If you’re comparing real estate asset classes, two names keep rising to the top: mobile home parks and self-storage. Both are niche, recession-resilient, and have drawn significant institutional capital over the past decade. Both were historically dominated by mom-and-pop operators — which means fragmented ownership and motivated sellers. But beyond the surface-level similarities, these two asset classes are fundamentally different investments, and understanding those differences matters a lot before you commit capital.

This guide breaks down mobile home park investing vs. self-storage side by side — covering cap rates, management intensity, tenant dynamics, financing, and long-term return potential.

Why Investors Are Comparing These Two Asset Classes

Mobile home parks and self-storage emerged as investor darlings for overlapping reasons: low operating costs relative to gross income, demand that holds up in downturns, and operational simplicity compared to multifamily. Both are “land plays” at their core — you’re primarily investing in the dirt and the infrastructure, not the structures themselves.

But the similarities mostly end there. Once you dig into the mechanics, mobile home park investing and self-storage are built on very different economic foundations.

The Case for Self-Storage

Self-storage has several things genuinely going for it:

- Simple operations: No tenants living on-site means no midnight maintenance calls, no habitability issues, no tenant-landlord regulations to navigate.

- Month-to-month leases: The flexibility to raise rents frequently without lease renewal friction is a real advantage in inflationary environments.

- Low physical maintenance: Metal storage buildings are durable and relatively inexpensive to maintain compared to residential properties.

- Strong long-term REIT performance: Self-storage REITs — Public Storage, Extra Space Storage, CubeSmart — have delivered competitive total returns over the past two decades.

The risks are real too. Institutional competition is now fierce in most major markets. Oversupply has emerged in dozens of markets where new development was easy to permit. And those month-to-month leases cut both ways: when the economy softens, tenants cancel quickly. Self-storage vacancy can spike faster than almost any other asset class in a downturn.

The Case for Mobile Home Park Investing

Mobile home park investing is built on a structurally different foundation — and in several meaningful ways, it offers advantages that self-storage simply cannot match.

