In real estate, the best moats are invisible until you go looking for them. With mobile home parks, one of the most powerful structural advantages isn’t a technology, a brand, or even operational expertise — it’s simply the fact that almost no one is building new ones.

While apartments, office buildings, warehouses, and single-family homes are added to the market each year by the hundreds of thousands, the number of new mobile home park communities being developed annually is nearly zero. That supply constraint — baked into zoning law, community politics, and development economics — creates a durable advantage for investors who own existing communities. And in 2026, that moat is wider than ever.

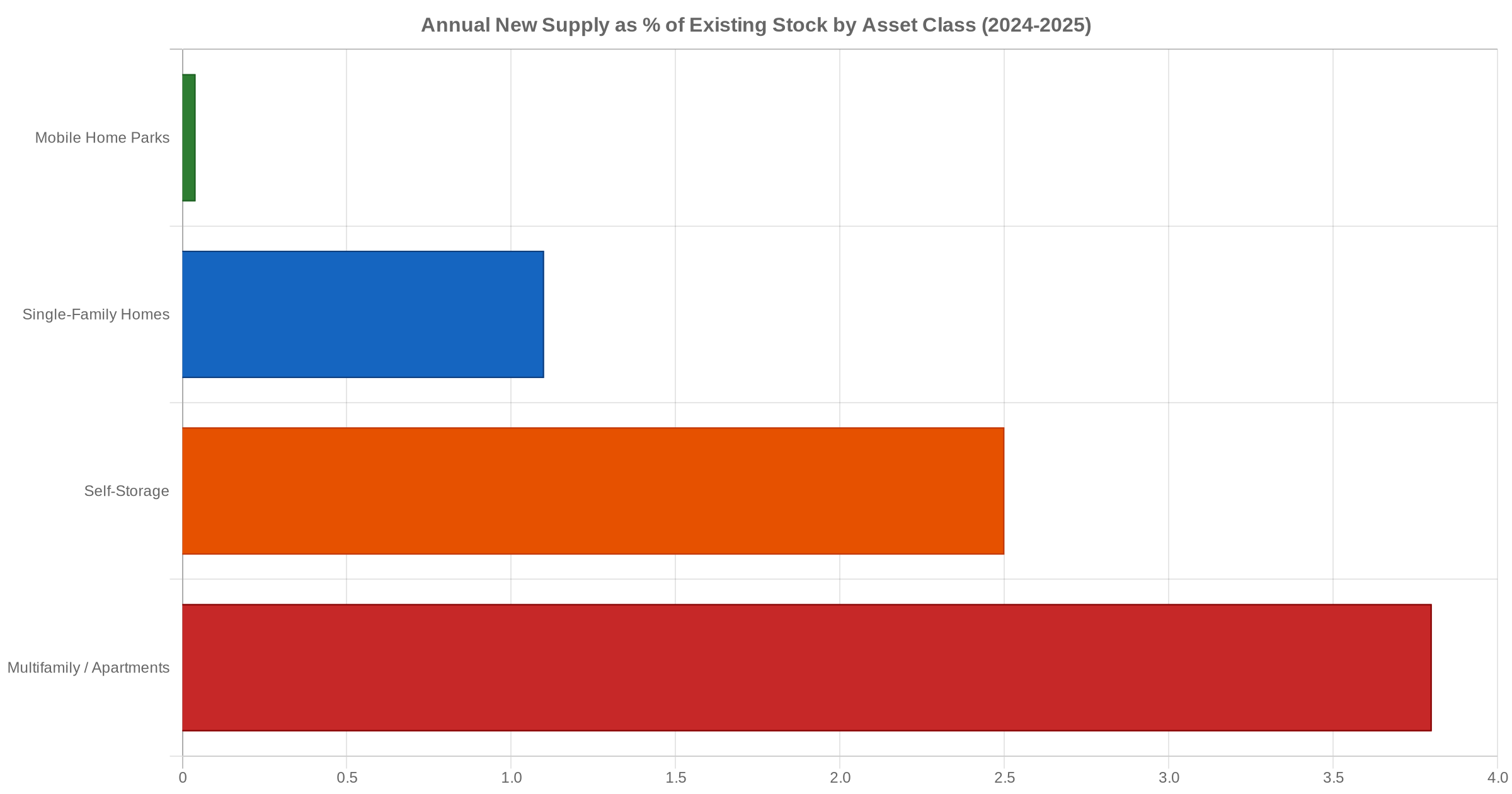

The Numbers Don’t Lie: Almost Zero New Mobile Home Parks Being Built

The United States has approximately 43,000 to 45,000 manufactured housing communities. Across all of those communities, roughly 20 new ones are developed each year. That’s a net new supply rate of approximately 0.04% per year.

By comparison:

- Multifamily / Apartments: ~3.8% new supply annually (588,000+ units delivered in 2024 alone)

- Self-Storage: ~2.5% new supply annually

- Single-Family Homes: ~1.1% new supply annually

- Mobile Home Parks: ~0.04% new supply annually

No other major real estate asset class even comes close to this level of supply scarcity. When demand rises, property owners can raise lot rents. When the economy softens, residents can’t easily move to a cheaper alternative that doesn’t exist. The supply side of the equation is essentially frozen.

Why Zoning Laws Make New Mobile Home Park Development Nearly Impossible

The single biggest barrier to new mobile home park development isn’t capital — it’s zoning. In most U.S. municipalities, manufactured housing communities require a special use permit or are outright prohibited in residential zones. The land that would support a mobile home park is typically zoned for something more politically palatable: single-family subdivisions, retail, or light industrial use.

Even where manufactured housing communities are theoretically permitted, developers face:

- Minimum lot size requirements that make smaller communities economically unviable

- Infrastructure mandates requiring the developer to fund roads, utilities, and stormwater systems upfront

- Design standards that increase per-lot development costs significantly

