If you’ve been exploring real estate alternatives and heard the term mobile home park syndication, you’re not alone. More investors are looking at manufactured housing as a stable, income-producing asset — and syndication is one of the most accessible ways to participate without buying a community outright.

But before committing capital, you need to understand exactly how these deals are structured, how money flows between partners, and what separates a well-run syndication from a problematic one. This guide breaks it all down in plain language.

What Is Mobile Home Park Syndication?

A mobile home park syndication is a private real estate investment structure where a group of investors pool their capital to acquire, operate, and eventually sell a mobile home park community. It’s governed by federal securities law — most mobile home park syndications operate under Regulation D, either 506(b) or 506(c) — which determines how the deal can be marketed and who can participate as an investor.

The structure divides participants into two distinct roles: the General Partner (GP) and Limited Partners (LPs). Understanding those roles is the starting point for everything else.

The GP/LP Structure: Who Does What

The General Partner (GP)

The GP — also called the sponsor or operator — handles everything active: sourcing the deal, conducting due diligence, negotiating the purchase, arranging financing, managing day-to-day operations, and executing the business plan. The GP assumes full operational responsibility and earns compensation (fees and a profit share) in exchange for that work.

The Limited Partners (LPs)

The LPs are the passive investors. They contribute equity capital and receive proportional ownership in the property. Limited partners have no day-to-day operational role and their liability is capped at their invested capital. In exchange for giving up control, they receive distributions from operating cash flow and a share of profits when the property is eventually sold.

This division is what makes mobile home park syndication attractive to busy professionals: you hold real ownership in a tangible income-producing asset and receive distributions — without managing a single tenant or utility bill.

How the Capital Stack Is Structured

A typical mobile home park syndication is capitalized with a combination of debt and equity:

- Senior debt (60–70%): A first-position mortgage from a lender — often agency debt through Fannie Mae or Freddie Mac, or a community bank. The debt is secured by the property and serviced from lot rent income.

- LP equity (25–35%): Passive investor capital covering the down payment and operating reserves.

- GP co-invest (1–5%): The sponsor’s own capital in the deal — aligning their financial interests directly with limited partners.

For a $4 million mobile home park acquisition, this might look like: $2.8M bank loan + $1.1M LP equity + $100K GP co-investment.