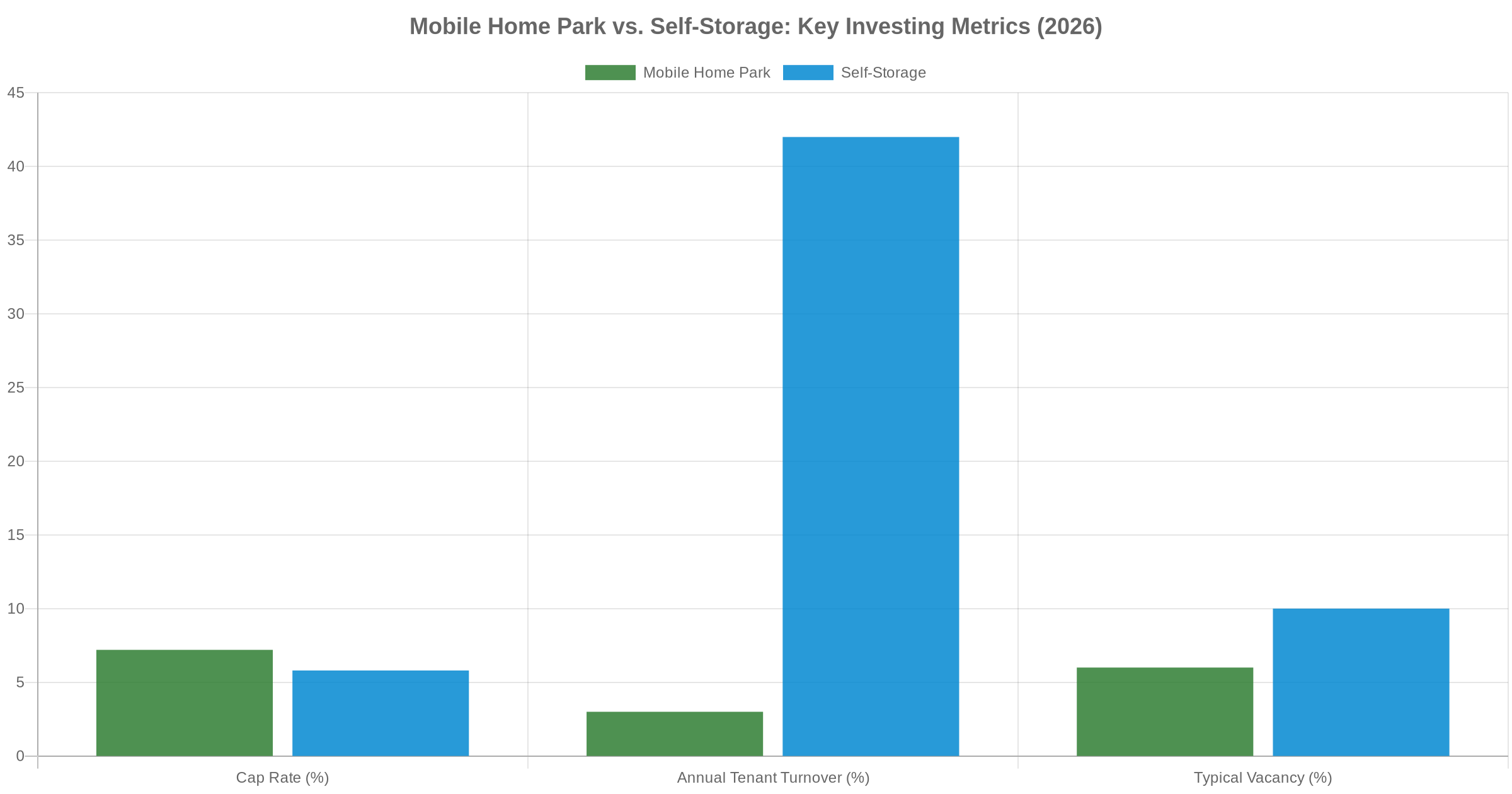

The most important structural advantage: tenants own their homes. A mobile home park operator is not renting units — they are renting land. The residents own manufactured homes that sit on that land, and moving one costs $5,000–$15,000 or more. That economic friction creates tenant retention unlike anything else in real estate. Annual turnover in well-run mobile home parks typically runs 2–4%, versus 40–50% or more for self-storage units.

That stability has profound effects on cash flow predictability, operating costs, and long-term asset value.

Additional structural advantages of mobile home park investments:

- Supply constraints: New mobile home parks are almost never permitted. Zoning opposition is fierce, and approvals are nearly impossible in most municipalities. The existing supply is essentially fixed — which creates long-term pricing power for current owners.

- Affordable housing tailwind: Manufactured housing is often the most cost-effective housing option in markets where single-family rents exceed $1,600–$2,000 per month. As affordability pressures intensify nationally, demand for mobile home park lots is likely to grow, not shrink.

- Value-add runway: Many mobile home parks still carry below-market rents, master-metered utilities, and operational inefficiencies left by decades of absentee management. For an active operator, there is genuine room to create value — not just ride market appreciation.

- Less competition below 200 lots: The large institutional players — Sun Communities, Equity LifeStyle Properties, RHP Properties — focus on larger communities. Smaller operators face significantly less competition for acquisitions in the 50–150 lot range.

For historical context on how the asset class has performed through market cycles, see: Mobile Home Park Investment Returns: What the Data Actually Shows.

Before you invest in any mobile home park — as an active buyer or passive LP — you need to know how to evaluate the deal. The MHP Due Diligence Playbook includes 10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of analyzing a mobile home park acquisition with confidence.

