Net operating income — NOI — is the single most important number in mobile home park investing. It determines what a property is worth, how much debt it can support, and whether a deal is worth pursuing at all.

Yet plenty of investors coming from single-family or small multifamily backgrounds underestimate how different mobile home park net operating income looks compared to other asset classes. The income streams are different. The expense ratios are different. The risks are different. Get comfortable with this calculation and you’ll evaluate deals faster and more accurately than most buyers in the market.

This guide walks through exactly how to calculate net operating income for a mobile home park, what expenses belong in the formula (and which ones don’t), and how to use NOI to drive your valuation. For a broader view of how mobile home park returns work, see our mobile home park investments guide.

The Basic NOI Formula

NOI = Gross Income − Operating Expenses

Simple in concept, easy to get wrong in practice. Let’s break down each side of the equation.

Step 1: Calculate Gross Income for a Mobile Home Park

Mobile home parks generate income from several sources. You need to capture all of them — and understand which are reliable versus variable.

Lot Rent (Primary Income)

The cornerstone of mobile home park income is lot rent — the monthly fee tenants pay for the space their home occupies. If a park has 80 occupied lots at $425/month average lot rent, gross lot rent income is $408,000 per year.

Lot rent is the most valuable income stream in a mobile home park because:

- It’s the most stable — tenants rarely move because relocating a manufactured home costs $5,000–$10,000 or more

- It carries the lowest expense burden — you’re responsible for the land, not the home

- It’s the income stream that drives valuation and cap rate analysis

Home Rent (Park-Owned Homes)

If the park owns and rents out homes, that rental income is included in gross income. Be careful here: park-owned homes carry significantly higher expenses and management complexity than lot-only income. Many experienced operators work to transition from park-owned homes to tenant-owned homes over time, converting home rent to lot rent and improving the quality of NOI in the process.

Other Income

- Utility income (water, sewer, trash — if billed back to tenants through sub-metering or ratio utility billing)

- Storage fees

- Laundry facilities

- Late fees and other ancillary charges

Effective Gross Income

Once you have all income sources, apply a vacancy allowance. If a park has 100 total lots and 88 are occupied, your occupancy rate is 88%. Effective gross income (EGI) = gross potential income × occupancy rate, with adjustments for any known lease concessions or credit losses.

For stabilized mobile home parks, model 5–10% vacancy. For value-add parks with significant empty lots, vacancy loss will be much higher — and closing that gap is where the upside lives.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Step 2: Identify and Calculate Operating Expenses

This is where mobile home parks diverge sharply from apartments. Because tenants own their homes in a lot-rent model, you’re not paying for roof repairs, HVAC calls, or appliance replacements. Mobile home park operating expenses are land and infrastructure focused — which is one reason expense ratios can be significantly lower than apartment properties.

Property Taxes

Typically the largest single expense line in a mobile home park. Property tax rates vary considerably by state and county. Budget 12–20% of gross income in most markets, though it can run higher in high-tax states.

Insurance

General liability and property insurance for the park’s land and infrastructure (roads, common areas, owned structures). Mobile home parks are increasingly expensive to insure, particularly in hurricane-prone states like the Carolinas and Georgia. Budget 5–8% of gross income.

Utilities (Park-Paid)

If the park doesn’t sub-meter utilities — billing tenants individually for water, sewer, and trash — this becomes the biggest variable expense. A master-metered park where the owner pays all water and sewer can see 20–30% of gross income consumed by utility costs. This is exactly why sub-metering and utility pass-through is one of the most impactful value-add plays in mobile home park investing.

Management Fees

Professional property management for mobile home parks typically runs 8–12% of gross collected income. Even if you plan to self-manage, always budget a management fee in your underwriting — it represents the true economic cost of management and prevents your analysis from being owner-dependent (and unpresentable to lenders or partners).

Maintenance and Repairs

Roads, drainage, common areas, signage, playgrounds, landscaping, and minor infrastructure repairs. For a lot-rent mobile home park, this is substantially lower than apartment maintenance — often 5–10% of gross income for a well-maintained property. Deferred maintenance parks will be higher.

Administrative Costs

Bookkeeping, property management software (platforms like Rent Manager or Rent Café), legal and compliance costs, banking fees, and general administrative overhead.

