Buying your first mobile home park is one of the most consequential real estate decisions you’ll ever make. Unlike single-family homes or apartment buildings, mobile home parks operate by an entirely different set of rules. Get it right, and you’ve got a cash-flowing asset with remarkably low tenant turnover, a landlord-favorable dynamic, and inflation-resistant rent income. Get it wrong, and you’re staring down private utility nightmares, deferred infrastructure, and a market too illiquid to exit cleanly.

The good news? Most of the landmines are findable before you close — if you know what to look for. This guide covers what experienced mobile home park investors evaluate on every deal, and what you should be scrutinizing on your first one. If you’re just beginning your research into how to invest in mobile home parks, this is a solid place to start.

1. Location: The Market Behind the Market

Mobile home park investing begins with location — but not in the same way as residential real estate. You’re not just looking for a nice neighborhood. You’re looking for a market with the right economic fundamentals: stable employment, population growth, and genuine demand for workforce housing.

The sweet spot for most mobile home park investors is a park located within one hour of a major metro area with at least 100,000 residents. This gives you a broad enough labor pool to attract and retain tenants while keeping acquisition prices at more reasonable levels compared to the urban core.

Avoid markets with significant population decline, major employer exits, or heavy oversupply of competing manufactured housing communities. A mobile home park in a shrinking town is a hard asset to turn around and an even harder one to sell.

2. Lot Count and Occupancy Rate

Scale matters in mobile home park investing. Most experienced buyers target parks with at least 50 lots, and ideally 70 or more. Here’s the math: fixed operating costs — management fees, insurance, property taxes, accounting — don’t scale down proportionally with lot count. A 30-lot park carries similar overhead to an 80-lot park but generates far less revenue to absorb it.

Occupancy is equally critical. A park at 50% occupancy may look cheap on paper, but filling vacant lots is expensive and time-consuming. You’ll need to source homes, set them up, find tenants, and often offer move-in incentives to attract residents. Budget conservatively for lease-up costs before counting vacant lots as near-term income.

For your first mobile home park, target properties that are at least 70–80% occupied. You’ll sleep better at night, and your lender will be more comfortable too.

3. City Water and Sewer — Non-Negotiable for Most First-Time Buyers

If there’s one rule of thumb that experienced mobile home park investors consistently agree on, it’s this: stick to city water and city sewer. Private utilities — wells, septic systems, lagoons, and wastewater treatment plants — introduce operating complexity, regulatory risk, and capital expenditure that most operators are not equipped to manage.

A leaking lagoon can cost hundreds of thousands of dollars to remediate. A failing well can trigger health code violations and tenant displacement. These aren’t edge cases — they’re among the most common sources of catastrophic outcomes in mobile home park deals.

City water and sewer means you’re essentially a landlord collecting lot rent, not a utility operator managing infrastructure. That’s the business you want to be in — especially on your first deal.

4. The Lot Rent Spread: Room to Grow

One of the most powerful value drivers in mobile home park investing is below-market lot rent. If the current owner is charging $225 per month in a market where comparable mobile home parks charge $375–425 per month, that spread represents latent value you can unlock over time through modest, annual rent increases.

Before you underwrite any deal, pull lot rent comparables from other mobile home parks in the same market. Call neighboring parks. Check local listings. If the subject property is already at market rate, you’ll need to find value elsewhere — through infill, expense reduction, or operational improvements.

A mobile home park with significant rent upside is often worth paying a modest premium for, because that rent growth is repeatable, compounding, and reflected directly in your net operating income and eventual exit cap rate.

📋 The MHP Due Diligence Playbook — 10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal. Get the Playbook →

5. Park-Owned vs. Tenant-Owned Homes

The composition of your mobile home park — how many homes are owned by tenants versus owned by the park itself — has a major impact on your operating model and risk profile.

Tenant-owned homes are the gold standard. The tenant owns their home outright and rents only the land beneath it. This creates a sticky tenancy: moving a manufactured home costs $3,000–$10,000 or more, so residents rarely leave voluntarily. Your turnover is minimal and your cash flow is predictable month over month.

