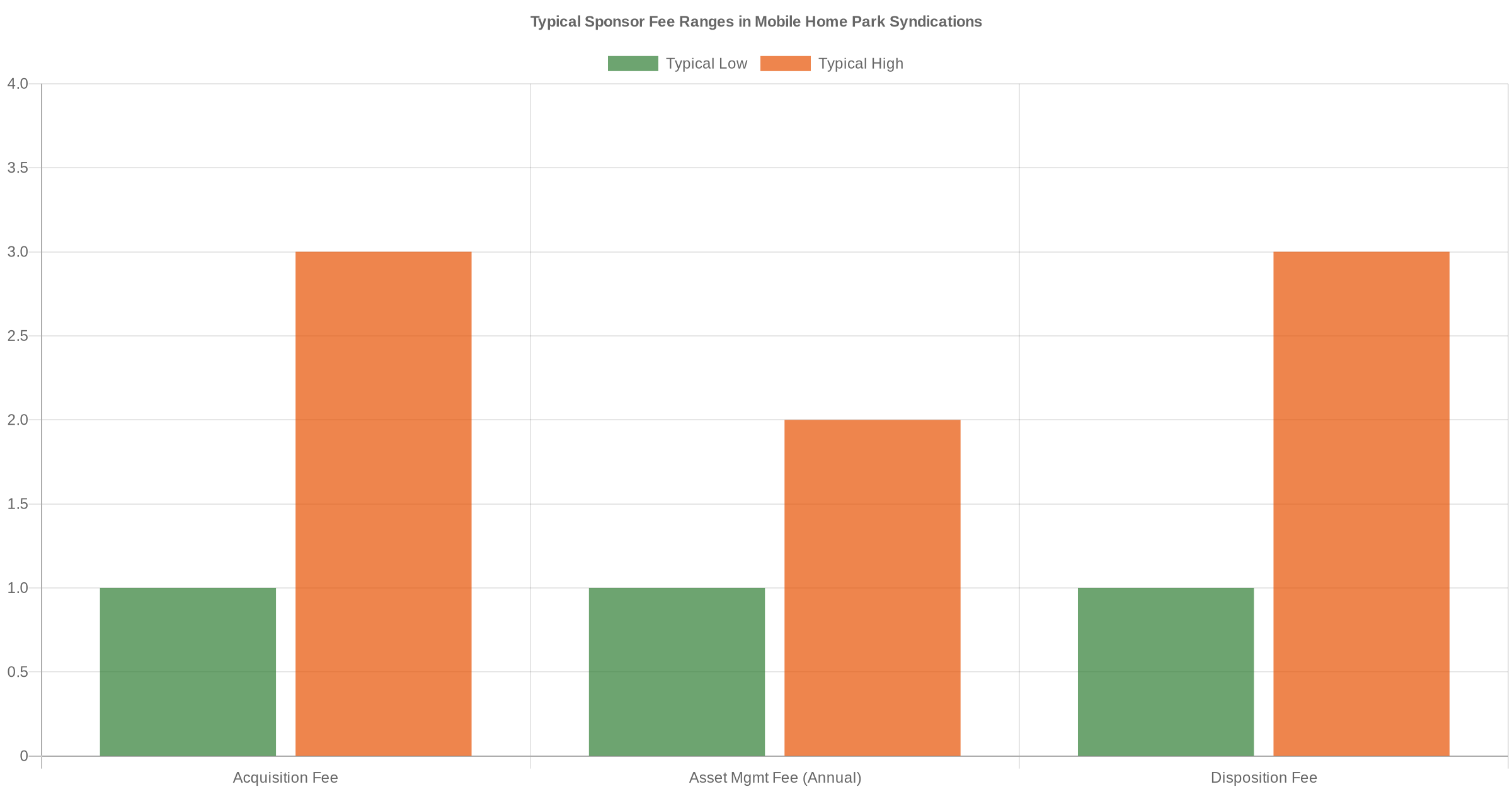

1. Acquisition Fee

The acquisition fee is paid at closing and compensates the sponsor for sourcing the deal, conducting due diligence, negotiating the purchase, and arranging financing. It’s typically expressed as a percentage of the total purchase price.

- Typical range: 1% to 3% of the purchase price

- On a $5M deal: $50,000 to $150,000

- When it’s paid: At or near closing, from equity raised

A 1–2% acquisition fee is standard and reasonable. At 3%, it’s on the high end but acceptable if the sponsor is bringing exceptional deal flow or deal complexity. Above 3% is worth questioning — especially on larger deals where the absolute dollar amount becomes significant.

Some sponsors also charge a separate loan origination or financing fee (typically 0.5% to 1% of the loan amount). Make sure you’re reading the PPM carefully enough to catch both. For more on navigating deal documents, see our guide on how to read a mobile home park syndication PPM.

2. Asset Management Fee

The asset management fee is an ongoing annual fee paid to the sponsor for overseeing the investment — managing the property management company, executing the business plan, handling investor relations, and making operational decisions.

