If you’re a mobile home park investor who bought a value-add property with significant vacancy, you’ve probably already discovered something the underwriting spreadsheets don’t warn you about: filling lots is much harder than it looks.

It’s not because residents don’t want to live there. Demand for affordable housing is at an all-time high. The issue isn’t demand. The issue is financing — and in 2026, the manufactured housing financing system is broken in ways that directly impact your ability to execute an infill strategy.

Here’s what’s actually happening, and what experienced operators are doing about it.

The Chattel Loan Problem

When a prospective resident wants to buy a manufactured home in a land-lease community — your park — they can’t use a conventional mortgage. The home sits on land they don’t own. That disqualifies it from standard Fannie Mae or Freddie Mac financing in most configurations.

Instead, they need a chattel loan — a personal property loan secured by the home itself, not real estate. Roughly 76% of manufactured homes are financed this way. And the terms are punishing:

- Interest rates: 7.5%–11% as of mid-2026

- Down payment: 10%–20% required

- Loan term: 15–20 years (shorter than a 30-year mortgage, meaning higher monthly payments)

- Minimum credit score: typically 600–650

Run the math on a $90,000 home at 9.5% for 20 years with 10% down: you’re looking at roughly $750–$850/month in loan payment. Add lot rent of $500/month and your resident’s total housing cost is $1,250–$1,350/month. That’s not outrageous — but for the residents most likely looking at your park (credit scores in the 580–620 range, limited savings, or inconsistent income history) qualifying at all is a significant hurdle.