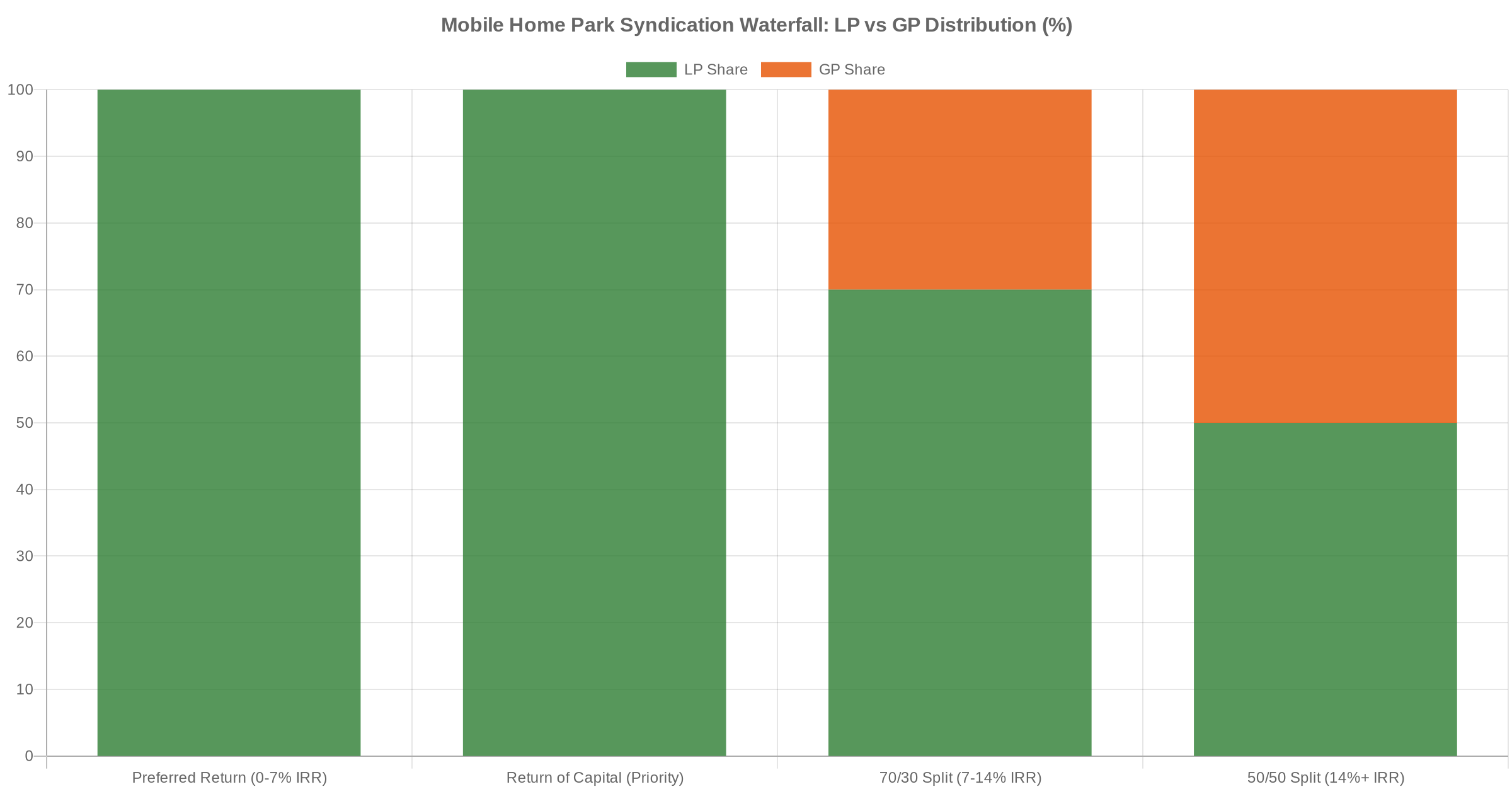

Understanding the Return Waterfall

The return waterfall defines how profits are divided between GPs and LPs at each stage. This is one of the most important — and most frequently misunderstood — elements of any mobile home park syndication deal.

Tier 1: Preferred Return

Most mobile home park syndications include a preferred return — typically 6–8% annualized — that LPs receive before the GP takes any profit split. This is paid from operating cash flow (lot rent collected minus expenses and debt service) and is usually cumulative: if it isn’t fully paid in one quarter, it accrues and is paid from future distributions when cash flow allows.

The preferred return protects LPs during slower periods and establishes a minimum return threshold the GP must clear before any promote is earned.

Tier 2: Return of Capital

Before equity split profits are distributed at exit, investors receive their contributed capital back — from proceeds of a property sale or refinance. This return of capital is senior to the GP’s promoted interest.

Tier 3: Equity Split (the Promote)

Once LPs have received their preferred return and original capital, remaining profits are split between GP and LPs. A common structure:

- Up to a 14% IRR: 70% to LPs / 30% to the GP

- Above 14% IRR: 50% to LPs / 50% to the GP

The GP’s additional profit above their pro-rata co-investment share is called the promote or carried interest — the incentive for performance above the baseline. It’s what makes GP compensation back-loaded and aligned with investor outcomes.

To understand how acquisition fees, asset management fees, and disposition fees work alongside the waterfall, read our detailed breakdown of sponsor compensation structures.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

How Passive Investors Actually Get Paid

LP distributions come from two sources throughout the life of a mobile home park syndication:

- Operating cash flow: Quarterly or monthly distributions from lot rent collected, after debt service and operating expenses. These vary based on occupancy rates, expense management, and whether capital improvements are being funded from reserves versus cash flow.

- Exit proceeds: The larger payout — distributed when the mobile home park is sold or refinanced. This is when equity appreciation and the profit split are fully realized.

Hold periods for mobile home park syndications typically range from 5 to 10 years. Value-add deals with significant operational upside may target a 3–5 year exit. Your capital is illiquid during this period, so understanding the projected timeline before committing is essential.

Exit Strategies: How a Mobile Home Park Syndication Ends

When the business plan runs its course, the GP executes one of three primary exit strategies:

- Outright sale: The most common exit — sell the property at a higher price than acquisition cost. Proceeds are distributed to investors after debt payoff, closing costs, and fees per the waterfall.

- Cash-out refinance: The GP refinances at a higher valuation after improvements, pulling out equity that’s distributed to LPs — often tax-efficiently, since a refinance is not a taxable event. The property continues operating, and LPs may receive ongoing distributions post-refi.

