In 2026, building passive income has never been more discussed — or more misunderstood. Scroll through any finance forum and you will find everyone from dividend stock enthusiasts to real estate syndicators claiming their approach is the best.

The truth? There is no single best passive income strategy. The right one depends on how much capital you are starting with, your tax bracket, and how hands-off you actually want to be.

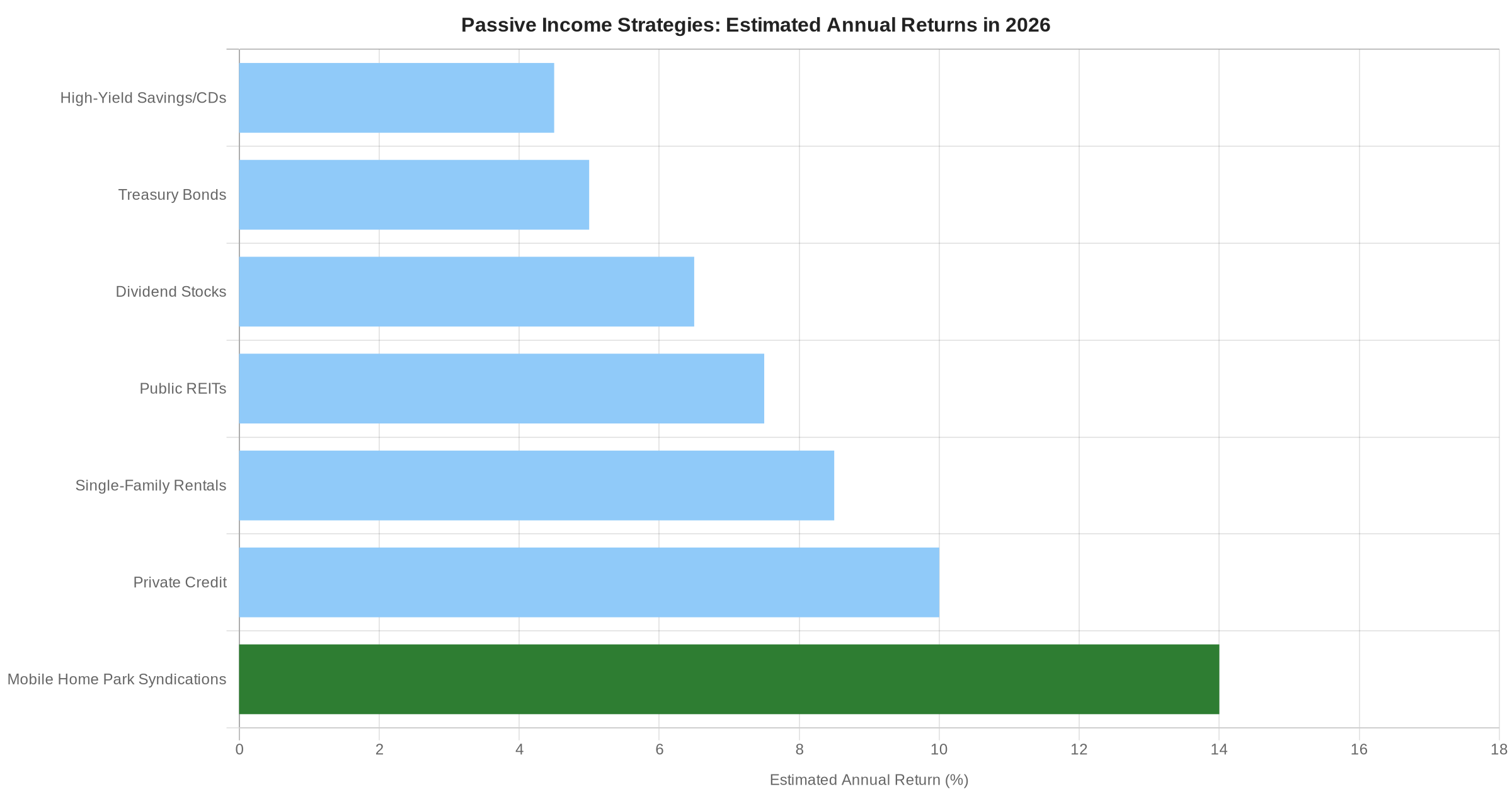

This breakdown ranks seven of the most popular passive income ideas across three key dimensions: minimum capital required, estimated annual return, and tax efficiency. We will give you an honest look at each — starting with the lowest barrier and working up to the strategies that generate the most after-tax income for serious investors.

How We Ranked These Passive Income Ideas

Each strategy was evaluated on three factors:

- Capital required: What is the realistic minimum to participate?

- Annual return potential: What can you reasonably expect per year?

- Tax efficiency: How much of that return do you actually keep after taxes?

Returns are estimates based on 2025–2026 market conditions. Actual results vary based on deal quality, market timing, and individual tax situations.