Park-owned homes put you in the landlord business — responsible for maintenance, repairs, and unit turnover. This adds operational complexity and capital exposure. That said, park-owned homes can represent an opportunity: if you can convert them to tenant ownership over time (through rent-to-own programs or direct sales), you reduce your operating burden while potentially capturing a lump-sum payment.

For your first mobile home park, a property with 80% or more tenant-owned homes is generally lower-risk and significantly easier to manage.

6. The Income and Expense Story

Mobile home parks are valued on net operating income using cap rates. That means every dollar of verified NOI translates directly into appraised value. Before you trust the seller’s numbers, rebuild the income and expense statement from scratch using primary source documents.

On the income side, verify every lot that’s actually paying rent. Request 12 months of bank statements. Look for seasonal patterns, delinquency trends, and any one-time income items that shouldn’t be annualized in your pro forma.

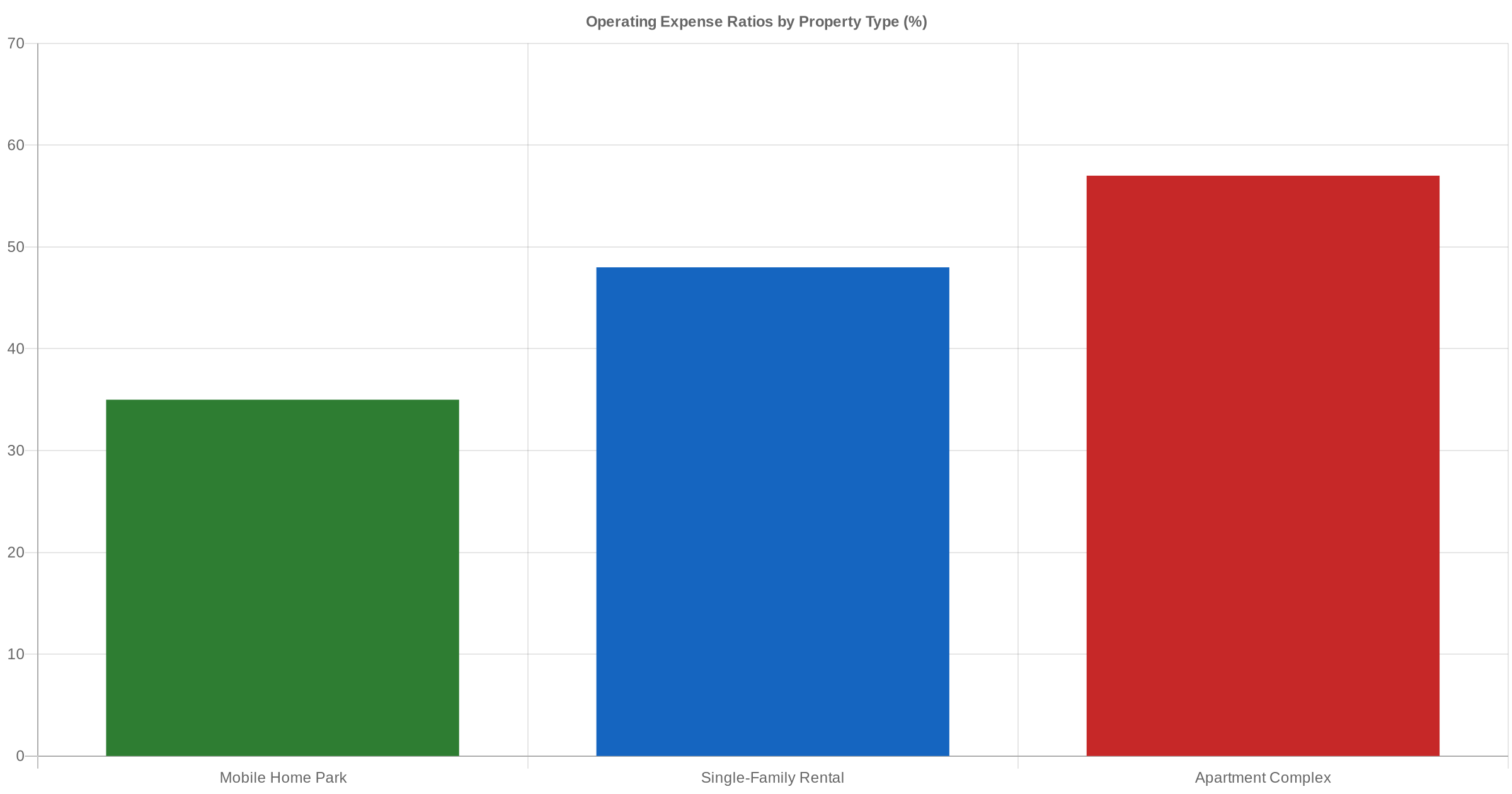

On the expense side, watch for what’s missing. Sellers commonly omit or understate management fees, capital expenditure reserves, and property tax estimates (especially if the park was recently purchased and hasn’t yet been reassessed at the new value). A realistic expense ratio for a well-run mobile home park is typically 30–45% of gross income, depending on utility structure and management arrangement.

For a detailed walkthrough of the underwriting process, see our guide on mobile home park underwriting 101.

7. Management and Infrastructure Condition

Before you close on your first mobile home park, walk every road, inspect every utility pedestal, and document every visible deferred maintenance item. The cost of aging infrastructure — roads, electrical pedestals, water and sewer lines — can be substantial and is often not reflected in the asking price.

Equally important: assess how the park has been managed. A self-managed mom-and-pop operation may have informal lease agreements, minimal documentation, and tenants who have never been asked to comply with a written community policy. Transitioning to professional management is absolutely doable, but expect 6–12 months of operational adjustment before collections and compliance stabilize.