- 1031 Exchange: Proceeds roll into a larger acquisition, deferring capital gains tax. Limited partners may roll their equity into the next deal or receive a cash distribution, depending on the structure.

What Due Diligence Should a Passive LP Do on a Sponsor?

The quality of any mobile home park syndication depends almost entirely on the GP’s execution. Before committing capital, ask:

- Track record: How many deals have they completed and exited? Can they provide audited financials or investor letters from prior deals?

- Alignment: Is the GP co-investing their own capital? How much?

- Deal structure: Is the preferred return cumulative? Are fees within market norms?

- Market selection: Do they operate in markets with strong population growth, city water and sewer utilities, and demonstrable lot rent upside?

- References: Can you speak directly with investors from prior syndications?

For a detailed checklist of warning signs to avoid, see our guide to mobile home park syndication red flags — seven things to look out for before committing capital.

Why Mobile Home Parks Are Well-Suited to the Syndication Model

Not every real estate asset class is equally suited to the syndication structure. Mobile home parks have characteristics that make them particularly effective:

- Predictable cash flow: Lot rent is stable and consistent. Residents own their homes and simply lease the land — average annual turnover in mobile home park communities is roughly 2%, compared to 47% for apartment communities.

- Supply constraints: Only around 20 new mobile home park communities are permitted nationally each year across approximately 45,000 total communities. Zoning restrictions and community opposition have made new supply nearly impossible to add at scale.

- Affordable housing tailwind: With over 20 million Americans living in manufactured housing, demand is structural — not cyclical. Economic downturns tend to increase, not decrease, demand for affordable housing options.

- Lower management intensity: Because residents own their homes and lease the land, operators face significantly lower maintenance overhead compared to apartment buildings where the landlord owns every unit.

These fundamentals make it possible for a well-underwritten mobile home park syndication to generate consistent preferred return distributions throughout the hold — not just at exit.

Is Mobile Home Park Syndication Right for You?

Mobile home park syndication is a compelling structure for passive investors seeking real asset exposure with income and appreciation potential. But it’s not without risk. Capital is illiquid for years. Outcomes depend on the operator’s skill and integrity. And returns are never guaranteed.

The investors who do well in this space tend to be those who do the work upfront: vetting sponsors thoroughly, reading the PPM carefully, understanding the waterfall, and asking hard questions before writing a check.

If you’re interested in learning more about mobile home park investing and whether it might align with your financial goals, reach out and we’re happy to set up a call.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Frequently Asked Questions About Mobile Home Park Syndication

What is the minimum investment for a mobile home park syndication?

Minimums vary by deal and sponsor, but $50,000–$100,000 is typical for mobile home park syndications. Most 506(b) deals require investors to be accredited (net worth over $1M excluding primary residence, or income above $200K annually) and to have a pre-existing substantive relationship with the sponsor before investing.

How long is my capital locked up in a mobile home park syndication?

Most mobile home park syndications target a hold period of 5–10 years. Capital is generally illiquid during this period — there is no liquid secondary market for LP interests. Some sponsors permit transfers with GP approval. Understanding the projected timeline is critical before committing.

Is the preferred return in a syndication guaranteed?

No. A preferred return is a preferential distribution from operating cash flow — LPs receive it before the GP takes any profit split — but it is not legally guaranteed like a bond coupon. If the property underperforms due to high vacancy or unexpected capital expenditures, distributions may be reduced or deferred. Cumulative preferred returns accrue and are paid from future distributions when cash flow allows.

How does mobile home park syndication differ from investing in a mobile home park REIT?

A publicly traded REIT like Sun Communities or Equity LifeStyle Properties is highly liquid, diversified across hundreds of communities, and trades on a stock exchange. A private syndication is illiquid, typically involves one to several communities, and can offer higher potential returns — without the liquidity premium built into public REIT valuations. We cover this comparison in detail in our Mobile Home Park Syndication vs. REIT guide.

Can I use a Self-Directed IRA to invest in a mobile home park syndication?

Yes. Many passive investors use a Self-Directed IRA (SDIRA) or Solo 401(k) to invest in private real estate syndications. This requires a qualified custodian and proper documentation from the syndication sponsor. UBTI (Unrelated Business Taxable Income) may apply when the investment is leveraged. Always consult a tax advisor familiar with SDIRA rules before investing this way.

Get the top 20 lessons from two decades of mobile home park investing — free.