If you’ve identified a mobile home park worth buying, financing is what turns intent into ownership. And yet it’s one of the most misunderstood parts of the acquisition process — especially for investors coming from single-family or multifamily backgrounds, where lender options are more standardized.

Mobile home park financing operates in its own lane. There are distinct programs, eligibility requirements, and trade-offs depending on the size of the park, its occupancy, utility infrastructure, and your experience as an operator. Understanding the landscape before you make an offer can mean the difference between a smooth closing and a deal that falls apart.

This guide breaks down every major loan type available to mobile home park investors in 2026 — who they’re best for, what to expect on rates and leverage, and where each option fits in a real acquisition strategy.

Agency Debt: Fannie Mae and Freddie Mac Programs

For stabilized mobile home parks that meet program eligibility, agency debt from Fannie Mae or Freddie Mac is typically the most attractive financing available. These are non-recourse loans with competitive rates and long amortization schedules — the gold standard for acquisitions of quality assets.

Fannie Mae Manufactured Housing Community Loans require a minimum loan amount of $3 million and a minimum of 50 pad sites. Properties must be stabilized and professionally managed, and no more than 25% of homes can be park-owned. Maximum LTV is 80% for acquisitions and 75% for cash-out refinances. Terms run up to 30 years, with both fixed and variable rate options.

Freddie Mac’s Manufactured Housing Community program offers five-, seven-, and ten-year terms with amortizations up to 30 years. For 7-year amortizing loans, the maximum LTV is 80% with a minimum debt service coverage ratio (DSCR) of 1.25x. Freddie requires a minimum of five pad sites, though loan minimums from approved lenders tend to push this to much larger parks in practice.

The catch: both agencies have strict property conditions — city water and city sewer are strongly preferred, POH (park-owned home) ratios are scrutinized, and occupancy must typically be above 80%. If your target park has well and septic or a high park-owned home count, expect to look elsewhere for financing.

For first-time buyers, the operator experience requirement is worth noting — at least one key principal typically needs a verifiable track record operating manufactured housing communities. This is where a mentor relationship or co-GP structure can help bridge the gap.

CMBS Loans for Mobile Home Parks

Commercial Mortgage-Backed Securities (CMBS) loans — sometimes called conduit loans — are another non-recourse option for larger mobile home parks. They’re originated by banks or CMBS lenders, pooled with other commercial loans, and sold as securities on the secondary market.

For mobile home park investors, CMBS loans typically offer:

- LTV up to 70–75% for stabilized assets

- 10-year fixed terms with 25–30 year amortization

- Non-recourse structure (with standard carve-outs for fraud, environmental, etc.)

- Rates typically in the 6–7.5% range depending on market conditions

The tradeoff with CMBS is flexibility. These loans come with significant prepayment penalties (defeasance or yield maintenance), meaning you’re locked in. If your business plan involves a 3–5 year flip or value-add exit, CMBS is likely not the right fit. But for a long-term hold on a stabilized asset, it can be an excellent structure.

Community Bank and Conventional Loans

For mobile home parks that don’t qualify for agency or CMBS programs — parks under $3M, rural markets, parks with well/septic utilities, or operators without an institutional track record — community banks are often the first call.

Community banks that understand the asset class will lend on mobile home parks at:

- LTV up to 70–75%

- 5–7 year terms with 20–25 year amortization

- Recourse (personal guarantee required)

- Rates: typically SOFR-based or prime-linked, often 6.5–8.5% in the current rate environment

The advantage of community banks is flexibility. They underwrite based on local relationships and common sense, not a rigid national program matrix. A bank that has previously financed mobile home parks in your target market will move faster and ask fewer questions than an agency lender.

The key is finding a bank with mobile home park experience. Loan officers unfamiliar with the asset class will often misprice risk or decline entirely. Ask your broker network, local real estate attorneys, and other operators who their preferred lenders are before calling cold.

If you’re looking for guidance on how to structure your underwriting before approaching a lender, our step-by-step NOI calculation guide walks through exactly what lenders will scrutinize.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

SBA Loans: 7(a) and 504 Programs

The Small Business Administration’s loan programs are an underutilized option for mobile home park buyers, particularly for smaller parks or owner-operators who intend to manage the property themselves.

SBA 7(a) loans offer up to $5 million with LTVs up to 85–90% and terms up to 25 years. Rates are variable, typically tied to prime plus 2–3%, and loans are partially guaranteed by the SBA. The catch: the borrower must actively manage the business (not a pure passive hold), and SBA loans require a personal guarantee.

SBA 504 loans pair a conventional lender (50%) with an SBA Certified Development Company (CDC, 40%) and your down payment (10%). Effective LTVs reach 80–90%, and the CDC portion carries a below-market fixed rate — making this one of the most cost-efficient structures for owner-operators in the $1M–$15M range.

