There’s a conversation happening in group chats among orthopedic surgeons, dental practice owners, and partners at regional law firms — and it goes something like this:

“Have you looked at mobile home park syndications?”

If you’ve heard this conversation, you’re not alone. High-income professionals with limited time and significant W-2 income are increasingly turning to manufactured housing communities as a passive investment vehicle. The reasons are practical, not sentimental: strong risk-adjusted returns, meaningful tax advantages, and a business model that doesn’t require them to answer a tenant call at 11 PM.

This post breaks down exactly why mobile home parks are gaining traction among this audience — and what you need to understand before exploring the asset class further.

The Problem with Being High-Income and Busy

Doctors, attorneys, and dentists typically earn well above the national average. But there’s a structural problem with W-2 income, even at high levels: it stops the moment you stop working. And it gets taxed heavily — often at 35–37% federal plus state.

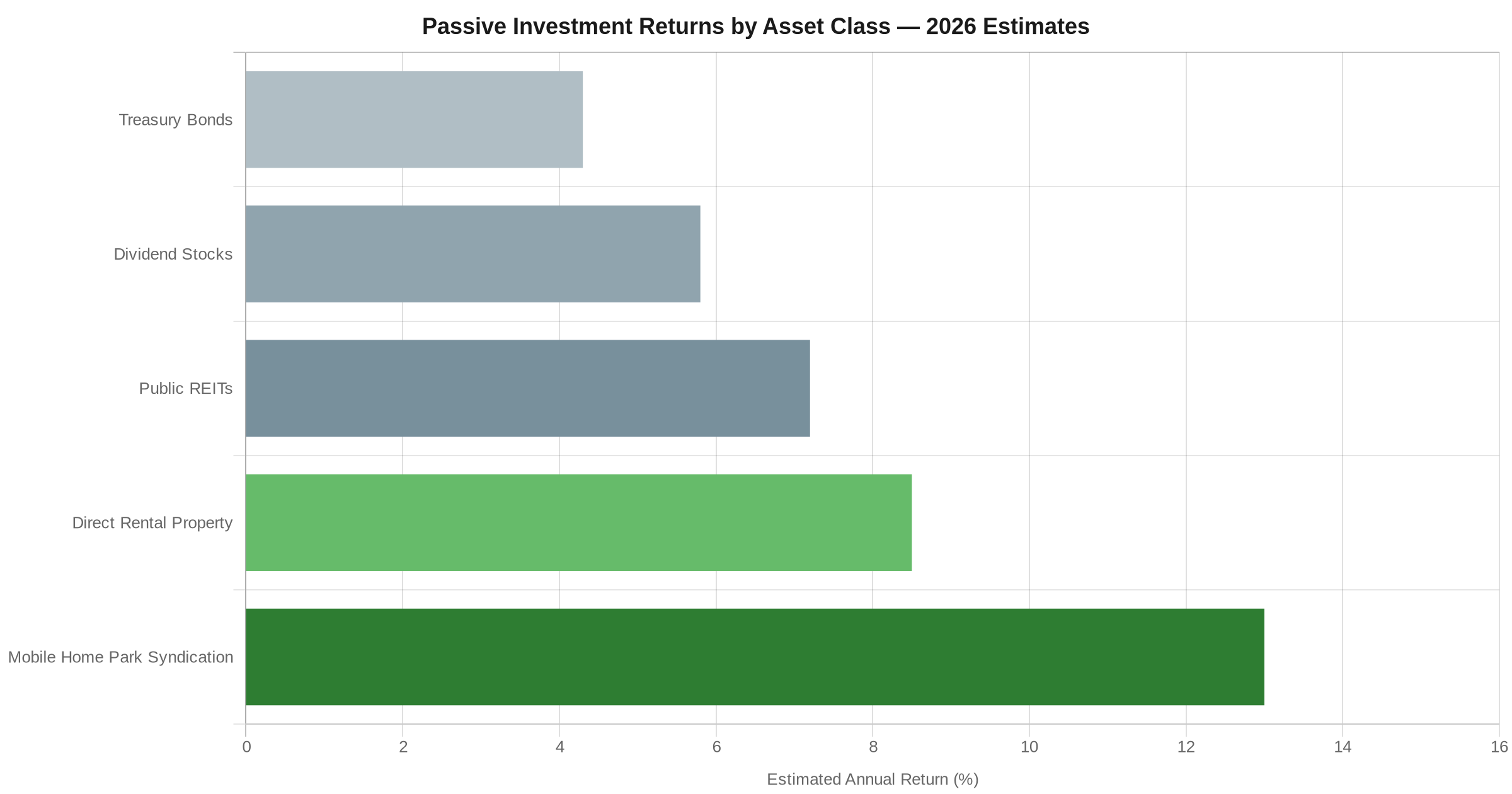

Most investment options available to high-income earners — index funds, REITs, dividend portfolios — are taxed as ordinary income or capital gains, generate modest yields relative to risk, and offer limited depreciation benefits. Direct rental property ownership solves some of this, but it introduces management complexity that most professionals simply don’t have time for.

What many high-earning professionals actually want is:

- True passivity — no active management required

- Meaningful cash distributions on a predictable schedule

- Depreciation and tax shelter to offset W-2 income

- Asset class stability — something that doesn’t crater in a recession

Mobile home park syndications check all four boxes.

What Makes Mobile Home Parks Structurally Different

The manufactured housing business model is fundamentally different from apartments, office, or retail real estate. In a mobile home park, residents own their homes and rent only the land beneath them — called a lot. This creates an unusual dynamic that drives remarkable tenant stability:

- Moving a manufactured home costs $5,000–$10,000 or more. Most residents don’t do it. Annual home turnover in mobile home parks runs roughly 2–3%, compared to 45–50% in apartment communities. That stickiness translates directly into lower vacancy risk and more predictable cash flow.

- No meaningful new supply. Zoning restrictions and community opposition have made it nearly impossible to build new mobile home parks. Fewer than 20 new communities per year have been permitted nationally, against a base of approximately 45,000 existing communities. This supply constraint is structural — it doesn’t reverse in a healthy economy.

