Mobile home park syndications have attracted a growing wave of passive investors seeking inflation-resistant cash flow and recession-resilient returns. But not every syndication is worth your capital — and the difference between a quality deal and a costly mistake often comes down to recognizing the warning signs early. Knowing the key mobile home park syndication red flags before you wire funds can save you from years of frustration and potential loss.

This guide breaks down seven warning signs that should give any investor pause — along with what good operator behavior actually looks like.

Why the Operator Matters More Than the Deal

In mobile home park syndication, the deal matters — but the operator matters more. You can find a well-located park with strong occupancy, but if the person running the show lacks experience, transparency, or integrity, the investment can unravel quickly. A seasoned operator can turn a mediocre deal into a winner. An inexperienced or dishonest operator can torch a great one.

Before evaluating any specific offering, it’s worth understanding how to evaluate a mobile home park operator in depth. The seven red flags below build directly on that foundation.

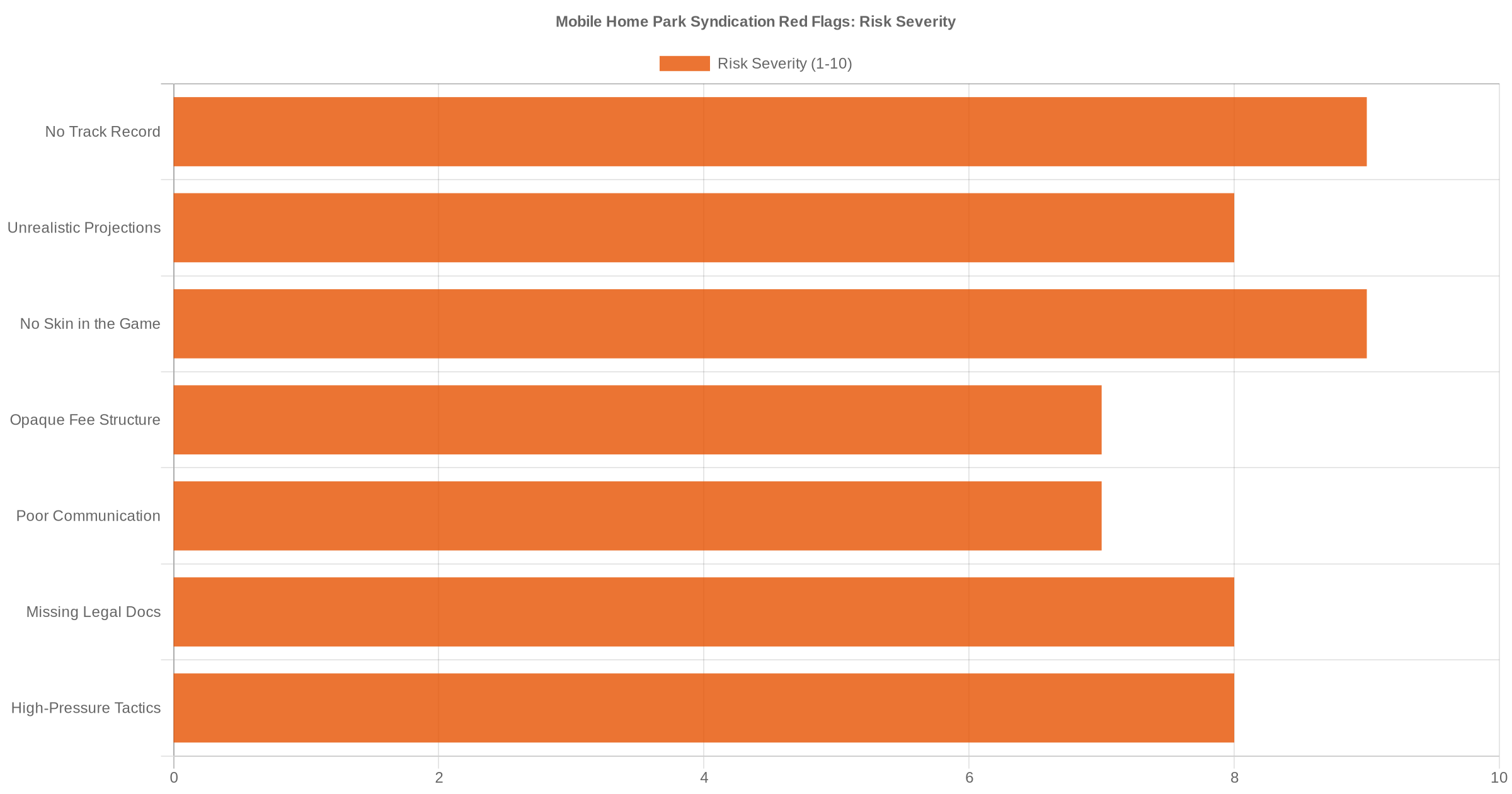

Red Flag #1: No Track Record or Vague Deal History

Experience in mobile home park operations is hard to fake over time. If an operator can’t point to specific parks they’ve acquired, managed, and either held or exited — with concrete performance data — that’s a serious concern.

