Inflation is a passive investor’s quiet adversary. It doesn’t announce itself — it just steadily chips away at the purchasing power of your returns. A 6% annual distribution sounds great until inflation is running at 5%. What looks like a solid gain is, in real terms, barely keeping pace.

This is why savvy investors look beyond nominal yields and ask a more important question: does this asset keep pace with — or outrun — inflation? For mobile home park investing, the answer is a consistent yes, and the mechanics behind it are worth understanding before you commit capital as a passive investor.

Why Inflation Matters More Than Most Passive Investors Realize

Fixed-income investments — bonds, CDs, money markets — are notoriously vulnerable to inflation. When CPI runs hot, fixed payments lose real value. Even dividend stocks can lag if the underlying business can’t pass rising costs to customers.

Real assets are different. Hard assets like real estate have a natural tendency to appreciate alongside inflation because replacement costs rise with the price of materials and labor. But not all real estate is equal in this regard. Apartment landlords, for example, face lease rollover risk — they can only raise rents when a lease expires, and in competitive markets, that pricing power can be limited.

Mobile home parks operate differently, and those structural differences matter enormously for inflation protection.

What Makes an Asset a True Inflation Hedge?

A genuine inflation hedge must do at least one of the following:

- Generate cash flows that grow with or faster than inflation

- Appreciate in value as the general price level rises

- Offer tax benefits that preserve real after-tax returns

The best assets do all three. Mobile home parks check all three boxes, which is why high-income professionals increasingly allocate to this asset class as part of a diversified, inflation-resistant portfolio.

How Lot Rent Creates a Built-In Inflation Escalator

The core of the mobile home park inflation hedge is lot rent — the monthly fee tenants pay to lease the land beneath their home. Unlike apartment rents, which require vacancy and re-leasing to reset, lot rent can be increased with proper notice to current tenants on an annual basis. Most well-operated mobile home parks raise lot rents 3–8% per year regardless of market conditions.

