Two days ago, something quietly significant happened in Washington — and most mobile home park operators haven’t fully processed it yet.

On April 22, 2026, FHFA Director Bill Pulte and HUD Secretary Scott Turner announced that Fannie Mae and Freddie Mac are immediately implementing new credit scoring models — VantageScore and FICO 10T — that count rental payment history and utility payments toward a borrower’s credit score.

“Effective immediately, Fannie Mae and Freddie Mac are accepting new, modern credit scores that give American homebuyers the credit they deserve for paying their rent,” Pulte stated.

For most real estate sectors, this is moderately interesting news. For mobile home park operators — especially those wrestling with aging home stock — it could be a genuine turning point.

Here’s the problem it exposes, and why it matters right now.

The Aging Home Stock Crisis Nobody Talks About

Walk through most mobile home parks built before 1995 and you’ll see the same thing: single-wide homes with original roofing, original plumbing, and a resale value somewhere between “not much” and “pay someone to haul it.” The American manufactured housing inventory is old — and getting older.

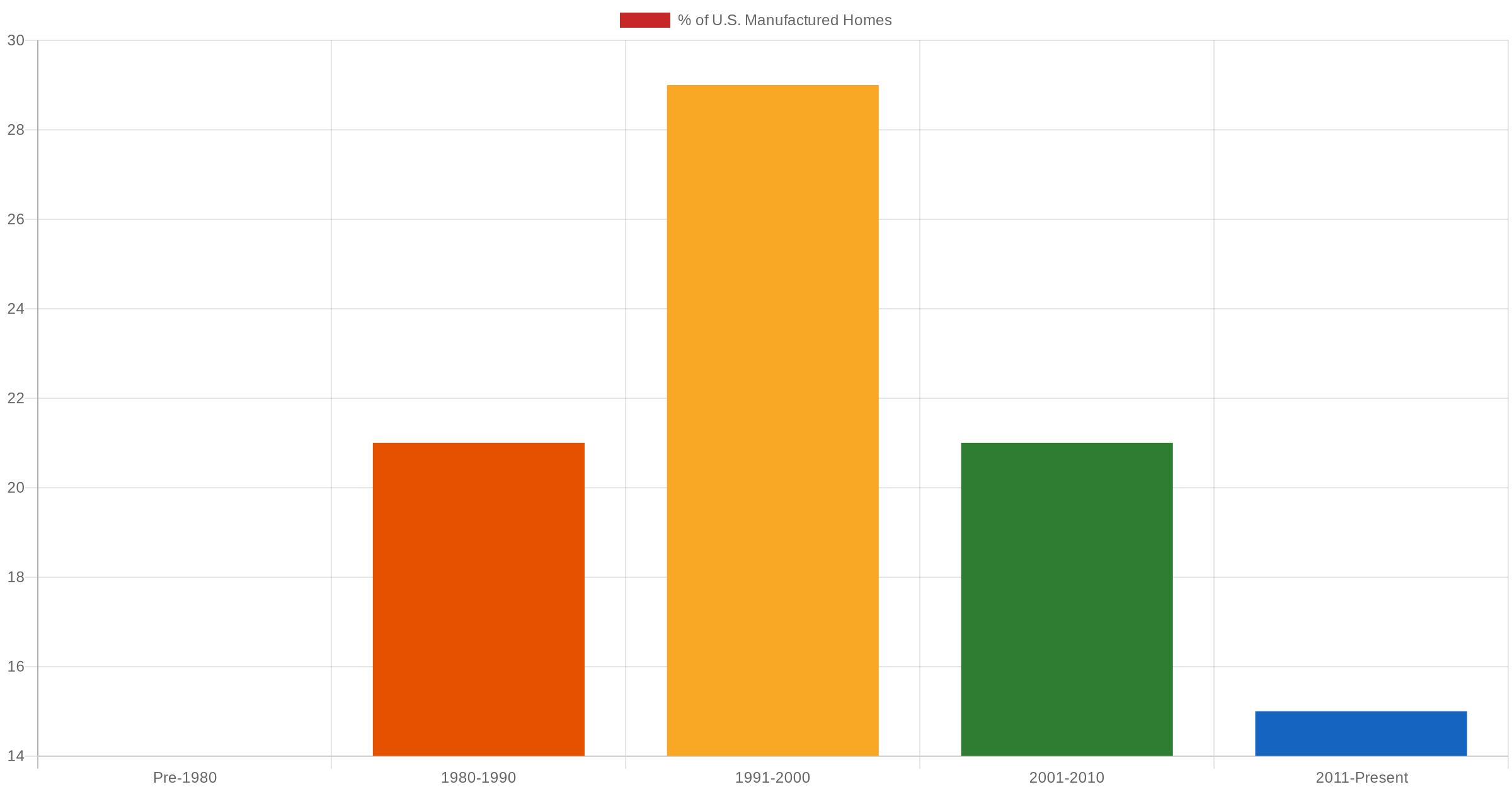

Industry data tells a sobering story:

- Approximately 35% of manufactured homes currently occupied in U.S. communities were placed before 1990

- The average age of a manufactured home in a land-lease community is over 25 years

- In the Southeast — North Carolina, Tennessee, Georgia, and South Carolina — the concentration of pre-1990 home stock is even higher due to the historically slower pace of infill with new homes

This aging inventory creates a cascade of operational headaches that compound over time:

1. Suppressed Lot Rents

You cannot charge $500/month lot rent when the home sitting on that lot is a 1982 single-wide with a leaking roof. The market won’t support it. Residents in aging homes are effectively capping your rental income growth, even in strong markets where lot rents are rising everywhere else.