SBA financing works best for the operator who is buying a mobile home park as an operating business, not purely as a real estate investment. It’s worth consulting an SBA-experienced lender early in your search if you fit this profile.

Seller Financing

For off-market acquisitions — which is where the best mobile home park deals are found — seller financing is often on the table, particularly when dealing with retirement-age owners who don’t need a large cash-out event.

Seller-financed deals typically feature:

- LTV of 70–90% (fully negotiated)

- Interest rates of 4–7% (often below bank rates)

- 5–10 year terms with balloon payments or full amortization

- No bank approval process, no appraisal delays

A seller note can be structured in many ways — as a first lien, as subordinate financing behind a bank loan, or as a wraparound mortgage. In competitive off-market environments, offering seller financing terms can be a dealmaker when an all-cash offer isn’t feasible.

See our guide on finding off-market mobile home parks for strategies to reach sellers who are open to creative terms.

Bridge Loans and Hard Money

Bridge loans fill the gap when a property doesn’t yet qualify for permanent financing — typically because of low occupancy, deferred maintenance, or a recent acquisition that needs stabilization before a bank will lend.

Bridge/hard money loans for mobile home parks typically come with:

- LTV of 60–70% (based on as-is value)

- Rates of 9–13%

- Terms of 12–36 months

- Interest-only structure during the hold period

Bridge loans are a tool, not a strategy. They’re designed to be paid off — either through a value-add-driven refinance into permanent financing or an outright sale. The key question is: do you have a clear path to the exit within the bridge term? If not, extend your bridge or reconsider the deal.