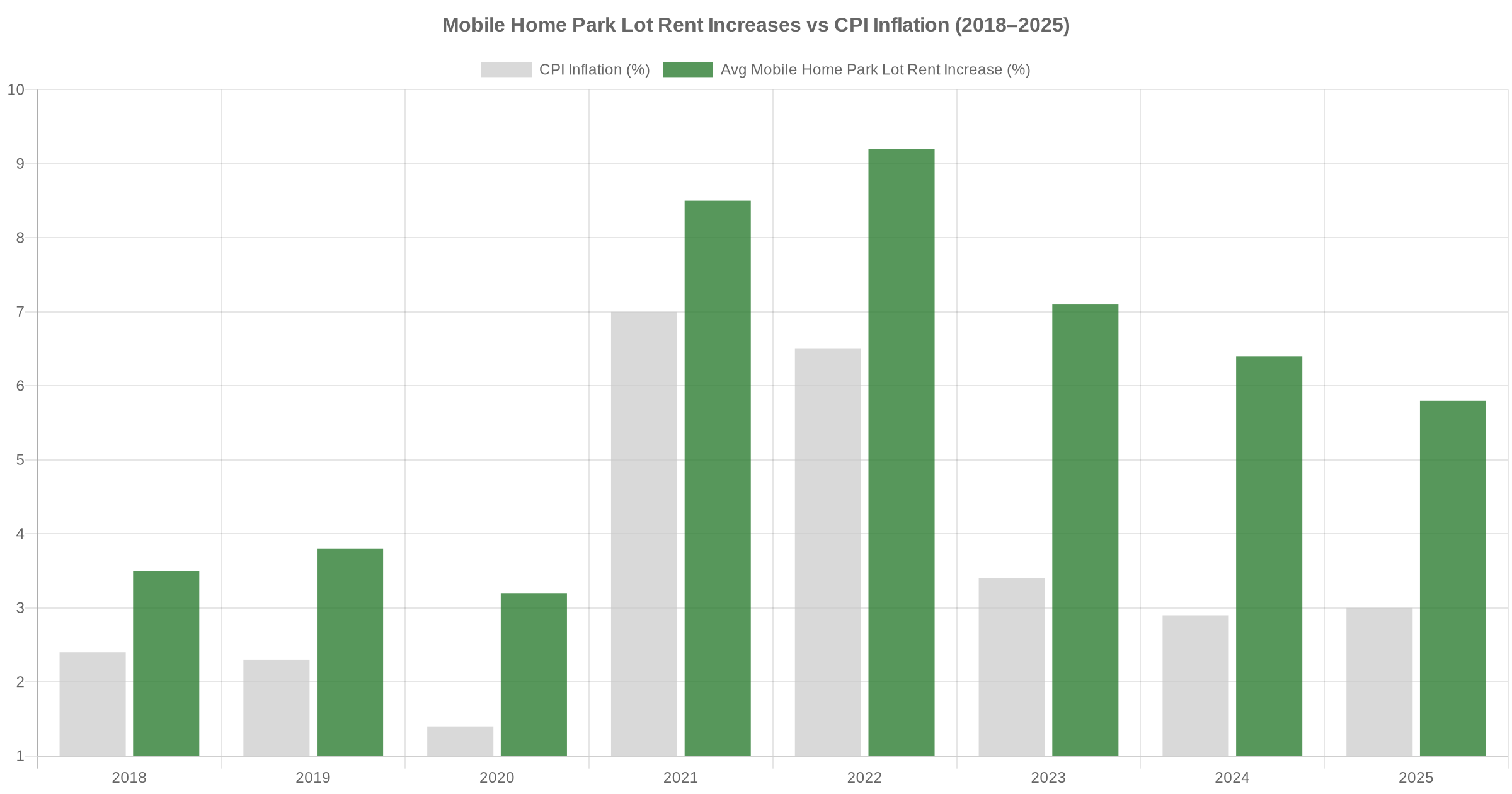

The chart below illustrates the historical relationship between CPI inflation and average lot rent increases at mobile home parks across the Southeast and Midwest:

Notice the pattern: in low-inflation years (2018–2020), lot rent increases still ran 1–2 points above CPI. When inflation spiked in 2021–2022, experienced operators had room to push lot rents by 8–9% — aggressively, but not unusually. Tenants, who had signed leases at below-market rates for years, largely absorbed the increases because their cost to move far exceeds the incremental rent bump.

The Tenant Stickiness Factor — Why Rent Increases Actually Stick

Here’s the dynamic that makes the mobile home park inflation hedge structurally durable: mobile homes are, paradoxically, not very mobile.

Moving a manufactured home off its foundation — disconnecting utilities, hiring a licensed transporter, and reinstalling at a new site — typically costs $5,000 to $10,000 or more, and that’s assuming another mobile home park with available lots exists nearby. It usually doesn’t. New mobile home parks haven’t been built in meaningful quantities since the 1980s due to zoning restrictions. The supply of lots is effectively fixed.

This creates extraordinary tenant retention. Industry-wide, annual tenant turnover at mobile home parks hovers around 2–4%, compared to 40–50%+ at conventional apartment communities. Low turnover means:

- No vacancy drag between tenants

- No unit rehabilitation costs between leases

- Consistent rent collection month over month

- Real pricing power when raising lot rents annually

For passive investors evaluating passive investing in mobile home parks, this tenant retention profile is what allows operators to deliver stable distributions even in inflationary environments where other property types face elevated vacancies and concessions.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Supply Constraints Amplify the Hedge

No discussion of mobile home parks and inflation is complete without addressing supply. The fundamental law of supply and demand means that inflation protection is strongest when supply cannot expand to meet rising prices.

For mobile home parks, supply constraints are structural and largely permanent. Zoning laws in most municipalities prohibit new mobile home park development — often explicitly. Existing mobile home parks operate under grandfathered entitlements that would be extraordinarily difficult to obtain today. As a result, the national inventory of mobile home park lots has been flat or declining for over two decades even as demand for affordable housing has surged.

This supply inelasticity means that as inflation increases replacement costs for new affordable housing options, mobile home parks become more valuable, not less. Operators with well-located, city-utilities-connected mobile home parks in growing MSAs have genuine pricing power that most real estate owners can only dream about.

How Passive Investors Capture the Inflation Hedge

As a limited partner in a mobile home park syndication, you don’t operate the park — you benefit from the operator’s ability to raise lot rents and manage expenses. The inflation hedge flows through to you in three primary ways:

1. Growing Cash Distributions

As lot rents increase annually, net operating income grows — often faster than the rate of inflation because most operating expenses (property taxes, insurance, management fees) don’t scale proportionally with small rent bumps. This NOI growth translates into higher distributions over the hold period. A deal projecting 6% cash-on-cash in year one may deliver 8–9% by year four simply through rent escalation.

2. Appreciation at Exit

Mobile home park valuations are driven by NOI divided by a cap rate. When NOI grows because lot rents have kept pace with inflation, the asset’s market value rises in kind. In an inflationary environment, both the NOI growth and cap rate compression (as institutional demand for mobile home parks increases) work in the passive investor’s favor at exit.

3. Tax Benefits That Preserve Real Returns

Bonus depreciation, cost segregation, and pass-through losses allow limited partners to shelter a significant portion of their annual distributions from current income tax. This tax efficiency is particularly valuable during inflationary periods when nominal gains would otherwise push investors into higher brackets. You can learn more about how these benefits work in our breakdown of tax benefits of mobile home park investing as a limited partner.

Comparing Mobile Home Parks to Other Inflation Hedges

Investors seeking inflation protection typically consider several asset classes. Here’s how mobile home parks stack up:

- TIPS (Treasury Inflation-Protected Securities): Protect principal from inflation but offer minimal real yield, no tax efficiency, and zero appreciation upside.

- Gold: A classic store of value but generates no cash flow. Purely a speculative inflation hedge.