2. Endless Maintenance Drag

Older homes — especially park-owned homes — are maintenance sponges. Plumbing, electrical, HVAC, roofing, flooring: the repair calls never stop. On properties with significant aging home stock, maintenance can consume 20-30% of gross revenue on park-owned homes, compared to 4-8% on lots with resident-owned newer homes.

3. Community Appearance and New Resident Recruitment

A mobile home park full of deteriorating 40-year-old homes is harder to market. It affects your ability to attract new residents, which directly affects vacancy rates. And vacancy in a land-lease community is pure income destruction — the infrastructure is still there, you’re still paying utilities and taxes, but the lot is producing zero revenue.

4. Habitability Risk

At a certain point, aging homes become a liability. Structural failures, code violations, and habitability issues expose operators to regulatory action and, in the worst cases, mass vacancy events when residents have to be displaced. This is an increasingly common story in communities with very old home stock and operators who deferred investment for too long.

Evaluating a mobile home park deal means understanding far more than the rent roll. The MHP Due Diligence Playbook walks you through every critical step — 10 video modules, a 55-page master checklist, and 9 ready-to-use templates covering infrastructure, home stock assessment, utility systems, and more. It’s the complete system for analyzing mobile home park acquisitions with confidence.

The Financing Problem That Trapped Operators (Until Now)

Here’s the thing: operators have known about the aging home stock problem for years. The solution is obvious — get newer homes into the community. But the implementation has been brutally difficult because of one word: financing.

Unlike a single-family home on owned land, a manufactured home sitting on a leased lot cannot be financed with a conventional 30-year mortgage. The product used to finance manufactured homes on leased land is called chattel lending — a personal property loan that functions more like an auto loan than a real estate loan. Interest rates are higher (typically 7-10%), terms are shorter (15-20 years), and qualification standards have historically been tight.

The practical result: many of your long-term residents who’ve been faithfully paying their lot rent for 8, 10, 15 years have been unable to qualify for financing to upgrade their home. Their traditional credit score didn’t reflect their actual payment behavior. Rent payments were invisible to the credit bureaus.

The FHFA’s new credit scoring models change that equation. VantageScore and FICO 10T incorporate consistent on-time rent and utility payments into credit scores. The resident who’s paid your lot rent without a single late payment for a decade may now have a meaningfully higher credit score than the old models showed.

As Cody Pearce, co-CEO of Triad Financial Services — one of the nation’s largest manufactured home lenders — put it: “For too long, responsible consumers who consistently pay their rent and utilities on time have been overlooked by traditional scoring systems. This change is a meaningful step toward expanding access to homeownership.”

Why This Matters for Mobile Home Park Operators Right Now

The immediate implication: a portion of your residents who were previously unfinanceable may now qualify for chattel loans to upgrade their aging homes. That’s a meaningful operational opportunity.

Think through the math. If you operate a 75-lot mobile home park in North Carolina and 30 of those lots have homes placed before 1990, and even 20% of those residents can now qualify for financing they previously couldn’t access — that’s potentially 6 home upgrades. New homes on those lots could support $75-100/month more in lot rent per site. Over time, that’s $5,400-$7,200 in annual incremental NOI from a community-driven upgrade program — without you fronting the capital.

The chattel lending market is served primarily by three major players in the Southeast:

- 21st Mortgage (Knoxville, TN — Berkshire Hathaway subsidiary)

- Triad Financial Services (Jacksonville, FL)

- Vanderbilt Mortgage (Maryville, TN — Clayton Homes subsidiary)

Each has programs for residents financing new homes on existing lots in land-lease communities. If you don’t have established relationships with these lenders, now is the time to build them.

A Practical Playbook for Operators

You don’t need to overhaul your entire operation to start taking advantage of this shift. Here’s a methodical approach:

Step 1: Audit Your Home Stock

Build a simple spreadsheet: lot number, year of home placement, home condition (1-5 scale), estimated remaining useful life. A park manager who knows the community can knock this out in a few hours. Focus on lots where the home is 20+ years old and condition is a 2 or below.

Step 2: Cross-Reference With Payment History

Your highest-value upgrade candidates are long-term residents with consistent on-time payment records who are living in deteriorating homes. These are people who’ve been building credit history through their lot rent payments — and whose credit profiles may have just improved under the new scoring models.