- Counter-cyclical demand. When the economy weakens, demand for affordable housing strengthens. Mobile home parks generated positive NOI growth throughout the 2008–2009 financial crisis and through COVID-19 — while apartments and retail bled occupancy.

For a professional who watched their retirement account drop 40% in 2008, the stability of a supply-constrained affordable housing asset is genuinely compelling.

The Tax Angle: Why High Earners Specifically Benefit

This is where mobile home park investing gets particularly interesting for professionals with high W-2 income.

In a real estate syndication, passive investors receive a K-1 each year reflecting their proportional share of income, losses, and depreciation. Mobile home park deals generate significant depreciation through cost segregation studies — accelerating deductions on paved roads, utility infrastructure, and other components.

For a physician earning $500,000/year in W-2 income, a $200,000 investment in a mobile home park syndication with bonus depreciation of 80–90% could generate $160,000–$180,000 in first-year depreciation losses — which may offset a significant portion of passive income for tax purposes. (Always consult your CPA before making investment decisions — tax outcomes vary based on individual circumstances and IRS passive activity classification.)

This is why high-income professionals specifically benefit from the asset class. A retiree on fixed income doesn’t need the same depreciation offset. A physician at peak earnings does.

For a deeper dive on how the tax math works, read our full breakdown: Tax Benefits of Investing in Mobile Home Parks as a Limited Partner.

Two decades of hard-won lessons distilled into one free guide. Whether you're evaluating your first deal or your fiftieth, these insights will sharpen your approach.

How a Mobile Home Park Syndication Works

In a syndication, a general partner (the operator) sources a mobile home park deal, negotiates the purchase, arranges financing, and manages the asset throughout the hold period. Passive investors — limited partners — contribute capital in exchange for an ownership stake and a pro-rata share of distributions and profits.

A typical mobile home park syndication structure looks like this:

- Preferred return: Limited partners receive a preferred return (often 6–8%) before the general partner participates in profits

- Cash flow distributions: Quarterly or semi-annual payments from lot rent income, after operating expenses and debt service

- Equity split on exit: When the property sells — typically after a 5–7 year hold — remaining profits split between limited and general partners based on the agreed waterfall structure

Because mobile home parks are land-rent businesses with low ongoing capital expenditure (residents own the homes), operating margins are generally higher than apartment communities. A well-operated mobile home park can generate cash-on-cash returns of 6–10% before appreciation — difficult to match in most passive real estate structures at current cap rates.