Reserves for Capital Expenditures

Water lines, sewer infrastructure, road resurfacing, electrical distribution — these are the major capital risks in mobile home park ownership. Many buyers model capital reserves separately from operating expenses, but a disciplined underwriter builds in at least $100–$200 per lot per year as a capital reserve line. This is especially important in older parks with aging infrastructure.

What Is NOT Included in NOI

Net operating income is always calculated before:

- Debt service (mortgage payments) — those are below-the-line

- Depreciation and amortization

- Income taxes

- Capital expenditures (though some underwriters include reserves)

- Owner’s personal expenses or salary

Sellers will sometimes present “adjusted NOI” that excludes a management fee (if they self-manage) or underestimates key expense lines. Always normalize the income statement to reflect true market expenses before you rely on any NOI figure for valuation.

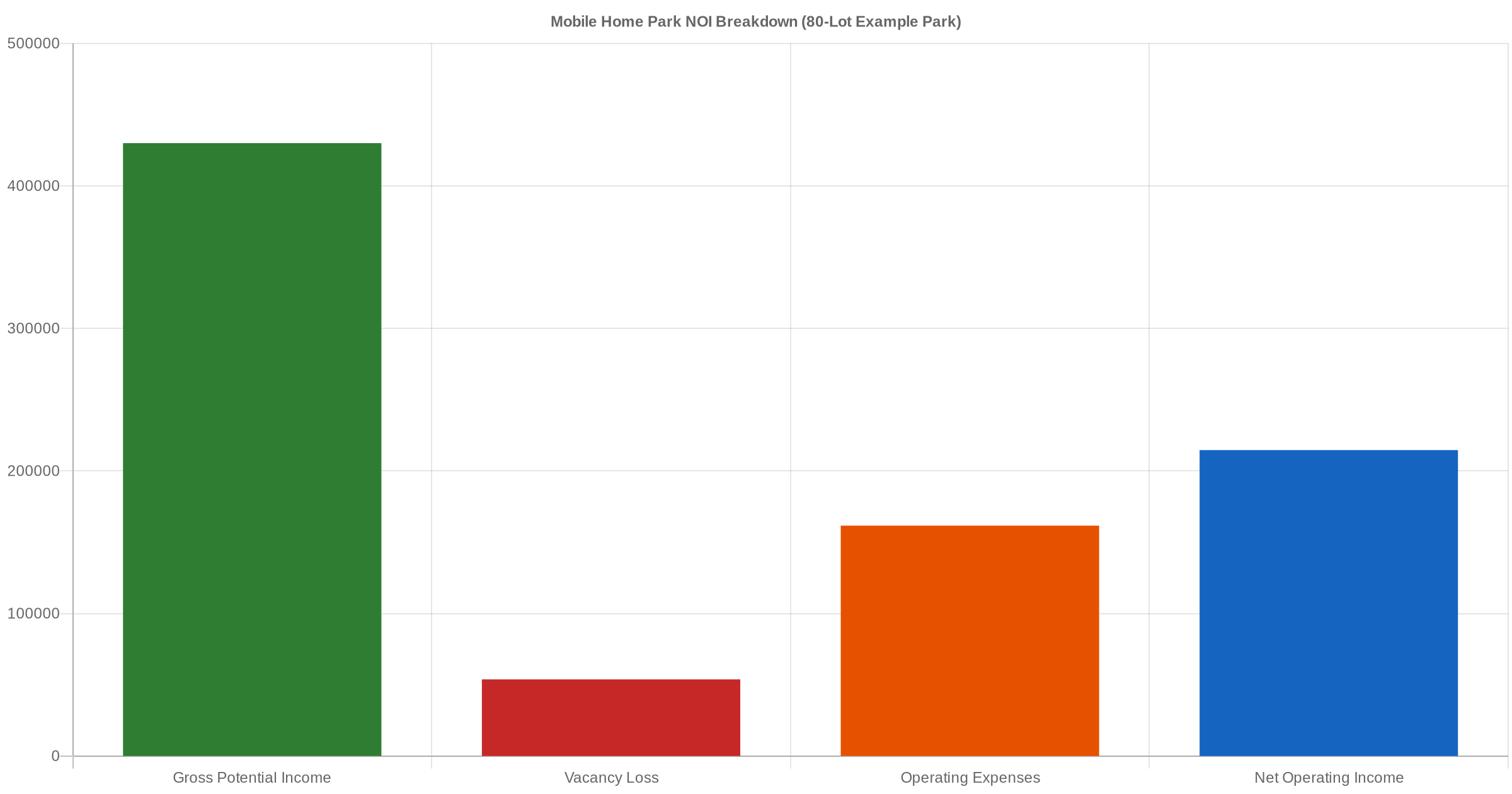

Step 3: A Real-World Mobile Home Park NOI Example

Let’s walk through a realistic 80-lot mobile home park with 70 lots occupied at $425/month average lot rent.