- Typical range: 1% to 2% of gross revenue (or sometimes of equity raised)

- On a $400,000/year gross revenue mobile home park: $4,000 to $8,000/year

- How it’s paid: Monthly or quarterly from operating cash flow

Watch for asset management fees calculated on equity raised rather than gross revenue. On a deal that underperforms, equity-based fees can be higher than revenue-based fees — meaning the sponsor gets paid even when the mobile home park is struggling. Revenue-based fees are generally more aligned with investor outcomes.

3. Disposition Fee

The disposition fee (also called a sales fee) is paid when the asset is sold, and compensates the sponsor for managing the exit process — hiring a broker, negotiating the sale, and overseeing closing.

- Typical range: 1% to 3% of the sale price

- On a $7M exit: $70,000 to $210,000

- When it’s paid: At closing of the sale

Not every mobile home park syndication includes a disposition fee, and some sponsors waive it in exchange for a larger profit split. When it is included, verify that it doesn’t come out of gross proceeds before the preferred return is calculated — that sequencing matters significantly for your net return.

4. The Profit Split (Equity Waterfall)

After all fees are paid and investors receive their preferred return, remaining profits are split between LPs and the GP. This split is where sponsors can earn their most significant upside — and where the structure either aligns or diverges from investor interests.

- Typical GP share: 20% to 30% of profits after preferred return

- Typical LP share: 70% to 80%

- With hurdles: Some deals include tiered splits — e.g., 80/20 until a 2x equity multiple, then 70/30 on returns above that threshold

The most investor-friendly structures include a preferred return (typically 6–8% annually) that must be paid in full before any profit split begins. The promoted interest — the GP’s share of upside — is the reward for performance. For a deep dive on how the math works at each stage, see our article on waterfall structures in real estate syndication.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

What a Reasonable Fee Structure Looks Like

Putting it all together, here’s what a well-structured mobile home park syndication typically looks like on the compensation side:

- Acquisition fee: 1–2%

- Asset management fee: 1–1.5% of gross revenue annually

- Disposition fee: 1–2% (or waived)

- Preferred return: 6–8% annually before profit split

- Profit split: 70/30 to 80/20 (LP/GP) on gains above preferred return

A deal hitting all five of those marks is set up fairly. The sponsor is incentivized to grow the asset because the majority of their upside comes from performance — not from fees extracted along the way.

Fee Structures That Should Give You Pause

Not every unusual fee structure is a red flag — but some combinations should prompt serious questions before you commit:

- Asset management fees on equity raised, not revenue. This decouples the sponsor’s income from mobile home park performance.

- No preferred return. If there’s no priority payout to investors before the GP participates in profits, the structure doesn’t reward performance — it just rewards being in the deal.

- GP promote above 30%. At 35% or higher, ask what’s justifying it. Experience and track record matter, but even exceptional sponsors rarely push above 30%.

- Multiple fee layers with no cap. An acquisition fee plus a loan fee plus a construction management fee plus a disposition fee can stack quickly. Add them all up and compare to total equity raised.

- Fees paid before preferred return is current. In some PPMs, asset management fees are treated as a priority over investor preferred returns. That’s a sign of a misaligned structure.

For a more detailed breakdown of warning signs, see our post on mobile home park syndication red flags.

How to Evaluate Fees in the Context of the Full Deal

Fees don’t exist in isolation — they need to be evaluated against the deal’s projected returns. A sponsor charging a 2% acquisition fee and 1.5% asset management fee on a deal projecting an 18% IRR is a different conversation than those same fees on a deal projecting 10% IRR.

Here’s a practical checklist for evaluating sponsor compensation before you sign:

- List every fee mentioned in the PPM and calculate the total dollar amount

- Calculate total fees as a percentage of equity raised

- Confirm how the waterfall is sequenced — fees first? preferred return first?

- Understand whether the GP has meaningful personal equity invested alongside LPs

- Ask what the GP earns if the deal returns exactly the preferred return and nothing more

That last question is often the most revealing. A good sponsor should be able to walk you through their compensation at multiple return scenarios. If they can’t — or won’t — that tells you something important about how they think about their relationship with investors. For guidance on evaluating operators more broadly, see how to evaluate a mobile home park operator before you invest.

One More Thing: Does the GP Have Skin in the Game?

The cleanest alignment signal in any mobile home park syndication is co-investment: does the GP have their own money in the deal? Sponsors who invest alongside LPs have personal skin in the game. Their fees become secondary to making the asset perform — because they’re also a limited partner in their own deal.

Not all sponsors co-invest, and that alone isn’t disqualifying. But when a sponsor charges acquisition, management, and disposition fees while declining to put personal capital in — that’s worth noting in your analysis. It doesn’t make the deal bad. It does change the incentive math.

Conclusion

Mobile home park syndication fees aren’t the enemy — they’re the cost of accessing deals you couldn’t otherwise source, underwrite, or operate. What matters is whether the structure is transparent, reasonable in total, and aligned with investor success at every stage.

Read the PPM carefully. Add up the total fee load. Understand the waterfall. And ask every question you have before you commit capital — that’s exactly what the sponsor relationship is built for.

For a complete guide to passive mobile home park investing, visit our mobile home park syndication overview.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.