If you’ve invested passively in a mobile home park syndication, you’ve probably received a Schedule K-1 in the mail each spring. And if you’ve stared at it wondering what it all means — you’re not alone. K-1 forms are notoriously confusing, even for experienced investors.

The good news: once you understand the basics, reading your mobile home park K-1 becomes straightforward. More importantly, understanding it reveals just how tax-efficient passive mobile home park investing can be compared to most other asset classes.

What Is a Schedule K-1 and Why Do Passive Investors Receive One?

When you invest in a mobile home park syndication as a limited partner (LP), you’re investing in a partnership — typically structured as a Limited Liability Company (LLC) or Limited Partnership. Partnerships don’t pay income taxes at the entity level. Instead, all income, losses, deductions, and credits pass through to each individual partner, who reports them on their personal tax return.

The Schedule K-1 (IRS Form 1065) is how the partnership communicates your share of that activity. Each year you hold a syndication interest, you’ll receive a K-1 showing:

- Your share of ordinary income or loss from operations

- Your share of rental real estate income or loss

- Depreciation and other deductions allocated to you

- Capital gains or losses (typically at exit)

- Any guaranteed payments

- Interest, dividends, and other pass-through items

The Most Important Box on Your Mobile Home Park K-1

For most passive investors, the single most valuable part of the K-1 is the depreciation allocation — and it often surprises first-time limited partners.

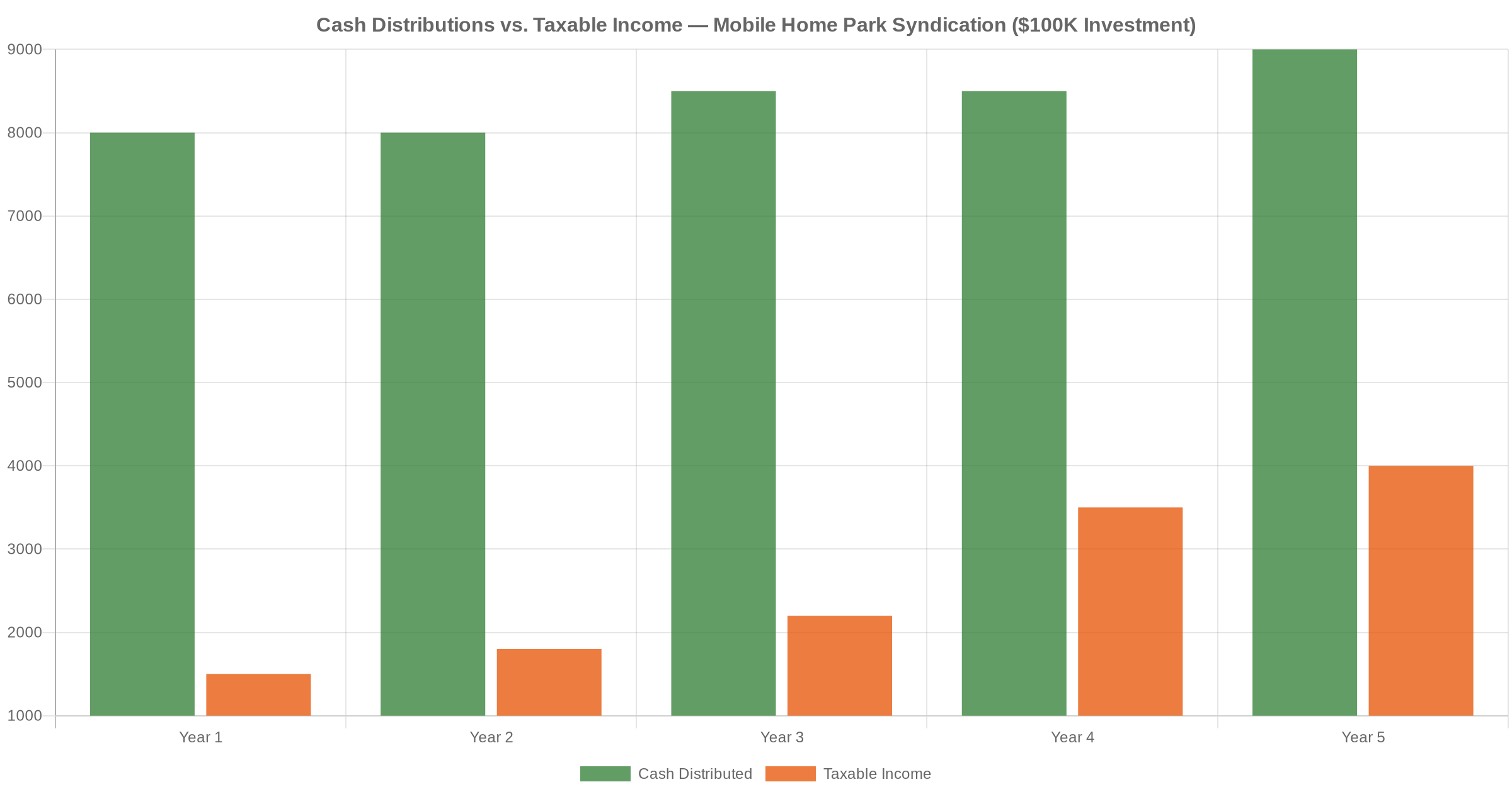

Here’s a typical scenario: you invested $100,000 in a mobile home park syndication, and the partnership distributes $8,000 to you in year one. You might expect to owe taxes on all $8,000. But when your K-1 arrives, it may show something very different.

