There is a single question that separates mobile home park investors who consistently generate returns from those who constantly fight fires: how many of the homes in this park does the operator actually own?

The park-owned home versus tenant-owned home distinction is not a minor operational detail. It defines your maintenance exposure, your lender options, your income quality, your management complexity, and ultimately your cap rate at resale. Yet many first-time mobile home park buyers underestimate it, or treat it as a secondary concern behind occupancy and lot rent.

This post breaks down the real economics — with actual numbers — so you understand exactly what you are buying into.

The Fundamental Difference: What Each Model Actually Means

In a tenant-owned home (TOH) community, the resident owns their manufactured home outright. They pay you lot rent — typically $400–$750 per month in most Southeast and Midwest markets — and you provide the land, utilities infrastructure, and community amenities. The home itself is their asset. Their maintenance problem.

In a park-owned home (POH) community, you own the homes and rent them out like a traditional landlord. The tenant pays you a combined rent — lot rent plus home rent — that typically runs $800–$1,200 per month. You collect more gross revenue per unit, but you are also responsible for every repair, every turnover, every appliance that breaks, and every roof that leaks.

On paper, park-owned homes look attractive: higher revenue per door. In practice, the math often tells a different story.

The Maintenance Cost Problem Nobody Prices In Correctly

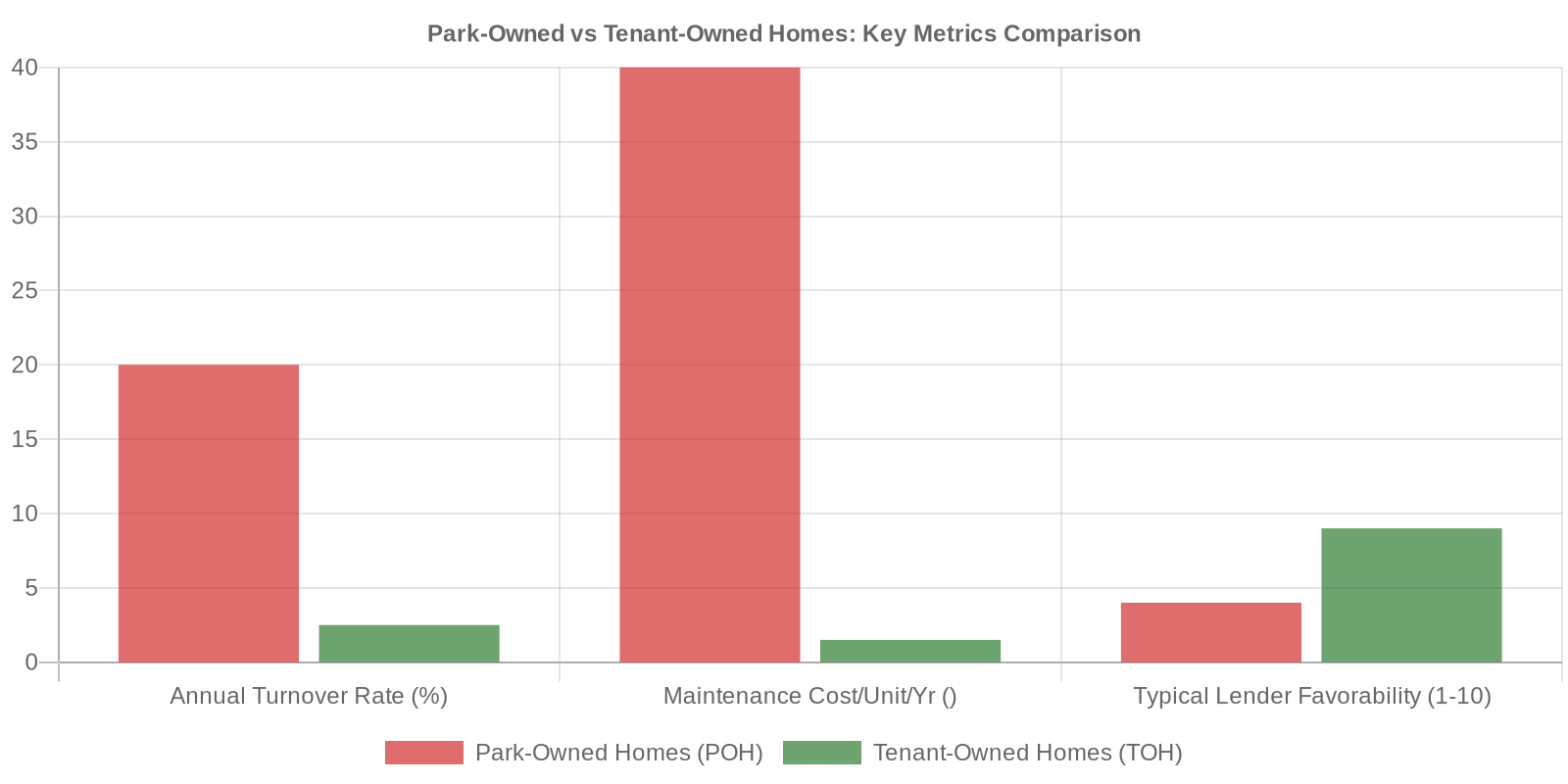

The biggest mistake buyers make when evaluating a park-owned home portfolio is underestimating ongoing maintenance costs. Industry operators typically see $2,000–$8,000 per park-owned home per year in maintenance expenses — and that number spikes sharply when a home turns over between tenants.

A single turnover on a park-owned home can include:

- Deep cleaning and paint: $800–$1,500

- HVAC service or replacement: $500–$3,500

- Plumbing repairs (fixtures, water heater): $400–$1,200

- Flooring replacement: $1,000–$3,000

- Appliance repair or replacement: $300–$1,500

- Exterior repairs (skirting, steps, tie-downs): $200–$800

A modest 80-lot park with 20 park-owned homes experiencing just 25% annual turnover (which is typical) will see five turnovers per year. At $5,000 average per turnover, that is $25,000 in capital that your proforma did not account for — before you even get to ongoing repairs on occupied units.

By contrast, a tenant-owned home community at the same occupancy level has near-zero operator maintenance liability. If a resident’s furnace breaks, it is their problem. If a window needs replacing, that is on them. The operator’s cost structure drops dramatically.

Turnover Rates: The Hidden NOI Killer

Tenant turnover is one of the most significant — and most overlooked — factors in mobile home park investing economics. The data here is stark.

