Mobile home park investing has quietly become one of the most compelling real estate strategies of the decade. National occupancy sits at 93%, average lot rents have grown to $752 per month, and transaction volume in the manufactured housing sector jumped 47.1% in 2025. Yet despite that momentum, the market remains fragmented — roughly 45,000 communities across the country, most owned by private operators, not institutions.

If you are new to this asset class and wondering where to start, this guide breaks down exactly how to invest in mobile home parks, step by step. Whether you are considering buying and operating a community yourself or investing as a limited partner in a syndication, these fundamentals apply.

Why Mobile Home Parks Attract Serious Investors

Before diving into the how, it helps to understand the why. Mobile home park investing stands out for several structural reasons that other real estate asset classes cannot match:

- Almost zero new supply: Only about 20 new mobile home park communities are permitted per year across the entire country. That is roughly 0.04% of the existing 45,000+ community stock. Compare that to multifamily, where new apartment supply adds roughly 3.8% annually.

- Sticky tenants: Annual home turnover in mobile home parks runs around 2.2% compared to approximately 47% in apartment communities. Moving a manufactured home costs thousands of dollars, so residents rarely leave.

- Recession resilience: During the 2008-2009 financial crisis, manufactured housing community NOI was +1.5% while apartment NOI fell -5.6%. During COVID in 2020, mobile home parks posted +4.2% while apartments fell -3.2%.

- Affordable housing tailwind: With 20+ million Americans living in manufactured housing communities, demand for affordable housing continues to grow as home prices and rents remain elevated.

