When most investors evaluate a mobile home park, they focus on lot rents, occupancy, and cap rates. Zoning rarely tops the checklist — until it causes a deal to fall apart at closing, or worse, after you own it.

Mobile home park zoning determines whether the park is legally permitted to operate, whether you can expand it, and what happens if a significant portion is destroyed. Getting clarity on zoning before you buy isn’t optional. It’s one of the most important steps in evaluating a mobile home park investment.

Here’s what every investor needs to understand.

What Is Mobile Home Park Zoning?

Zoning is a local government’s way of regulating how land can be used. Each parcel of land is assigned a zoning designation that dictates what can be built on it, how many units can exist, what setbacks apply, and whether a particular use is permitted at all.

For mobile home parks, the relevant question is: does this jurisdiction allow a mobile home park to legally operate on this parcel? The answer falls into a few distinct categories, each carrying very different implications for investors.

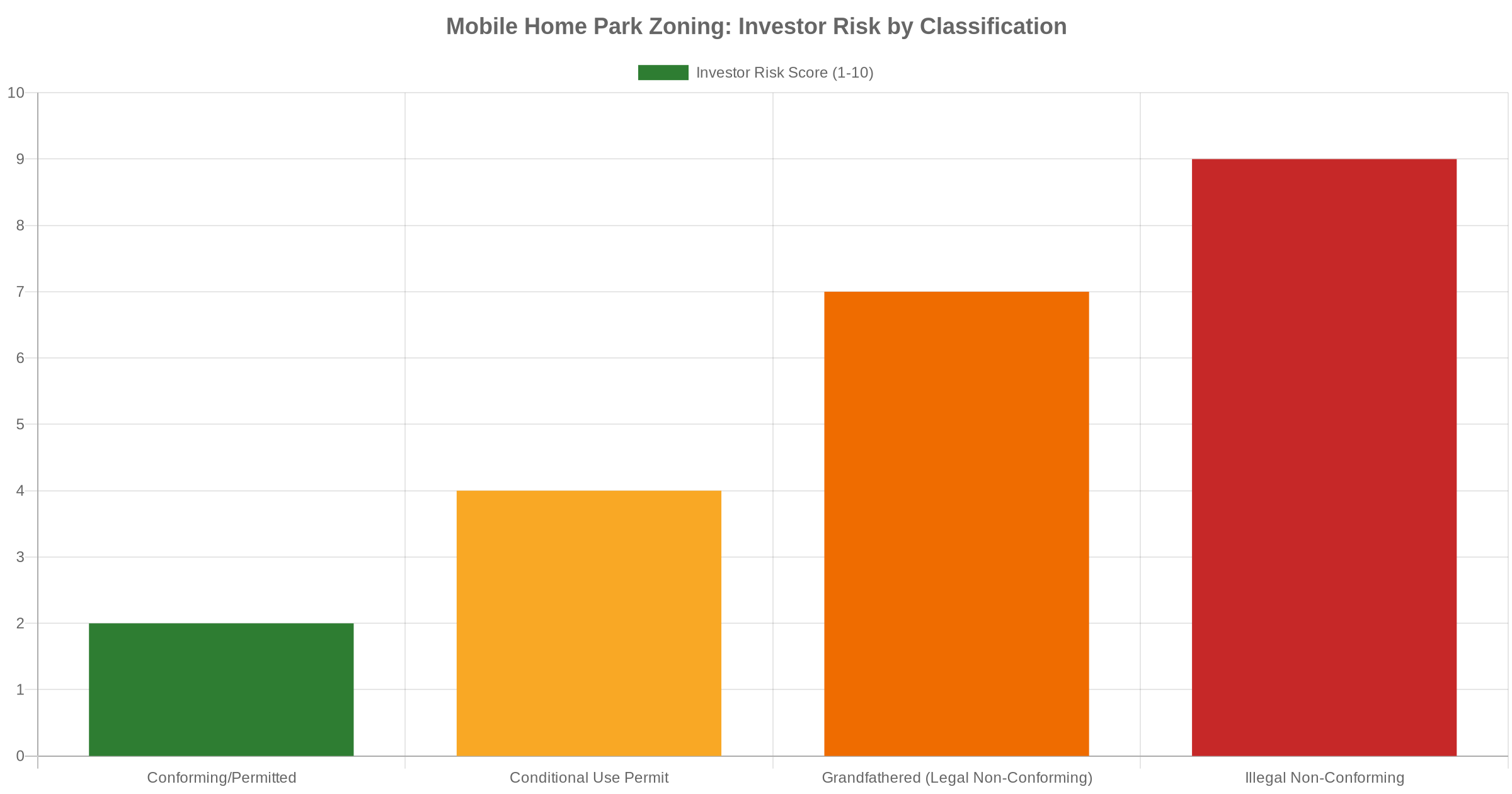

Common Zoning Classifications for Mobile Home Parks

Not all zoning is created equal. When you’re evaluating a mobile home park, you’ll typically encounter one of these four situations:

1. Conforming / Permitted Use

The park is located in a zone that explicitly allows mobile home parks or manufactured housing communities — by right. No special approval is needed for it to operate. This is the cleanest scenario and should be the baseline expectation for any serious acquisition.

2. Conditional Use Permit (CUP)

The zoning code allows mobile home parks in this zone, but only with a conditional use permit that was approved at some point in the past. This is common and generally fine — as long as the CUP is valid, transferable, and not tied to specific ownership. Review the permit carefully. Some CUPs have expiration dates or compliance conditions.