Tenant-owned home communities operate at annual turnover rates of roughly 2–4%. When someone owns their home and has moved it onto a lot (at a cost of $5,000–$15,000 or more), they do not leave lightly. The moving cost alone creates an enormous retention anchor. That is why the mobile home park asset class famously outperforms multifamily on tenant stability — national apartment turnover runs approximately 47% annually versus 2–3% for mobile home park lot tenants.

Park-owned home tenants, however, behave more like traditional apartment renters. Turnover in park-owned home portfolios typically runs 15–25% annually. They have no equity in the home, no moving cost barrier, and no ownership stake. When life changes — a job loss, a relationship ending, a better deal across town — they leave. And you are left with a vacant, depreciated home that needs work before the next resident moves in.

That 20-point difference in turnover rate has a compounding effect on your NOI that most underwriting models do not fully capture.

Evaluating a mobile home park with a mix of park-owned and tenant-owned homes? Our Due Diligence Playbook includes 10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step — including how to underwrite a park-owned home portfolio and model a conversion strategy.

Lender Constraints: Why Park-Owned Homes Change Your Financing Options

If you are planning to use agency debt — Fannie Mae or Freddie Mac programs — on a mobile home park acquisition, the park-owned home percentage matters enormously. Both agencies generally require that the majority of homes in a community be tenant-owned to qualify for their most favorable loan programs. Many lenders set a threshold around 80% tenant-owned minimum for full agency eligibility.

A park with 40% park-owned homes may still be financeable, but likely through community banks, credit unions, or bridge lenders — at higher rates, lower LTV ratios, and stricter terms. In today’s rate environment, that financing differential can meaningfully change your deal economics before you even turn the key.

This is not a minor wrinkle. We have evaluated deals at Keel Team where the park-owned home concentration alone — and the associated financing constraints — changed a deal from attractive to unattractive without any other factor changing.

The chattel lending challenges facing the manufactured housing sector compound this problem. As we covered recently in our analysis of the chattel lending crisis, financing for manufactured homes at the individual level remains constrained — which means park-owned home operators face limited exit options when trying to sell or finance homes to residents.

The Cap Rate Differential Is Real

Here is the data point that should matter most to any buyer: park-owned home heavy communities trade at meaningfully higher cap rates than tenant-owned home communities — reflecting the lower quality and higher risk of the income stream.

A well-occupied mobile home park in the Southeast with 90%+ tenant-owned homes, city water and sewer, and stable lot rents might trade at a 5.5–6.5% cap rate in today’s market. An otherwise similar park with 35–40% park-owned homes will typically trade at 7.5–9.0% — or higher, depending on the age and condition of the homes.