For a detailed breakdown of how structures and distributions work: Mobile Home Park Syndication Explained: GP/LP Structure and Return Waterfalls.

What to Look for in a Mobile Home Park Operator

Passive investing is only as good as the operator running the deal. Before investing in any syndication, vet the general partner thoroughly. Key questions to ask:

- How many mobile home parks have you operated — not just acquired? Track record in operations matters more than deal count.

- Have you previously returned capital to limited partners? A track record of exits — not just acquisitions — matters.

- What is your infill strategy? Occupancy improvement is often the core value-add thesis — make sure the operator has a specific, credible plan.

- How do you communicate with investors during the hold? Quarterly reports, investor calls, and proactive updates signal a professional operation.

- What is your lender relationship history? Agency financing access affects both deal quality and refinance optionality.

For a complete framework on evaluating operators before you commit capital: How to Evaluate a Mobile Home Park Operator Before You Invest.

What Returns Should Professionals Realistically Expect?

Return expectations vary by deal, market, and operator. Here are realistic ranges for mobile home park limited partner investments based on current market conditions:

- Cash-on-cash return: 5–9% annually (varies based on leverage and occupancy at acquisition)

- Preferred return: Usually 6–8% before general partner participation

- Equity multiple over 5–7 year hold: Target ranges of 1.6x–2.2x are common in operator projections

- Internal Rate of Return: Target IRRs of 12–18% are typical in operator materials, though actual results depend heavily on exit cap rates and hold timing

These are targets and general ranges — not guarantees. Real estate investments carry risk, including loss of principal. Due diligence on both the deal and the operator is non-negotiable.

The Accredited Investor Requirement

Most mobile home park syndications are offered under Regulation D Rule 506(b) or 506(c), which require investors to be accredited. The thresholds as of 2026:

- Individual income exceeding $200,000/year ($300,000 combined with a spouse) for the prior two years, with expectation of the same going forward

- Net worth exceeding $1 million, excluding the primary residence

- Holding certain professional licenses (Series 7, 65, or 82)

Most physicians, attorneys, and dental practice owners qualify on income alone. Your CPA or financial advisor can confirm your accreditation status if you're unsure.

Conclusion

High-income professionals are drawn to mobile home park investing for reasons that go beyond yield numbers. It's an asset class with genuine scarcity, counter-cyclical demand, and a business model that doesn't require active involvement from limited partners.

The combination of stable cash flow, depreciation benefits, and supply-constrained fundamentals creates something rare in passive investing: an income-generating asset that tends to hold value when other real estate classes struggle.

If you're exploring passive real estate options and want to understand more about how this asset class works, the best next step is education. Start with the resources below.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Frequently Asked Questions

Do I need to be an accredited investor to participate in a mobile home park syndication?

In most cases, yes. Most mobile home park syndications are structured as private placements under Reg D 506(b) or 506(c), which require accredited investor status. A small number of deals allow a limited number of non-accredited investors under 506(b), but this is the exception rather than the rule.

How much capital do I typically need to invest in a mobile home park syndication?

Most syndications have minimum investment thresholds of $50,000–$100,000 per limited partner. Some larger platforms set minimums at $25,000. This differs significantly from direct acquisition, which often requires $500,000 or more in equity for a mid-sized mobile home park.

Can I use a self-directed IRA to invest in a mobile home park syndication?

Yes. Syndication investments can be made through self-directed IRAs and self-directed 401(k)s, subject to UBTI (unrelated business taxable income) rules. Consult your custodian and tax advisor before investing retirement funds in a syndication.

What are the primary risks of investing in a mobile home park syndication?

Key risks include: illiquidity (capital is locked up for the hold period, typically 5–7 years), operator execution risk (the general partner may not achieve underwriting projections), regulatory risk (state tenant protection laws can affect NOI), and exit risk (cap rate expansion at sale can reduce the equity multiple). Thorough due diligence is essential.

How are mobile home park syndication distributions taxed?

Distributions are generally treated as passive income. K-1 losses from depreciation can offset passive income. Tax treatment is complex and highly individual — a CPA with real estate syndication experience is strongly recommended for any professional considering this investment type.

Get the top 20 lessons from two decades of mobile home park investing — free.