1. High-Yield Savings Accounts and CDs

Capital Required: Any amount | Est. Annual Return: 4–5% | Tax Efficiency: Low

High-yield savings accounts and certificates of deposit are the simplest entry point for passive income. In 2026, top-tier online banks are still offering 4–5% APY — a significant improvement from the near-zero rates of a few years ago.

The catch: all interest income is taxed as ordinary income, meaning investors in higher brackets keep only 60–70 cents of every dollar earned. CDs also lock up capital for a fixed term, limiting flexibility when better opportunities arise.

Best for: Emergency funds and short-term capital you cannot afford to put at risk.

2. Treasury Bonds and I-Bonds

Capital Required: $100+ | Est. Annual Return: 4.5–5.2% | Tax Efficiency: Moderate

U.S. Treasury securities — bills, notes, bonds, and I-Bonds — are among the safest passive income vehicles available. They are backed by the federal government and largely exempt from state and local income taxes, providing modest tax relief compared to savings accounts.

However, nominal returns remain modest by real estate standards, and during periods of elevated inflation, real returns can turn negative. I-Bonds are capped at $10,000 per year per person, limiting scalability for larger capital deployments.

Best for: Conservative investors or capital preservation within a larger portfolio.

3. Dividend Stocks

Capital Required: $500–$5,000+ to build meaningful income | Est. Annual Return: 5–7% | Tax Efficiency: Moderate

Dividend-paying stocks — especially Dividend Aristocrats with 25+ consecutive years of increases — are a classic passive income approach. Qualified dividends are taxed at the lower long-term capital gains rate (0–20%), which is more favorable than ordinary income treatment.

The downside: stock market volatility affects both yield and principal. A 5% dividend does not feel great when the underlying stock drops 20%. Meaningful monthly cash flow also requires substantial capital — a 5% yield on $50,000 is only $208 per month before taxes.

Best for: Long-term wealth builders comfortable with market volatility.

4. Public REITs (Real Estate Investment Trusts)

Capital Required: Any amount (publicly traded) | Est. Annual Return: 6–9% | Tax Efficiency: Moderate

REITs offer real estate exposure with stock-market liquidity. They are required to distribute at least 90% of taxable income as dividends, which creates reliable payouts. The 20% pass-through deduction under Section 199A can reduce the effective tax rate on REIT dividends for qualifying investors.

The tradeoff: public REITs move with equity markets, not just real estate fundamentals. During the 2022 rate-hike cycle, many REITs dropped 30–40% even while underlying properties held value. You also have no control over the assets you own — you are entirely dependent on management decisions.

Best for: Investors who want real estate exposure with full liquidity and no minimum hold period.

5. Single-Family Rental Properties

Capital Required: $50,000–$150,000+ (down payment + reserves) | Est. Annual Return: 6–10% cash-on-cash | Tax Efficiency: High (depreciation)

Rental properties are the classic passive income play for American investors — buy a house, rent it out, collect monthly cash flow. The real advantage is depreciation: the IRS allows you to deduct the cost of the building over 27.5 years, often creating paper losses that offset other income for qualifying real estate professionals.

But passive is a stretch for most landlords. Tenant calls, maintenance emergencies, vacancies, and turnover between tenants are real management burdens. Professional property management helps, but typically costs 8–12% of gross rent, compressing margins significantly on lower-rent properties.

Best for: Hands-on investors willing to manage assets directly and build equity over time.

📋 The MHP Due Diligence Playbook — 10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal. Get the Playbook →

6. Private Credit and Hard Money Lending

Capital Required: $25,000–$100,000+ | Est. Annual Return: 9–12% | Tax Efficiency: Low to Moderate

Private credit — lending capital directly to real estate investors or businesses at above-market rates — has grown significantly as institutional investors chased yield in a higher-rate environment. Hard money loans typically earn 10–12% annualized, paid as ordinary interest income.

The risks are real: defaults, slow repayment, and illiquidity. Unless you are lending through a well-managed fund diversified across dozens of loans, a single default can wipe out a full year of returns. Tax treatment is similar to savings account interest — fully taxable as ordinary income.

Best for: Sophisticated investors comfortable with underwriting credit risk and tolerating illiquidity.

7. Mobile Home Park Syndications

Capital Required: $50,000–$100,000 (typical minimum) | Est. Annual Return: 12–16% total return | Tax Efficiency: Very High

Mobile home park syndications — where a professional operator raises capital from passive investors to acquire and operate a community — consistently rank among the highest total-return, tax-advantaged passive income vehicles available to accredited investors.

Here is why mobile home park investing stands out from every other option on this list:

- Depreciation and cost segregation: Investors typically receive K-1s with significant paper losses from cost segregation studies, which can offset passive income or even earned income for qualifying real estate professionals. This often results in paying taxes on only a fraction of the cash distributions received.