That gap exists because sophisticated buyers price in the maintenance risk, the turnover exposure, the financing constraints, and the management overhead. The market has done the math, and it consistently discounts park-owned home income relative to lot rent income.

This creates a genuine value-add opportunity for operators who know how to close the gap.

The Conversion Strategy: Turning a Problem Into a Value Driver

The most established value-add strategy in mobile home park investing is converting park-owned homes to tenant-owned homes — systematically selling the homes to residents, transforming renters into homeowners, and removing the maintenance liability from the operator’s books.

The mechanics look like this:

- Identify residents in park-owned homes who have demonstrated reliable payment history

- Offer to sell them the home — often at below-replacement cost — through seller financing or a third-party chattel loan

- Structure the sale so the resident’s total payment (chattel loan + lot rent) is comparable to their current combined rent

- Transfer maintenance responsibility to the resident upon closing

When done well, this strategy compresses cap rates over time by improving income quality, reduces operating costs immediately, and creates loyal long-term tenants who now have equity in their homes. A park that starts at 60% park-owned homes and converts to 15% over three years may see its market value increase by 20–30% at resale — not from rent increases alone, but from income quality improvement and financing eligibility expansion.

The conversion process is not without complexity — it requires careful lease restructuring, tenant communication, and proper chattel financing coordination. But it is one of the most powerful tools in the mobile home park operator’s toolkit.

Related: the insurance cost implications of park-owned home portfolios are also significant — operators who own homes carry substantially higher property insurance burdens than those managing purely land-lease communities.

What This Means When You Evaluate a Deal

Before you submit an LOI on any mobile home park, you need clear answers to these questions about the home ownership structure:

- What percentage of homes are park-owned vs. tenant-owned? Get the lot-by-lot breakdown, not an estimate.

- What is the average age and condition of park-owned homes? A 1985 single-wide with a failing HVAC is a different asset than a 2005 double-wide in good condition.

- What is the trailing 24-month maintenance expense per park-owned home? Sellers routinely understate this number. Verify against bank statements, not just seller-provided schedules.

- What is the realistic conversion opportunity? How many current park-owned home residents could qualify for chattel financing or seller-financed purchases?

- How are your lenders treating the park-owned home percentage? Get this answer before you go under contract, not after.

The answers to these questions should directly inform your offer price, your financing strategy, and your three-year operating plan. A park with 30 park-owned homes and a realistic conversion roadmap is a different investment — at a different price — than the same park with no viable conversion path.

Get the MHP Due Diligence Playbook — the complete system for analyzing mobile home park acquisitions with confidence. Covers park-owned home underwriting, conversion strategies, lender checklists, and 55 pages of due diligence frameworks built from 50+ acquisitions.

Frequently Asked Questions

What percentage of park-owned homes is too high when buying a mobile home park?

There is no universal threshold, but most experienced operators set informal limits around 20–25% park-owned homes for a new acquisition. Above 30–35%, the maintenance burden, management complexity, and financing constraints typically outweigh the revenue premium. Exceptions exist when a deep discount and clear conversion path justify the risk.

Can you convert a park-owned home to tenant-owned if the home is in poor condition?

It depends on the condition. Homes that are structurally sound but cosmetically dated are strong conversion candidates — residents can take on maintenance as part of ownership. Homes with significant structural issues (roof, foundation, HVAC failure) generally need remediation before conversion or may need to be removed entirely and replaced with a new home or leased-lot vacancy.

Do park-owned home communities require more active management than tenant-owned communities?

Significantly more. Park-owned home portfolios function more like traditional apartment management — maintenance requests, repair coordination, vacancy management, and turnover work are ongoing. Tenant-owned home communities, once stabilized, can often be managed with a part-time community manager and minimal maintenance overhead. The management cost difference is meaningful for operators who want passive income rather than a second job.

How does a park-owned home conversion affect property taxes?

This varies by state and municipality. In many jurisdictions, manufactured homes titled as real property (when on a permanent foundation) are taxed differently than homes on leased land. When you sell a park-owned home to a tenant, the tax treatment of that home may shift — sometimes increasing taxes on the resident, sometimes decreasing operator liability. Always consult a local CPA and real estate attorney before structuring a conversion program.

What financing structures are used when selling park-owned homes to residents?

The two most common are seller financing (operator holds the note, often at 8–12% interest over 5–15 years) and third-party chattel loans through specialized lenders like 21st Mortgage, Triad Financial Services, or Vanderbilt Mortgage. Seller financing is simpler to execute but ties up capital; chattel loans provide immediate cash but require the resident to qualify. A blended approach — seller-financed with a balloon that triggers a chattel refinance — can work well in markets with limited chattel lending options.