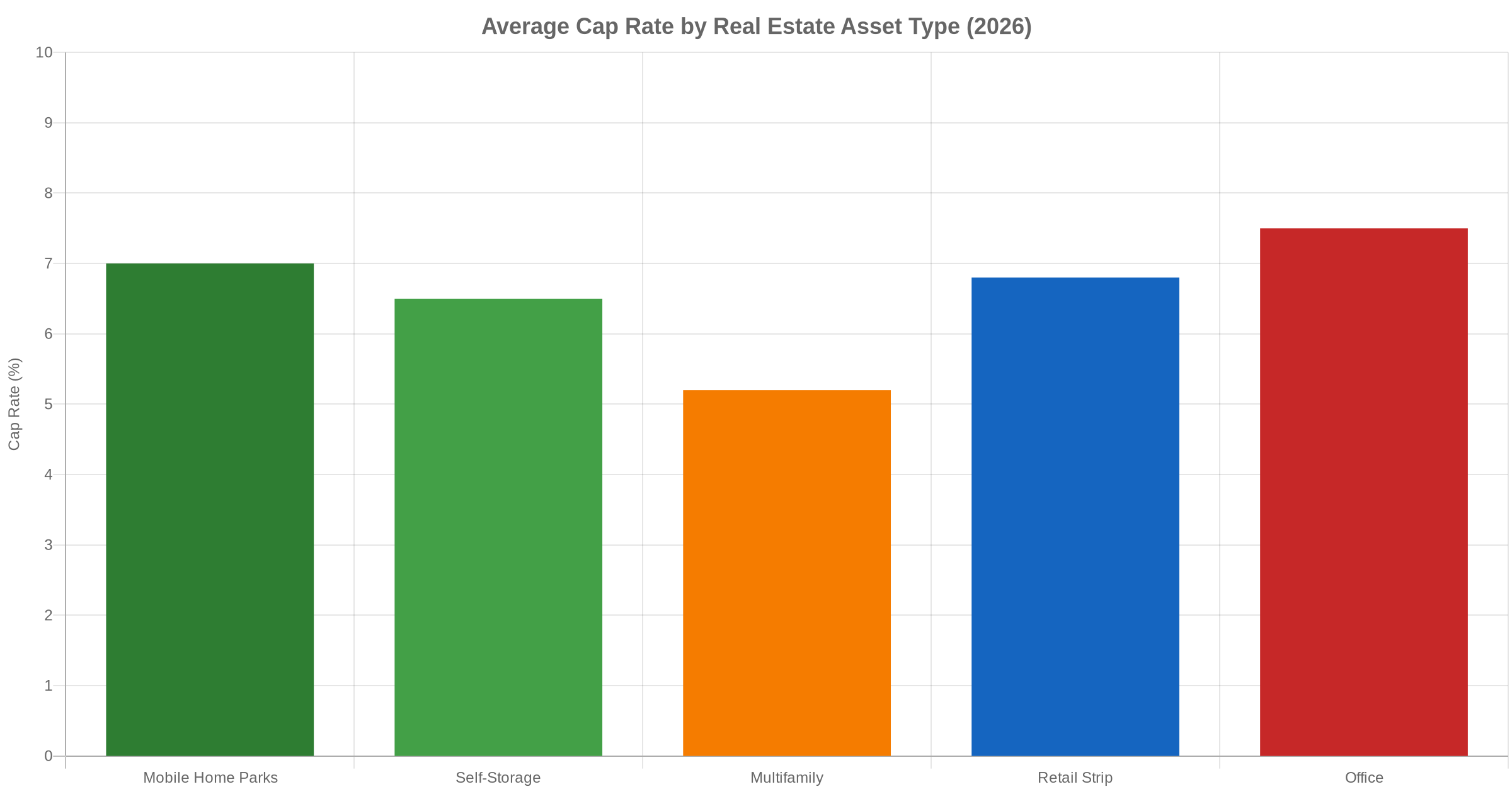

These structural advantages produce the cap rate premium shown in the chart below:

How Mobile Home Parks Generate Income

The core business model is straightforward: you own the land, and residents own (or rent) the homes sitting on it. Each month, residents pay you lot rent for the right to park their home on your land and access community utilities and amenities.

Here is what makes this model powerful:

- You are not responsible for maintaining the homes when residents own them

- Your primary expense is infrastructure: roads, utilities, common areas, and community management

- Operating expense ratios for well-run tenant-owned home communities typically run 30-40% of gross income, lower than apartments at 45-55%

- Net Operating Income (NOI) = Total Lot Rent Revenue minus Operating Expenses

For a deeper look at how the numbers work, see our guide on how to calculate net operating income for a mobile home park.

Two Ways to Invest: Active Operator vs. Passive Limited Partner

Before you start analyzing deals, you need to decide how you want to participate in this asset class. There are two primary paths:

1. Active Operator (Direct Ownership)

You find, acquire, and operate a mobile home park yourself. This means handling management (or hiring a manager), dealing with tenant issues, overseeing maintenance, and making all strategic decisions. The upside: you capture 100% of the economics. The reality: it requires significant time, capital, and operational expertise, especially for your first deal.

2. Passive Limited Partner (Syndication)

You invest capital alongside an experienced operator (the General Partner) who sources, acquires, and manages the deal. As a limited partner, you receive quarterly distributions and a share of the equity upside at exit without day-to-day responsibilities. Most syndications require investors to be accredited (net worth $1M+ or income $200K+). Minimum investments typically range from $50,000 to $100,000.

For most people new to this asset class, starting as a passive investor is a logical first step. It lets you learn the business from the inside while an experienced operator handles the heavy lifting.

Key Metrics Every Beginner Must Understand

Regardless of which path you choose, these are the numbers that matter:

- Cap Rate: NOI divided by purchase price. The higher the cap rate, the more income relative to cost. Stabilized mobile home parks in major Southeast markets typically trade at 6.5-9% cap rates in 2026. See our cap rate breakdown by state.

- Occupancy Rate: The percentage of lots currently generating income. Most lenders want to see 85%+ occupancy. The national average is currently around 93%.

- Lot Rent vs. Market Rate: Is the current lot rent below market? That gap represents value-add potential. Average U.S. lot rent is $752/month, but markets vary widely.

- Utilities: Who owns the utility infrastructure? City water and sewer is ideal. Private wells or lagoon systems add cost, risk, and complexity.

- Tenant-Owned Homes vs. Park-Owned Homes: The more homes residents own, the lower your operating costs and the stickier your tenants. A high park-owned home ratio adds management complexity and expense.

Two decades of hard-won lessons distilled into one free guide. Whether you are evaluating your first deal or your fiftieth, these insights will sharpen your approach.

How to Find Mobile Home Parks for Sale

Finding good deals requires a multi-channel approach. Here are the most effective methods:

On-Market Listings

Brokers like Marcus and Millichap, CBRE, and specialty mobile home park brokers list properties on LoopNet and CoStar. These deals are competitively priced, but they are a good way to learn what is available and calibrate your pricing expectations.