The deal may have utilized bonus depreciation — a federal tax provision that allows real estate partnerships to accelerate depreciation deductions, often substantially in the first year. Your allocated share of that depreciation could dramatically reduce — or even eliminate — your taxable income from the distribution.

In practice, many mobile home park passive investors receive meaningful cash distributions while reporting little or no taxable income in the early years of a hold. This is the depreciation pass-through at work. For a deeper look at the full tax picture, see our post on the tax benefits of mobile home park investing as a limited partner.

Key Line Items on a Mobile Home Park Partnership K-1

Here’s a breakdown of the boxes you’ll encounter most often as a passive investor in a mobile home park deal:

Box 1 — Ordinary Business Income (Loss)

Your share of the partnership’s ordinary income or loss from operations. A loss here can offset other passive income you have from other investments, subject to passive activity loss rules.

Box 2 — Net Rental Real Estate Income (Loss)

For mobile home park syndications structured as rental real estate, lot rent income flows through here. Depreciation deductions are netted against rental income, which often produces a paper loss even when the investment is generating positive cash flow.

Box 9a — Net Long-Term Capital Gain (Loss)

Appears primarily at exit. When the mobile home park is sold, your share of the gain flows through here — typically taxed at favorable long-term capital gains rates rather than ordinary income rates.

Box 13 — Other Deductions

Often includes Section 179 deductions or bonus depreciation allocations. This is where much of the tax-sheltering power shows up for passive investors in mobile home park deals.

Box 20 — Other Information

Includes Section 199A information (Qualified Business Income deduction eligibility) and other items specific to your situation. Your CPA will need to review this carefully.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Passive Activity Loss Rules: What Every Limited Partner Must Understand

One of the most misunderstood aspects of K-1 income for passive investors involves the passive activity loss (PAL) rules under IRS Section 469.

The core rule: losses from passive investments — like limited partner interests in real estate syndications — can generally only offset income from other passive activities, not active income like wages or self-employment earnings.

This matters because your mobile home park K-1 may show a paper loss due to depreciation. That loss is “suspended” until you have other passive income to absorb it, or until you exit the investment — at which point all accumulated suspended losses become fully deductible in the year of sale.

There’s a significant exception: Real Estate Professional (REP) status. If you or your spouse qualifies as a real estate professional under IRS rules (750+ hours per year in real estate activities, with real estate as the primary occupation), passive losses can offset ordinary income. This is a major reason high-income professionals — doctors, dentists, attorneys, business owners — often use mobile home park syndications as part of their tax strategy. For more context, see our post on why professionals invest in mobile home parks.

For most passive investors without REP status: the paper losses accumulate and become fully deductible when the investment is eventually sold. They’re not wasted — they’re deferred.

When Does Your K-1 Arrive — and What If It’s Late?

K-1 forms are technically due by March 15 for partnerships with a December 31 fiscal year. However, many real estate partnerships file for extensions, which means your K-1 may not arrive until September or even later.

This is one of the most common frustrations passive investors in mobile home park syndications encounter at tax time. If your K-1 is delayed, you have two practical options:

- File a personal return extension (Form 4868), giving you until October 15 to file — this is the standard recommendation for anyone holding partnership interests

- File with estimates and amend later — possible, but it adds cost and complexity

If you invest in multiple mobile home park syndications, defaulting to a personal extension each year simplifies tax season considerably. It’s a habit worth building from the start.

Basis Tracking: Why It Matters More Than Most Investors Realize

Your outside basis in the partnership is a running ledger of what you’ve contributed, what income and losses have been allocated to you, and what distributions you’ve received. It matters because:

- You can only take losses up to your current basis

- It determines whether a distribution is taxable income or a tax-free return of capital

- It directly affects your gain or loss calculation at exit

Every year you receive a K-1, your tax advisor should be updating your basis. If you’ve been handling K-1 filings yourself without formally tracking basis, a CPA with real estate partnership experience can get you current — it’s worth the investment, particularly as your portfolio of mobile home park interests grows. For a broader overview of what smart limited partners track and monitor, see our passive investing limited partner guide.

What to Give Your CPA at Tax Time

Make it easy for your tax advisor. When K-1 season arrives, provide:

- The K-1 form itself

- All supplemental schedules (often several additional pages beyond the main form)

- Section 743(b) adjustment schedules, if applicable (relevant if you acquired your LP interest from another investor in a secondary transaction)

- Any plain-language summary or activity statement the operator includes with the K-1

Well-run mobile home park operators often include an investor-friendly memo alongside the K-1 that explains key line items in plain language. If yours doesn’t, it’s a reasonable ask — and the quality of operator communication at tax time is a meaningful signal about how they run everything else.

The Bottom Line on Mobile Home Park K-1 Forms

The Schedule K-1 is both an administrative obligation and a window into the tax efficiency of your mobile home park investment. Yes, it adds complexity to your annual filing. But it’s also the mechanism through which depreciation pass-throughs, long-term capital gains treatment at exit, and potential Qualified Business Income deductions reach you as a passive investor.

Understanding your K-1 isn’t just about compliance — it’s about fully appreciating the return profile of what you own. When you see near-zero taxable income next to a healthy cash distribution, that’s not an error. That’s the strategy working exactly as designed.

If you’d like to learn more about how mobile home park investing works for passive investors, feel free to reach out through our contact page and we’ll be happy to connect.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.