- Discretionary approval processes that give neighbors and elected officials veto power

Many states have preemption laws that theoretically prevent municipalities from banning manufactured housing outright. But local governments have found workarounds — setback requirements, density limits, and architectural standards — that achieve the same practical effect without triggering legal challenges. For a developer looking at a 3-5 year entitlement timeline before a single lot can be rented, the math rarely works.

You can read more about the development economics in our detailed breakdown: How to Develop a Mobile Home Park from Scratch: Costs, Timelines, and Why Most Investors Focus on Existing Communities.

The NIMBY Effect: Political Opposition to New Communities

Beyond zoning codes, mobile home park development faces something harder to quantify: organized community opposition. Despite the reality that manufactured housing communities provide stable, owner-occupied affordable housing, they carry a stigma that makes them politically toxic in many markets.

When a developer proposes a new mobile home park in a suburban municipality, the public hearing process almost inevitably surfaces concerns about property values, traffic, and community character. Elected officials — regardless of their stated positions on affordable housing — rarely want to be the vote that approved a mobile home park over neighborhood objections.

This dynamic is especially pronounced in the Sun Belt markets where population growth is driving the most demand for affordable housing. The places that need more manufactured housing the most are often the same places where local politics make it hardest to build.

The Economics of Building from Scratch vs. Buying Existing

Even when the zoning and political barriers can be cleared, the economics of ground-up mobile home park development are challenging. All-in development costs for a new community — including land, infrastructure, permitting, and initial home placement — typically run $40,000 to $75,000 per lot in markets where development is feasible. In high-cost coastal markets, that number can exceed $100,000 per lot.

Meanwhile, existing stabilized communities frequently trade at per-lot values of $15,000 to $50,000 depending on market, occupancy, and utility infrastructure. Buying an existing community at a reasonable cap rate almost always pencils better than building new — and the operational risks of a lease-up are avoided entirely.