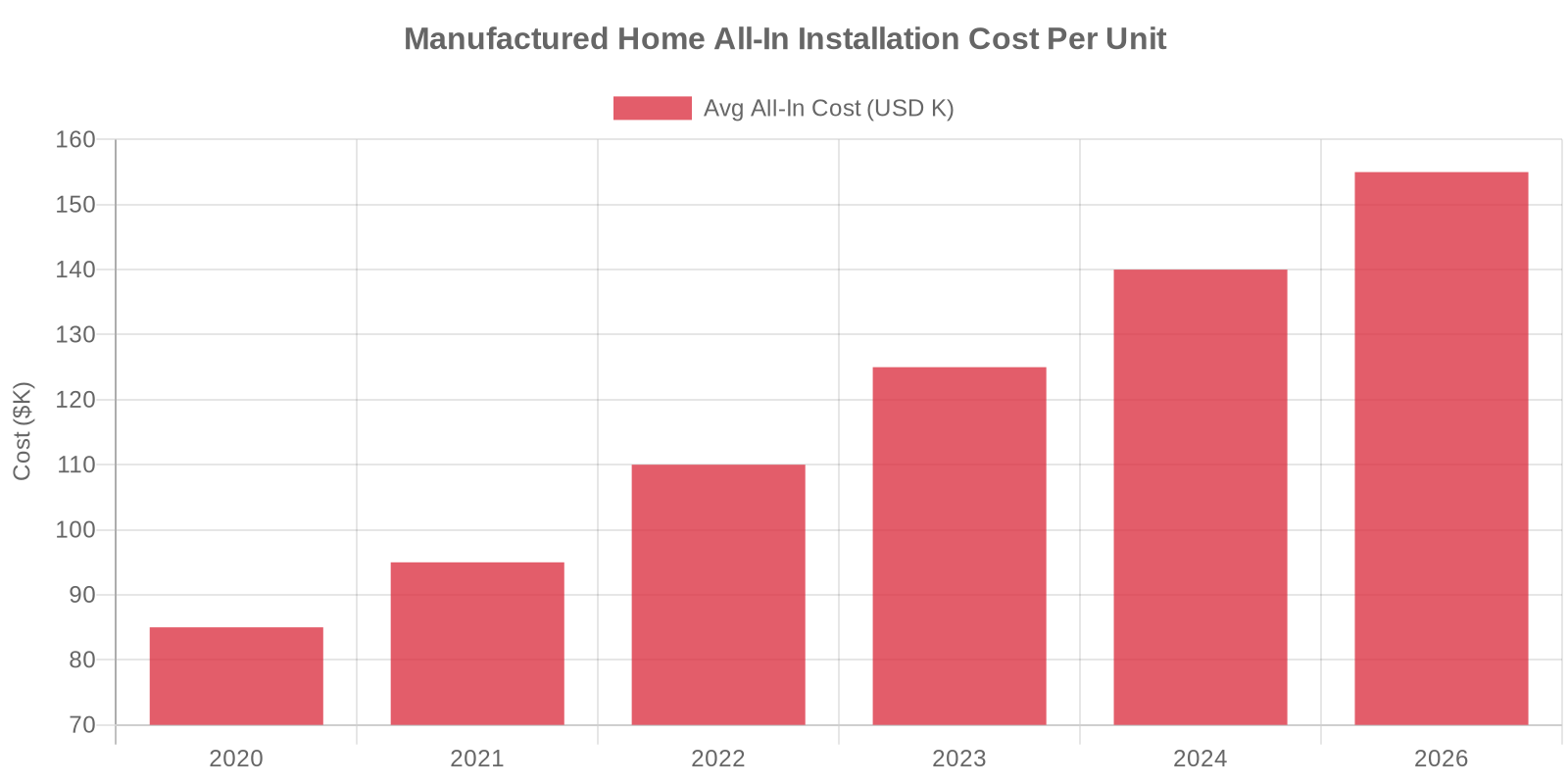

The Cost of Entry Has Exploded

The financing challenge is compounded by the dramatic increase in all-in home costs since 2021. Installation costs for new manufactured homes — including the home itself, transport, site preparation, utility hookups, and permits — have risen 35–60% in four years. What cost $85,000 all-in in 2020 now costs $130,000–$160,000.

This creates a compound problem for operators: the home costs more, the loan is more expensive, and the resident pool has the same (or worse) financial profile as before. The math that worked in 2020 is harder to make work in 2026.

Why Operators Get Stuck

Here’s the trap many operators fall into: they have vacant lots, they have prospective residents, but they can’t get those residents to the closing table. So they end up doing one of three things — none of them great:

- Buy homes themselves and rent them as park-owned homes. This works, but it converts an asset-light lot-rent business into a capital-intensive rental business with all the headaches of home maintenance.

- Wait for better-qualified applicants. Leads pile up, no one qualifies, months pass, lots stay empty. Every empty lot is $500–$700/month in lost revenue.

- Drop lot rent to make the economics work. This solves the immediate vacancy problem but undercuts the long-term value of the asset.

None of these is the right answer. The right answer is to systematically move prospective residents through the financing process more effectively.

What the Best Operators Are Doing

Build a lender network before you need it

Don’t wait until you have a qualified applicant to figure out your lending relationships. Call 21st Mortgage, Triad Financial Services, and Cascade Loans today. Understand their actual qualification criteria — credit score minimums, debt-to-income requirements, income documentation. Know which lender is best for which resident profile. This knowledge alone will save you enormous time and let you pre-screen applicants intelligently.

Create a “Resident Readiness” onboarding process

When a prospective resident inquires about moving in, don’t just show them homes and hope they can get financed. Give them a packet that explains exactly what they’ll need to qualify for financing: credit score, down payment, income verification. Help them understand where they are versus where they need to be. Residents who are 90 days from qualifying are worth nurturing — don’t let them disappear.

Implement a structured rent-to-own program

For residents who want to be there but can’t qualify for chattel financing today, consider a lease-to-own structure on park-owned homes. Set the purchase price upfront. A portion of each monthly payment credits toward the down payment. Eighteen to twenty-four months of on-time payments builds their credit while building their equity. Done correctly, this creates some of the most loyal, invested residents in your portfolio — and converts them to homeowners without the capital burden of carrying park-owned homes long-term.

Tap into state housing programs

This is the most underutilized tool in the mobile home park operator playbook. States like North Carolina (NC Housing Finance Agency) and Tennessee (THDA) have manufactured housing programs that include subsidized loans, down payment assistance, and community partnership programs. Getting listed as an approved community in these programs can unlock a pipeline of pre-approved residents who are ready to move. The application process takes time, but the payoff is significant.

Partner with local housing nonprofits

Many communities have housing assistance organizations specifically working to place qualified residents in affordable homeownership. A park that positions itself as a legitimate, well-managed affordable housing option can become a referral destination for these organizations — providing a steady stream of pre-screened applicants at no marketing cost.

The Bigger Picture

The financing gap in manufactured housing is a systemic problem that won’t be fixed quickly at the policy level, despite years of advocacy. Fannie Mae’s MH Advantage program and Freddie Mac’s CHOICEHome program have made modest progress, but they apply to a narrow slice of the market — higher-spec homes that look more like site-built housing.

For the typical mobile home park operator running value-add communities, the answer isn’t waiting for policy reform. It’s building systems to work more effectively within the current environment. The operators who are successfully executing infill strategies in 2026 approach resident financing with the same rigor they bring to acquisition due diligence — knowing their numbers cold before they go under contract. (If you’re evaluating a park with vacancy, the Keel Team Due Diligence Playbook walks through infill underwriting assumptions worth stress-testing.)

The vacant lots aren’t going to fill themselves. But with the right systems in place, they don’t have to stay empty either.

Keel Team specializes in acquiring and operating mobile home parks in the Southeast and Midwest. We focus on communities with city water, city sewer, and strong occupancy fundamentals. For more educational content on mobile home park investing, visit keelteam.com.