- Apartments: Real estate with cash flow, but higher tenant turnover, greater capex requirements, and lease rollover risk limit pricing power relative to mobile home parks.

- Self-storage: Good cash flow and pricing flexibility, but month-to-month leases create more volatility and supply has expanded significantly in recent years. See our mobile home park vs. self-storage comparison for a deeper look.

- Mobile home parks: Stable cash flow, annual rent escalation, structural supply constraints, low tenant turnover, and favorable tax treatment. The combination is difficult to match.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

What Passive Investors Should Look For

Not all mobile home parks are equally positioned to deliver inflation protection. As you evaluate opportunities, prioritize these characteristics:

- Lot rents below market rate: A mobile home park with lot rents 20–30% below comparable communities in the area has built-in rent growth potential regardless of inflation. The best deals have a rent escalation story baked in from day one.

- City water and sewer: Parks on private wells or septic systems face unpredictable infrastructure costs that can erode the inflation hedge. Municipal utilities pass cost increases to municipalities, not to the operator.

- High occupancy with tenant-owned homes: When tenants own their homes (rather than the park owning them), the operator has maximum pricing power and minimal capex exposure. This is the cleanest inflation hedge structure.

- Markets with strong demand: Mobile home parks near growing metros with limited affordable housing alternatives have the most durable pricing power over time.

The Bottom Line for Passive Investors

Inflation doesn’t have to be the enemy of your investment returns. Mobile home parks — with their annual lot rent escalations, structurally constrained supply, sticky tenant base, and tax efficiency — are among the most resilient inflation hedges available to passive investors in 2026.

The key is choosing the right operator and the right deal. A well-underwritten mobile home park in a growing market with below-market rents is positioned to grow its distributions in real terms even as prices rise across the broader economy.

If you want to learn more about what mobile home park passive investing looks like in practice — how deals are structured, what returns to expect, and what questions to ask — we’re happy to share what we’ve seen across two decades of acquiring and operating parks across the Southeast and Midwest. Reach out through our contact page and we’ll set up a conversation.

Why 2026 Is a Particularly Strong Moment for This Thesis

Several macroeconomic conditions in 2026 are reinforcing the mobile home park inflation hedge thesis. Elevated tariffs on building materials — particularly steel, lumber, and imported fixtures — have pushed new construction costs to record highs. Estimates suggest tariff-related increases have added $15,000–$25,000 or more to the cost of new residential construction. For affordable housing alternatives, this has made new manufactured homes and apartment development meaningfully more expensive, further widening the gap between mobile home park lot rents and their replacement-cost equivalents.

At the same time, interest rates remain elevated by historical standards, compressing new development activity across every residential category. Fewer new affordable housing units are being built. More workforce-income households are seeking mobile home park residency as a cost-effective alternative to apartment living. Demand is rising while supply remains structurally constrained — exactly the conditions that amplify the mobile home park inflation hedge for existing owners and their investors.

Frequently Asked Questions

Are mobile home parks a good inflation hedge in 2026?

Yes. Mobile home parks are widely considered one of the most effective inflation hedges in real estate. Annual lot rent escalations (typically 3–8% per year), structural supply constraints, and extraordinary tenant retention create durable pricing power that most asset classes lack. Elevated construction costs and persistent housing affordability pressures in 2026 reinforce these dynamics further.

How do mobile home park lot rent increases compare to CPI inflation historically?

At well-operated mobile home parks, lot rent increases have historically tracked 1–2 percentage points above CPI in normal years. Operators with below-market rents have pushed increases of 8–9% during inflationary spikes without triggering significant resident turnover — because residents face $5,000–$10,000+ moving costs and an extremely limited supply of alternative lots.

Why don’t mobile home park tenants leave when rents increase?

Moving a manufactured home requires a licensed transporter, utility disconnection and reconnection, and securing a new site — costing $5,000 to $10,000 or more. Since new mobile home parks haven’t been built in meaningful quantities since the 1980s, alternative lots are scarce. Most residents find it more economical to absorb an annual lot rent increase. This dynamic produces the industry’s famously low 2–4% annual turnover rate, compared to 40–50%+ at conventional apartment communities.

What role does supply constraint play in mobile home park inflation protection?

Supply constraint is the most important structural feature of this hedge. Competing housing assets can eventually be built to absorb rising demand — but mobile home park supply is frozen by decades of restrictive zoning. There is no supply response to rising prices, which means existing mobile home park owners retain genuine pricing power regardless of broader real estate cycle dynamics.

How does mobile home park depreciation help passive investors during inflationary periods?

Bonus depreciation and cost segregation allow limited partners to shelter a significant portion of annual distributions from current income tax. During inflationary periods this is especially valuable: inflation pushes nominal returns higher, which would ordinarily push investors into higher brackets. Accelerated depreciation offsets those paper gains, preserving real after-tax returns. In many deals, passive investors receive K-1 losses in early years that shelter both distribution income and other passive income from their portfolios.

Get the top 20 lessons from two decades of mobile home park investing — free.