3. Grandfathered / Legal Non-Conforming Use

The park was established before current zoning rules took effect. Under the old rules it was permitted; under today’s rules it technically is not — but it’s allowed to continue operating because it predates the change. This is called legal non-conforming use, and it’s far more common than most buyers realize.

The risk: if a significant portion of the park is destroyed (by fire, tornado, or flood), the municipality may not allow you to rebuild — because new construction would trigger current zoning requirements. In most jurisdictions, this threshold is 50% or more of the structure value. Some states have passed legislation protecting manufactured housing communities from this type of discontinuation, but many have not.

4. Illegal Non-Conforming Use

This is the red-flag scenario. The park is operating without proper zoning authorization and has no legal protection as a grandfathered use. This can happen when zoning changes occur and the owner never obtained updated permits — or when the park was established improperly from the start. Walk away unless you have extraordinary leverage and an airtight legal strategy.

Why Zoning Status Is Critical to Your Investment

Here’s where zoning directly affects your bottom line:

- Lender requirements: Conventional and agency lenders will require a zoning verification letter as part of their underwriting. A legal non-conforming designation can limit your financing options or require additional reserves.

- Insurance coverage: Some insurers reduce coverage or exclude rebuilding costs if the park is non-conforming — on the assumption that a rebuild wouldn’t be permitted anyway. Ask your insurer directly about their non-conforming use policy.

- Exit and resale: A park with clean conforming zoning is easier to sell, easier to finance, and commands a better multiple. Non-conforming status creates a discount that’s hard to eliminate.

- Value-add limitations: If you want to add lots, bring in new homes, or build amenities, zoning determines what’s possible. A non-conforming park may not be expandable at all.

For a full breakdown of what to evaluate before making an offer, see our complete guide to investing in mobile home parks.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

How to Verify Zoning Before You Buy

Don’t rely on the seller’s word or an old survey. Zoning codes change, and sellers don’t always know their park’s legal status. Here’s how to verify it yourself:

- Contact the local planning or zoning department. Call or visit the county or municipal planning office and ask directly: “Is this parcel currently zoned for mobile home park or manufactured housing community use?” Get the answer in writing if you can.

- Request a zoning verification letter. This is a formal written confirmation of the current zoning designation. Many lenders require it, and it protects you legally. Costs $25–$150 in most jurisdictions.

- Pull the current zoning map. Most counties publish their GIS zoning maps online. Cross-reference the parcel address against the current designation.

- Check the zoning ordinance text. Even if the parcel is in the right zone, the ordinance may have restrictions on density, setbacks, or age of homes that affect your plans. Read the code, not just the map.

- Research the history. If the park is non-conforming, find out when the zoning changed and whether any local ordinance protects the existing use. Some states have strong preemption laws that protect manufactured housing communities from municipal elimination.

This fits naturally into the broader mobile home park due diligence checklist every buyer should complete before closing.

Zoning and Your Expansion Plans

If part of your value-add strategy involves adding lots, bringing in new homes, or building a community center, zoning approval may be required before you can break ground. A conforming mobile home park in a mobile home park-friendly zone may allow expansion by right — or may require a separate site plan review. A non-conforming park likely cannot expand at all.

Ask the planning department specifically: “If we wanted to add 10 lots to the existing park, what approvals would be required?” The answer will tell you a lot about the municipality’s posture toward manufactured housing in general.

Red Flags in Zoning Due Diligence

Watch out for these warning signs when reviewing a mobile home park’s zoning status:

- Seller doesn’t know the zoning designation — suggests the park hasn’t been managed with any institutional rigor

- Zoning changed in the last 10–15 years — especially from MH to residential or commercial; non-conforming risk is highest here

- No rebuilding protection in state law — a 50% destruction rule without statutory protection is a real risk in storm-prone markets

- Conditional use permit with unusual conditions — e.g., capped at current number of lots, restricted to 55+ residents only, or tied to a specific owner/operator

- Municipality with a history of hostility toward mobile home parks — public meeting records and local news can reveal a lot about how the planning department views manufactured housing

If zoning turns out to be a problem, it doesn’t always mean walking away — but it absolutely should be reflected in the price. See what to look for in your first mobile home park investment for how to weight these risk factors during underwriting.

Zoning in Key Markets: NC, TN, GA, and SC

State-level context matters. Here’s a brief overview of the regulatory environment in four active mobile home park investment markets:

- North Carolina: NC passed the Mobile Home Park Act (SB 518) in 2024, giving residents certain protections and codifying park operations. Zoning is handled at the county level and varies significantly — some Piedmont counties are more restrictive than rural eastern counties.

- Tennessee: Tennessee is generally landlord-friendly with fewer municipal restrictions on manufactured housing. Many rural counties have limited zoning altogether, which can simplify the approval picture considerably.

- Georgia: Georgia municipalities vary widely. Metro Atlanta counties have increasingly complex zoning requirements; rural counties in middle and south Georgia remain more permissive toward manufactured housing communities.

- South Carolina: SC has a mix of coastal counties with strict zoning and inland rural counties with more flexibility. Always verify at the county level before assuming a favorable environment.

If you’re evaluating deals in any of these states, local legal counsel who specializes in land use is worth the investment.

Conclusion

Mobile home park zoning is one of the most overlooked risk factors in deal evaluation — and one of the most consequential. A non-conforming park can limit your financing options, cap your expansion plans, and expose you to rebuilding risk that most investors never price in.

The fix is simple: verify zoning early in due diligence, get it in writing, and understand exactly what the local code says about rebuilding, expansion, and use continuation. This is non-negotiable due diligence for any serious mobile home park buyer.

Want to learn how to finance your next mobile home park acquisition? See how to finance a mobile home park: loan options explained.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.