Step 3: Have Honest Conversations

A simple, respectful outreach: “There have been some recent changes to credit scoring that may allow residents who’ve consistently paid their rent to qualify for financing on a new home. If you’ve ever thought about upgrading, now might be a good time to explore it. We’re happy to connect you with a lender who works with our community.”

This is genuinely helpful. Most residents in aging homes want a new home — they just didn’t think they could afford one.

Step 4: Connect With Chattel Lenders Now

Call 21st Mortgage, Triad, and Vanderbilt before you have a specific resident to refer. Introduce yourself as a mobile home park operator in NC/TN/SC/GA. Ask about their current programs. Ask specifically how they’re incorporating the new credit scoring models. Build the relationship so when a resident is ready, you have a warm handoff ready to go.

Step 5: Explore the Home Retailer Model (For Larger Operators)

The most sophisticated play is partnering with a manufactured home retailer — or becoming an authorized dealer yourself — to have a pipeline of new homes available when residents are ready to upgrade. Operators doing this capture $10,000–$30,000 in home margin per transaction, while simultaneously improving their community and increasing lot rent capacity. It’s not a small undertaking, but the economics at scale are compelling.

For more on evaluating mobile home park investments and the operational factors that drive long-term value, read our guide on how to invest in mobile home parks and explore our breakdown of passive investing options for those who want exposure without direct operations.

What to Watch For Over the Next 12 Months

Important caveats: The FHFA announcement applies to federally-backed mortgages. Chattel lending for manufactured homes on leased land is a separate product category, and not all chattel lenders have fully integrated VantageScore and FICO 10T into their underwriting yet. The practical timeline for this to materially affect chattel loan approval rates will likely play out over the next 12-24 months.

But the direction of travel is clear. Credit access for manufactured housing residents is expanding. The operators who start building the systems, relationships, and home replacement pipelines now will be significantly better positioned when the wave arrives.

The aging home stock problem isn’t going away on its own. But for the first time in years, there’s a credible path to solving it that doesn’t require operators to front all the capital themselves.

Conclusion: The Problem and the Opportunity Are the Same Thing

Mobile home parks with aging, deteriorating home stock are underperforming on lot rents, bleeding maintenance dollars, and sitting on a long-term habitability risk they’ll have to deal with eventually. That’s the problem.

The opportunity is that your residents — many of whom have been quietly building payment history that the old credit system ignored — may now have a path to financing that could solve the problem without you writing the check. The FHFA’s credit expansion doesn’t eliminate the chattel lending challenges, but it meaningfully expands the pool of your residents who can qualify.

The work is: audit your stock, identify your candidates, build your lender relationships, and start the conversations. It’s not a quick fix. But it’s a real one.

The MHP Due Diligence Playbook is the complete system for analyzing mobile home park acquisitions — including home stock assessment, infrastructure evaluation, utility due diligence, and financial underwriting. 10 video modules, a 55-page checklist, and 9 plug-and-play templates. Don’t evaluate another deal without it.

Frequently Asked Questions

What is chattel lending for manufactured homes?

Chattel lending is a personal property loan used to finance manufactured homes that sit on leased land (like a lot inside a mobile home park). Because the home isn’t permanently attached to owned land, it can’t be financed with a conventional real estate mortgage. Chattel loans typically have higher interest rates (7-10%) and shorter terms (15-20 years) than conventional mortgages. The three major chattel lenders for manufactured homes are 21st Mortgage, Triad Financial Services, and Vanderbilt Mortgage.

How does the new FHFA credit scoring change affect mobile home park residents?

FHFA’s April 22, 2026 announcement requires Fannie Mae and Freddie Mac to accept VantageScore and FICO 10T credit scoring models, which incorporate rental payment history and utility payments. For mobile home park residents who’ve been consistently paying lot rent but had thin traditional credit files, this may meaningfully increase their credit scores — potentially qualifying them for manufactured home financing they couldn’t previously access.

What is the typical cost to replace an aging manufactured home in a land-lease community?

A new HUD-code manufactured home ranges from $60,000–$130,000+ depending on size (single-wide vs. double-wide), manufacturer, and features. Set-up and installation costs typically add $5,000–$15,000. When residents finance through chattel lenders, the operator doesn’t front this cost — the resident carries the loan. The operator’s benefit is an upgraded home on the lot, which supports higher lot rents over time.

Which states have the highest concentration of aging manufactured home stock?

The Southeast has particularly high concentrations of older manufactured homes, including North Carolina, South Carolina, Georgia, Tennessee, Alabama, and Mississippi. Many mobile home parks in these states were built in the 1960s-1980s and still have significant pre-1990 home stock on occupied lots. This is a key due diligence item for any operator or investor evaluating communities in these markets.

How should mobile home park operators approach residents about home upgrades?

The most effective approach is transparent and genuinely helpful — not sales-y. Informing residents about financing programs, connecting them with lenders, and explaining what’s available respects their autonomy while opening a door they may not have known existed. High-pressure tactics backfire in close-knit mobile home park communities. Build trust first. The residents who want new homes will find their way to the conversation.