Direct-to-Owner Outreach

The best mobile home park deals come from direct relationships with owners who have not listed their property. Common tactics include direct mail campaigns, cold calling from county parcel data, and attending regional manufactured housing association events. Many owners are aging operators who want to sell but have not listed publicly. Reaching them first gives you a significant advantage over competing buyers.

Broker Relationships

Cultivate relationships with regional brokers who specialize in manufactured housing. They will bring you off-market opportunities before they hit public listing platforms.

How to Finance Your First Mobile Home Park

Mobile home park financing has evolved significantly. Here is a quick overview of the main options available to buyers in 2026:

- Agency Debt (Fannie Mae/Freddie Mac): Best rates, longest terms (25-30 years), up to 80% LTV. Requires stabilized occupancy of 85%+ and minimum loan sizes around $2M+.

- Community and Regional Banks: More flexible on asset condition and occupancy. Shorter terms (5-7 year balloons), 70-75% LTV.

- Seller Financing: The most flexible option. Sellers who own parks outright may carry a note, ideal for value-add or transitional deals that do not yet qualify for agency debt.

- Bridge Loans: Short-term financing for repositioning plays. Higher rates, typically 65% LTV.

For a comprehensive breakdown of every loan type, current rates, and what lenders require, see our Mobile Home Park Financing Guide 2026.

Due Diligence: What to Verify Before You Close

Mobile home park due diligence has some unique elements that differ from other real estate asset classes. Before closing on any deal, verify the following:

- Utility infrastructure: Who owns the water and sewer lines? What is the condition of the electrical pedestals?

- Rent rolls and leases: Are current rents documented? Are leases month-to-month or long-term?

- Home ownership status: Which homes do residents own vs. which does the park own?

- Environmental Phase 1: Any soil contamination, underground tanks, or lagoon issues?

- Title and zoning: Is the park a legal conforming use? Any pending rezoning pressure?

- Actual occupancy vs. claimed: Drive every street. Count occupied homes, vacant lots, and abandonment situations yourself. Do not rely on the seller spreadsheet alone.

Our Mobile Home Park Due Diligence Checklist covers all 25 items you should verify before signing.

Taking Your First Step

Mobile home park investing rewards patience, preparation, and operational discipline. Whether you are pursuing active ownership or passive LP exposure, the path forward is the same: learn the fundamentals, study real deals, build relationships in the industry, and take deliberate action when the right opportunity presents itself.

The data is clear. This asset class has delivered consistent, risk-adjusted returns for decades, and the structural tailwinds — zero new supply, sticky tenants, affordable housing demand — show no sign of reversing. The question is not whether mobile home park investing works. It is whether you are ready to do the work to get started.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal from the first site visit to closing day.

Frequently Asked Questions

How much money do I need to invest in a mobile home park?

For direct ownership, smaller mobile home parks (30-70 lots) in secondary markets can be acquired for $500,000 to $2,000,000 with 20-30% equity required. For passive syndication investing, most deals require $50,000 to $100,000 minimum and accredited investor status.

Are mobile home parks a good investment for beginners?

Mobile home parks can be excellent investments, but the learning curve is real. The business model is straightforward, but operational nuances around utilities, infill, and community management take time to master. Passive syndication investing is often a better starting point for beginners who want exposure to the asset class without managing operations themselves.

What is a good cap rate for a mobile home park?

In 2026, stabilized mobile home parks in major Southeast markets (NC, TN, GA, SC) typically trade at 6.5-9% cap rates. Premium communities with high occupancy and city utilities can trade at 5.5-6.5%. Smaller, rural, or value-add communities may trade at 9-12% cap rates, reflecting higher risk and more operational upside.

Do I need to be an accredited investor to invest in mobile home parks?

For direct ownership, no. Anyone can buy a mobile home park. For syndications and private placements, most deals are offered under Reg D 506(b) and require investors to be accredited, meaning a net worth of $1M+ excluding primary residence or income of $200K+ annually.

What is the difference between a mobile home and a manufactured home?

Legally, homes built before June 15, 1976 are called mobile homes and predate federal HUD construction standards. Homes built after that date to HUD Code are manufactured homes. Most modern communities contain manufactured homes. The distinction matters for financing, insurance, and valuation. Learn more about the difference here.

Get the top 20 lessons from two decades of mobile home park investing, free.