- Structural rent growth: Mobile home park lot rents remain significantly below market in most regions. Operators can often raise rents 5–10% annually while still offering the most affordable housing option in their local market — demand does not compress when you raise rent from $400 to $440 per month.

- Extremely low tenant turnover: Unlike apartments — which see roughly 47% annual turnover — mobile home park communities average around 2% annual home turnover. Moving a manufactured home costs $3,000–$10,000, which makes residents extraordinarily sticky.

- Supply constraints that protect your investment: New mobile home parks are effectively impossible to build in most jurisdictions due to zoning restrictions. Fewer than 20 new communities are permitted nationally in a typical year, out of roughly 45,000 existing parks — a permanent structural moat that protects existing asset values.

For passive investors seeking after-tax income with inflation protection, this combination is difficult to replicate elsewhere. Learn more about what returns look like in a mobile home park syndication, and see how mobile home park tax benefits work for limited partners.

Best for: Accredited investors with a 5–7 year time horizon seeking high after-tax returns with a professionally managed, inflation-resistant real estate asset.

Passive Income Strategies Compared: The Full Picture

| Strategy | Min. Capital | Est. Annual Return | Tax Efficiency |

|---|---|---|---|

| High-Yield Savings/CDs | Any | 4–5% | ★ |

| Treasury Bonds | $100 | 4.5–5.2% | ★★ |

| Dividend Stocks | $500+ | 5–7% | ★★ |

| Public REITs | Any | 6–9% | ★★ |

| Single-Family Rentals | $50,000+ | 6–10% | ★★★ |

| Private Credit | $25,000+ | 9–12% | ★★ |

| Mobile Home Park Syndications | $50,000+ | 12–16% | ★★★★★ |

The Bottom Line: Which Passive Income Strategy Is Best in 2026?

There is no universal answer — but there is a logic to follow. If you need liquidity and cannot tolerate principal risk, high-yield savings and Treasury bonds belong at the foundation of your plan. If you are comfortable with market volatility and want real estate exposure without a lockup period, dividend stocks and public REITs round out a solid base.

If you are an accredited investor with capital to deploy for 5+ years and you are serious about maximizing after-tax returns, mobile home park syndications deserve a close look. The combination of structural rent growth, minimal new supply, sticky residents, and depreciation-driven tax advantages is genuinely hard to replicate in other asset classes.

The key is to match the strategy to your actual situation — not to chase the highest headline return without understanding the risk and liquidity profile that comes with it.

For a deeper dive into how passive investors participate in mobile home park deals, explore our complete guide to passive investing in mobile home parks.

Frequently Asked Questions

What is the best passive income investment in 2026?

For accredited investors prioritizing after-tax returns, mobile home park syndications consistently rank among the highest-performing passive income options — combining 12–16% estimated total annual returns with significant depreciation benefits that reduce taxable income. For investors who need liquidity or lower minimum commitments, public REITs or dividend stocks are strong alternatives.

How much money do you need to start earning passive income?

You can begin earning passive income with as little as a few hundred dollars through high-yield savings accounts or dividend ETFs. To generate meaningful monthly cash flow — say $2,000–$5,000 per month — you typically need $300,000–$600,000 deployed across higher-yielding strategies. The math is straightforward: a 12% annual return on $300,000 produces $36,000 per year ($3,000 per month) before taxes.

Is mobile home park investing really passive?

As a limited partner in a syndication, yes — it is genuinely passive. You provide capital, sign the operating agreement, and receive quarterly distributions and an annual K-1. The general partner handles everything from acquisition through day-to-day management to eventual sale. There are no tenant calls, maintenance requests, or leasing headaches on your end. See our post on active vs. passive mobile home park investing for a full breakdown.

Are passive income investments taxed?

Yes, but the tax treatment varies significantly by vehicle. Interest income from savings accounts, CDs, and bonds is taxed as ordinary income. Qualified dividends and long-term capital gains receive preferential rates. Real estate syndication income benefits from depreciation and cost segregation, often generating paper losses that offset cash distributions — making the after-tax return substantially higher than the pre-tax headline number. Always consult a CPA for your specific situation.

What is the difference between passive income and portfolio income for tax purposes?

The IRS distinguishes between passive income (from rental activities or businesses you do not materially participate in), portfolio income (dividends, interest, capital gains), and earned income (wages). Passive losses from real estate generally only offset passive income — though qualifying real estate professionals and some high-income earners have additional options. A tax advisor familiar with real estate syndication K-1s can help you navigate this effectively.

📋 Ready to Evaluate Your Next Mobile Home Park Deal? Get the MHP Due Diligence Playbook — the complete system for analyzing mobile home park acquisitions with confidence. 10 video modules, a 55-page master checklist, and 9 ready-to-use templates. Get the Playbook →