Always budget for a professional property condition assessment before closing. It typically costs $1,500–$4,000 and can surface issues that reshape your offer price or deal structure entirely. Consider it inexpensive insurance.

8. How to Find Your First Mobile Home Park

The best mobile home park deals rarely appear on the open market. They’re sourced through direct outreach — letters, cold calls, and relationships built directly with park owners over time. Experienced buyers spend months cultivating deal pipelines before a transaction comes together.

If you’re just getting started, broker networks, state associations, and targeted direct mail campaigns can help you identify potential sellers. You’ll also want to think carefully about how much capital you actually need before you start making offers. Our guide on finding off-market mobile home parks covers the most effective sourcing strategies in depth.

First Mobile Home Park Investment: Quick Checklist

- ✅ City water and city sewer confirmed (no private utilities)

- ✅ 50+ lots minimum (70+ strongly preferred)

- ✅ 70%+ current occupancy

- ✅ Located within 1 hour of a 100,000+ population metro area

- ✅ Lot rent below market (meaningful upside available)

- ✅ 75%+ tenant-owned homes

- ✅ 12 months of bank statements reviewed and verified

- ✅ Roads and utility infrastructure physically inspected

- ✅ Professional property condition assessment ordered

- ✅ Phase I environmental assessment completed

- ✅ All leases reviewed for enforceability

- ✅ Zoning confirmed as mobile home park use

The Bottom Line

Your first mobile home park investment sets the tone for everything that follows. Buy a clean, well-located park with city utilities, below-market rents, strong tenant ownership, and a healthy occupancy rate, and you’ve built a foundation for years of stable, growing cash flow. Cut corners on any one of those criteria, and you’re taking on risk that may not show up in your pro forma — but will absolutely show up in your operations.

Take your time. Do the work. And if you’re considering passive exposure to mobile home park investing before taking the operator leap, reach out and we’d be happy to have a conversation.

📋 Ready to Evaluate Your Next Deal? Get the MHP Due Diligence Playbook — the complete system for analyzing mobile home park acquisitions with confidence. 10 video modules, a 55-page checklist, and 9 ready-to-use templates. Everything you need to move from curious to confident.