Gross Potential Income:

- Lot rent: 80 lots × $425/mo × 12 = $408,000

- Utility pass-through income: $18,000

- Other income: $4,000

- Gross potential: $430,000

Vacancy allowance (12.5% — 10 empty lots): −$53,750

Effective Gross Income: $376,250

Operating Expenses:

- Property taxes: $52,000 (13.8%)

- Insurance: $22,000 (5.8%)

- Management (10%): $37,625

- Maintenance and repairs: $18,000

- Utilities (park-paid): $24,000

- Administrative: $8,000

- Total operating expenses: $161,625 (42.9% expense ratio)

Net Operating Income: $376,250 − $161,625 = $214,625

A 43% expense ratio is healthy for a well-run mobile home park. Expect the typical range to fall between 35–55% depending on utility structure, management intensity, and infrastructure condition.

How NOI Drives Mobile Home Park Valuation

This is why net operating income matters so much: mobile home parks are valued on income, not comparable sales the way single-family homes are. The income capitalization formula is:

Value = NOI ÷ Cap Rate

Using our example above at a 7.5% cap rate:

- $214,625 ÷ 0.075 = $2,861,667

The same NOI at a 6.5% cap rate (a stronger market) would price at $3,303,462. At an 8.5% cap rate, $2,525,000. This cap rate sensitivity is why understanding local market cap rates is so critical before you underwrite any deal. See our detailed breakdown of mobile home park cap rates for current benchmarks by region.

More importantly: every dollar of NOI you add — through lot rent increases, filling vacant lots, or reducing utility expenses — multiplies directly into property value at the prevailing cap rate. That’s the compounding leverage that makes mobile home park value-add investing so compelling compared to other commercial asset classes.

Common Mobile Home Park NOI Mistakes to Avoid

Trusting Seller-Provided Financials Without Verification

Always verify income with 12–24 months of bank statements and a current rent roll. Self-managed mobile home parks frequently have informal income, unreported vacancies, or expense categories that don’t appear in the P&L. Verify everything independently.

Forgetting to Normalize the Management Fee

If you’re buying a park the seller has managed themselves for years, their NOI will look better than it actually is for a third-party operator or future buyer. Always underwrite a market-rate management fee — typically 8–10% of gross — even if you plan to self-manage initially.

Ignoring Deferred Capital Items

An aging water distribution system or deteriorating gravel roads won’t appear in operating expenses — until they fail catastrophically. A thorough due diligence process should identify deferred capital items and either price them into your offer or hold sufficient capital reserves. For a structured approach to this process, see our mobile home park underwriting guide.

Conflating Gross Rents with Effective Gross Income

Buyers occasionally calculate NOI off gross potential rents without properly adjusting for actual occupancy, tenant credits, or non-collectibles. Always use effective gross income — what the park actually collects — as your starting point.

Ignoring Occupancy Trends Over Time

A park with declining occupancy but stable or rising NOI can look healthy on paper while the fundamentals deteriorate underneath. If lot counts are shrinking but rents are being pushed hard, the NOI trend is masking a deeper problem. Always look at NOI alongside occupancy trends over multiple years.

Final Thoughts

Net operating income is the engine that drives every critical number in a mobile home park investment — purchase price, financing terms, cash-on-cash returns, and eventual exit value. Getting comfortable building, stress-testing, and normalizing your own NOI model is one of the most valuable skills you can develop as a mobile home park investor.

The math isn’t complicated. But the judgment calls — which expenses to include, how to normalize management, how to account for deferred infrastructure — require experience and a willingness to look hard at the numbers rather than accept them at face value.

For more on how mobile home park investments generate returns across different market conditions, visit our mobile home park investments resource page.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.