Side-by-Side Comparison: Key Metrics

Cap Rates and Returns

Cap rates for stabilized mobile home parks in secondary markets typically range from 6–8%, with value-add deals sometimes underwriting at 5–6% on current income but projecting meaningful upside through rent increases and expense recapture. Self-storage cap rates have compressed to the 5–6.5% range in most markets as the asset class has become more institutionalized.

Mobile home parks often offer slightly higher going-in yields, particularly in markets that have not yet seen heavy institutional interest — which is still most of the country outside Sun Belt gateway markets.

Financing and Capital Requirements

Both asset classes can access agency financing (Fannie Mae, Freddie Mac) for stabilized properties, though mobile home parks have historically had more options at the community bank and regional bank level. Mobile home park loans typically require 20–30% down; self-storage financing is similarly structured.

One key difference: underwriting a mobile home park involves assessing factors — utility infrastructure, home title status, and lot occupancy versus physical occupancy — that self-storage deals do not require. The learning curve is steeper for mobile home parks, but so is the competitive moat for operators who master it.

Management Intensity

Self-storage wins this category decisively. A well-configured self-storage facility can operate nearly hands-off with automated gate access, online rentals, and minimal on-site staff. Mobile home parks require on-site or regional management to handle tenant relations, maintenance coordination, home sales, and regulatory compliance. That said, compared to apartments, mobile home parks are still relatively low-intensity — operators are not dealing with unit maintenance, appliance repairs, or interior turnover costs.

Recession Resilience

Both asset classes hold up well in downturns, but for different reasons. Self-storage benefits because people downsize and businesses cut overhead. But units can vacate quickly when people are truly under financial stress.

Mobile home park resilience is more structural. Mobile home parks have historically performed well during recessions because residents face significant logistical barriers to leaving — not just financial ones. When you own a home that costs $10,000 to move and is worth $8,000, paying $400 per month in lot rent is still the best available option. That is a fundamentally different risk profile than a self-storage unit that can be cleared out in an afternoon.

Long-Term Appreciation and Exit

Self-storage assets are valued primarily on income, and significant cap rate compression has already occurred in most markets. The easy gains have largely been made. Mobile home parks — particularly smaller communities — still have meaningful cap rate compression runway as more professional buyers enter the market and as operators professionalize formerly neglected assets.

Exit liquidity is stronger for self-storage in gateway markets. But mobile home parks in the 100–250 lot range have a growing and active buyer pool, including regional operators, private equity, and REIT aggregators looking to build scale.

Which One Is Right for You?

The honest answer depends on your goals, risk tolerance, and operational capacity.

Self-storage may be a better fit if:

- You want truly passive operations and minimal management complexity

- You are in a market with genuine storage demand and limited new supply pipeline

- You prefer a simpler due diligence process and faster path to stabilization

Mobile home park investing may be a better fit if:

- You want higher tenant retention and more predictable long-term cash flow

- You are interested in value-add opportunities with genuine operational upside

- You see affordable housing as a multi-decade structural tailwind worth positioning around

- You want to invest in an asset class that still has pricing inefficiency — especially below 150 lots

For passive investors who want exposure to mobile home park returns without operating a community themselves, there are options — funds, syndications, and joint ventures with experienced operators. If you are curious about learning more, feel free to reach out and learn more about mobile home park investing.

The Bottom Line

Both mobile home parks and self-storage are legitimate, defensive real estate investments. But mobile home park investing offers a combination of tenant stability, supply constraints, affordable housing demand, and value-add potential that is difficult to replicate in self-storage — especially now that self-storage has been heavily institutionalized and cap rates have compressed accordingly.

If you are evaluating either asset class, the most important thing is doing the analytical work upfront: understanding the local market, stress-testing the income, and knowing exactly what you are buying before you commit capital.

Get the MHP Due Diligence Playbook — the complete system for analyzing mobile home park acquisitions with confidence. Includes 10 video modules, a 55-page master checklist, and 9 ready-to-use templates. Everything you need to evaluate a deal the right way.