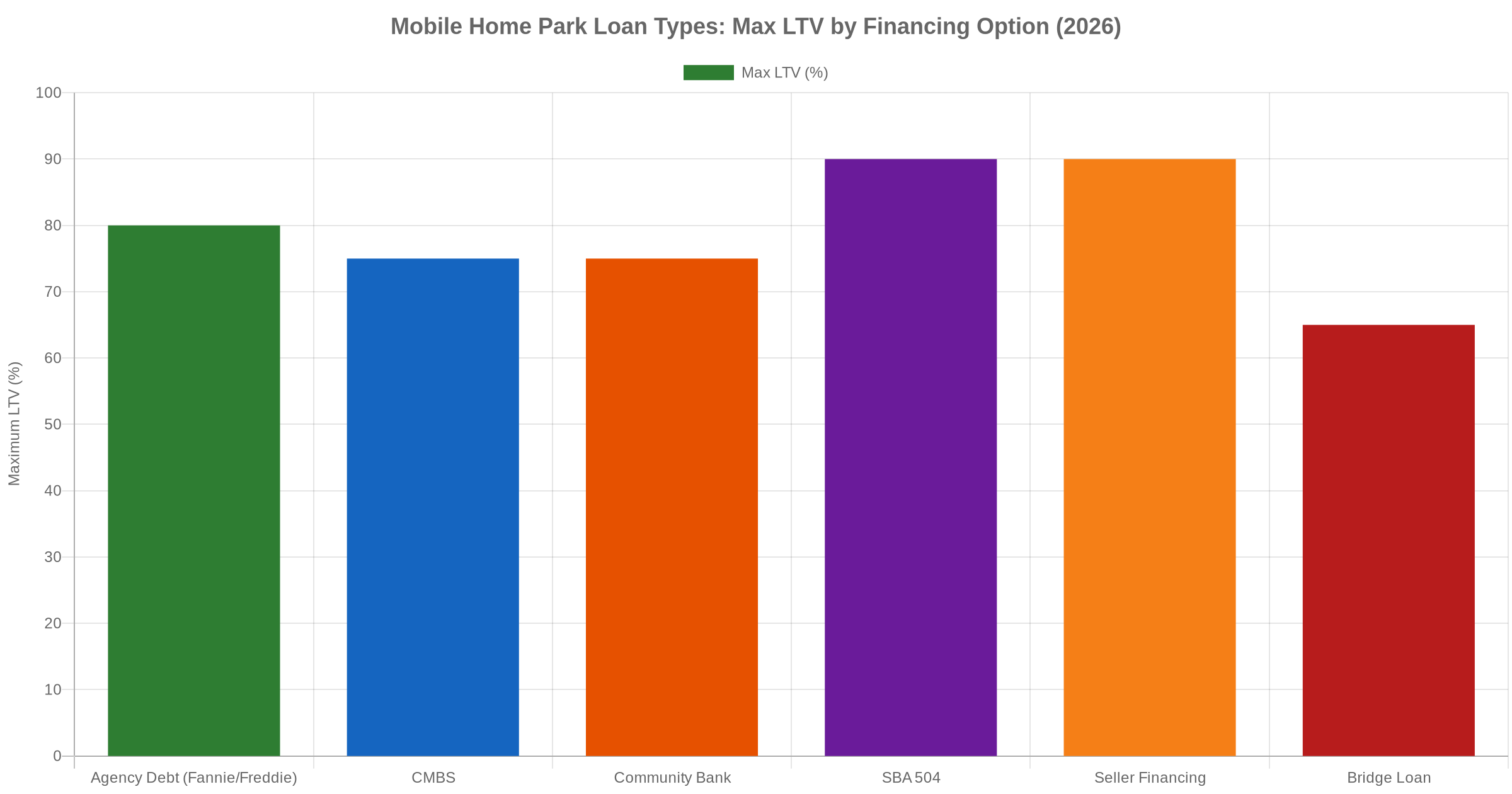

Side-by-Side Comparison: Every Loan Type at a Glance

| Loan Type | Max LTV | Typical Rate | Term | Recourse? | Best For |

|---|---|---|---|---|---|

| Agency (Fannie/Freddie) | 80% | 6.0–7.0% | Up to 30 yr | No | Stabilized 50+ pad parks |

| CMBS / Conduit | 75% | 6.5–7.5% | 10 yr / 25–30 am | No | Long-term holds |

| Community Bank | 75% | 6.5–8.5% | 5–7 yr / 20–25 am | Yes | Smaller parks, rural markets |

| SBA 7(a) | 85–90% | Prime + 2–3% | Up to 25 yr | Yes | Owner-operators |

| SBA 504 | 90% | Below-market fixed | 20–25 yr | Yes | Owner-operators <$15M |

| Seller Financing | 70–90% | 4–7% | 5–10 yr (negotiated) | Negotiated | Off-market acquisitions |

| Bridge / Hard Money | 65–70% | 9–13% | 12–36 months | Yes | Turnaround / value-add plays |

How Passive Investors Are Shielded from Financing Risk

If you’re investing as a limited partner in a mobile home park syndication, it’s worth understanding how deal-level financing affects you — even though you won’t be signing any loan documents yourself.

In a typical syndication, the GP (general partner or operator) secures financing at the entity level. As an LP, your equity sits behind the debt. That means the GP’s financing decisions directly affect your returns: a highly leveraged deal amplifies both upside and downside. A bridge loan with a short refinance window introduces timeline risk that could delay distributions or create a capital call situation if the market shifts.

When evaluating a mobile home park syndication, ask the GP specifically:

- What loan type did you use, and why?

- Is the debt fixed or floating rate?

- What happens if you can’t refinance at the planned exit?

- Is there a rate cap in place on floating-rate debt?

Our guide on mobile home park due diligence covers financing-related questions you should ask before committing capital to any deal.

Conclusion

There’s no single “best” financing option for mobile home park investing — the right loan depends on your park’s size and condition, your experience level, your business plan timeline, and your risk tolerance. Agency debt wins on cost and leverage for institutional-quality assets. Community banks provide flexibility for smaller deals. Seller financing opens doors that bank financing can’t. And bridge loans buy you time to execute a value-add play.

The investors who win at mobile home park acquisitions are the ones who know these options cold before they make an offer — so they’re not scrambling to understand their financing options after a deal is under contract.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Frequently Asked Questions

What credit score do I need to finance a mobile home park?

Agency lenders (Fannie/Freddie) generally require a minimum credit score of 680–700 for principals. Community banks vary, but most want 660+. SBA loans typically require 680+. Bridge lenders focus more on the asset and exit plan than personal credit. Keep in mind that for larger loans, liquidity and net worth requirements often matter as much as credit score.

Can I use an FHA or conventional residential mortgage to buy a mobile home park?

No. Mobile home parks are commercial real estate and require commercial financing. FHA, VA, and conventional residential mortgages are for owner-occupied single-family homes and small multifamily properties (up to 4 units). A mobile home park — even a small one — requires a commercial loan.

How much down payment is typically required to buy a mobile home park?

It depends on the loan type. Agency debt requires 20–25% down. Community banks typically want 25–35% down. SBA 504 can be done with as little as 10% down for owner-operators. Seller financing is fully negotiable — some deals close with 10% down, others require 30%+. The average across most acquisition types in 2026 is 25–30% equity at close.

Do mobile home parks qualify for Fannie Mae or Freddie Mac loans?

Yes — but only if the park meets specific criteria. Fannie Mae requires a minimum of 50 pad sites, city water and sewer preferred, a 3–5 star property rating, and no more than 25% park-owned homes. Freddie Mac requires a minimum of five pad sites but has similar quality and management standards. Many smaller or rural parks won’t qualify and will need community bank or seller financing instead.

What is the minimum loan amount for agency debt on a mobile home park?

Fannie Mae has a stated minimum of $3 million for its Manufactured Housing Community program. Freddie Mac’s minimum in practice is similar, though program terms allow smaller loans. In reality, most agency lenders prefer to write loans of $5M+ due to the fixed overhead of originating and servicing these loans. Below that threshold, a community bank or credit union is typically the better path.

Get the top 20 lessons from two decades of mobile home park investing — free.