Key questions to ask:

- How many mobile home parks have you acquired?

- What were the entry and exit cap rates on your last three deals?

- Can you share actual investor returns from prior syndications — not projections?

Vague answers, missing performance data, or pivoting from a completely different asset class with no mobile home park-specific history are all warning signs. First deals happen — but if an operator is raising from passive investors on their very first mobile home park, that risk should be clearly disclosed and priced accordingly.

Red Flag #2: Projections That Look Too Good

Every sponsor has an incentive to present optimistic numbers. But projections that assume aggressive rent growth, rapid lot infill, and minimal capital expenditure — without clear market data to support those assumptions — suggest underwriting that isn’t grounded in reality.

Watch for:

- Projected lot rent increases of 15–20%+ per year with no comparable market evidence

- Assumptions that all vacant lots will fill within 12 months in a thin housing supply market

- Near-zero expense ratios on an older, distressed mobile home park

- Exit cap rates that are materially lower than entry cap rates without a clear thesis

Conservative underwriting is a sign of discipline. Overly optimistic projections often reflect inexperience — or a deliberate effort to attract capital by showing numbers investors want to see.

Red Flag #3: No Skin in the Game

Alignment of interest is the foundation of any strong partnership. If the operator isn’t investing meaningful personal capital alongside limited partners, their incentives aren’t fully aligned with yours.

Ask directly: How much of your own money is going into this deal? A credible operator should be able to answer clearly and without hesitation. If they’re relying entirely on limited partner capital — with no personal equity at risk — that disconnect is worth exploring carefully before you commit.

Red Flag #4: Opaque or Complicated Fee Structures

Legitimate mobile home park syndications have fees — acquisition fees, asset management fees, disposition fees are all standard. But they should be clearly disclosed and proportionate. Red flags include:

- Multiple layers of fees that add up to 10%+ of invested capital before returns are calculated

- Fees that aren’t disclosed upfront and only surface deep in the PPM

- Complex waterfall structures that make it difficult to model your actual net return

If you’re reading the offering documents and the fee structure isn’t clear after two careful readings, that’s a problem with the document — not your reading comprehension. Understand how waterfall structures work in real estate syndication before you evaluate any deal.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Red Flag #5: Poor Communication Before the Deal Closes

How an operator communicates during the fundraising period tells you exactly how they’ll communicate when things get hard mid-hold. If they’re slow to respond to basic questions, vague in their answers, or dismissive of due diligence requests — those patterns don’t improve after you’ve committed capital.

A quality operator is proactive, specific, and genuinely comfortable with hard questions. They expect investors to do real due diligence, and they welcome it. Be cautious of operators who frame investor questions as obstacles rather than a normal part of the process.

Red Flag #6: Thin or Missing Legal Documentation

A legitimate mobile home park syndication raises capital under SEC Regulation D — either 506(b) or 506(c). That means there should be a Private Placement Memorandum (PPM), an Operating Agreement, and a Subscription Agreement. If any of these are missing, incomplete, or “still being prepared” while the offering is actively open, walk away.

The PPM is your legal protection document. It discloses risks, use of proceeds, operator compensation, and investor rights. You should know how to read a mobile home park syndication PPM before investing in any deal. Also understand the difference between 506(b) and 506(c) syndications — those rules determine who can participate and how the offering can be marketed.

Red Flag #7: Pressure to Invest Quickly

Artificial urgency is a classic tactic used to short-circuit due diligence. Legitimate operators don’t pressure investors to commit before they’ve had time to review documents, ask questions, and consult their advisors.

Phrases like “we’re closing this week,” “only two spots left,” or “we can’t hold your allocation past Friday” — especially early in the process — should raise your antenna. A deal worth doing will still be worth doing after you’ve done your homework. And if the deadline is real, a trustworthy operator will respect your need for adequate review time or work with you on it.

What Good Looks Like

The best mobile home park operators are transparent, responsive, and disciplined. When you find one, they typically:

- Share detailed, auditable performance data across prior deals — including deals that underperformed

- Present conservative underwriting with clearly sourced market comparables

- Invest meaningful personal capital alongside limited partner investors

- Disclose all fees upfront in plain language before you ask

- Provide complete legal documentation well before accepting capital commitments

- Welcome investor questions and never manufacture urgency

A strong syndication relationship is built on trust — and trust is earned through consistent, transparent behavior well before any capital changes hands. If an operator clears all seven of these filters, that’s a meaningful signal that they’ve done this before and intend to do it again.

Bottom Line

Mobile home park investing has real merit — recession resilience, affordable housing tailwinds, and strong cash flow characteristics make it one of the more compelling asset classes in private real estate. But those merits don’t protect you from a poorly-run syndication. They protect you when the operator actually knows what they’re doing.

Use this list methodically when evaluating any offering. Don’t let a polished pitch deck or a slick website substitute for substantive, direct answers to your questions. And always review all legal documents with a qualified advisor before committing capital.

For a deeper look at how passive investments in this asset class are structured, visit our complete guide to mobile home park syndication.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.