The result: rational developers with capital don’t build new mobile home parks. They buy existing ones. Which increases competition for a fixed asset pool. Which compresses cap rates and increases values for existing owners.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

What Supply Constraints Mean for Existing Mobile Home Park Values

The supply moat translates directly into pricing power and value protection for existing community owners. When a mobile home park in a growing market reaches high occupancy, the owner has significant leverage to raise lot rents over time. Residents cannot simply move to a new community that was built nearby — because that community doesn’t exist.

This is fundamentally different from apartment investing, where a new 300-unit complex opening across the street can force rent concessions on existing properties for years. Mobile home park operators don’t face that competitive pressure. The supply is fixed, and demand from the 20+ million Americans living in manufactured housing continues to grow.

The numbers bear this out. National manufactured housing community occupancy has climbed from approximately 86.5% a decade ago to roughly 94% nationally in 2025. In some high-demand coastal and Sun Belt markets, occupancy exceeds 99%. That’s what happens when demand grows and supply doesn’t.

How the Supply Moat Protects NOI Through Economic Cycles

The supply constraint advantage doesn’t just protect values in good times. It also creates resilience during economic downturns — and this is where mobile home parks have truly earned their reputation as a defensive asset class.

During the Global Financial Crisis (2008–2010), manufactured housing community net operating income grew approximately +1.5% annually on average. Apartment NOI declined by roughly -5.6% during the same period. During COVID-19 (2020), the gap was similar: manufactured housing communities saw NOI grow approximately +4.2% while apartments declined approximately -3.2%.

Why? Because when the economy contracts and households face financial pressure, affordable housing becomes more valuable, not less. People don’t move out of the cheapest housing option in a market when times get hard — they move in. And there is no new supply to absorb that demand surge.

Mobile home park NOI has been positive every single year since 2007. No other major real estate asset class can claim that consistency.

What This Means for Investors Buying Existing Parks in 2026

For investors evaluating the mobile home park investment thesis in 2026, the supply constraint story is simultaneously good news and a caution flag. The good news: the moat is real and durable. The caution: because it’s well understood, institutional capital has entered the space aggressively, compressing cap rates from what they were five to ten years ago.

Premium stabilized communities in high-demand markets now trade at 4.5–6% cap rates. Value-add opportunities with occupancy upside or rent-to-market potential typically trade at 6.5–8%. Tertiary-market or turnaround situations can still reach 8–12%. Understanding which tier you’re buying into matters significantly for return expectations. Our full breakdown: Mobile Home Park Cap Rates in 2026: What to Expect by Market Tier.

The supply constraint moat doesn’t guarantee returns regardless of price paid. But it does mean that a well-located, well-operated mobile home park has structural pricing power that very few other real estate assets can match — and that the competitive threat of new supply showing up to compete for your tenants is virtually nonexistent.

For operators focused on the Southeast — particularly North Carolina, Tennessee, Georgia, and South Carolina — the combination of population growth, affordable housing demand, and zero new supply is especially compelling. These are markets where lot rents remain well below comparable multifamily rents, leaving significant runway for responsible rent growth over time. You can explore financing options for acquiring existing parks here.

Conclusion

The supply constraint moat is one of the most underappreciated structural advantages in commercial real estate. While every other asset class wrestles with the competitive threat of new development, mobile home park investors operate in a market where the supply side is effectively frozen by zoning law, community politics, and unfavorable development economics.

The result is a fixed asset pool meeting growing demand — which translates to pricing power, occupancy stability, and NOI resilience through economic cycles that no amount of operational skill can replicate in higher-supply asset classes.

For investors serious about understanding why mobile home parks have attracted institutional capital and delivered consistent returns through multiple economic cycles, the supply story is the place to start.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Frequently Asked Questions

Why aren’t more mobile home parks being built in the United States?

The primary barriers are zoning restrictions (most municipalities don’t allow new manufactured housing communities in residential zones), strong NIMBY opposition at the local government level, and development economics that make buying existing communities more attractive than building new ones. The combined effect is that only roughly 20 new communities are developed annually out of a base of 43,000–45,000 — a new supply rate of about 0.04% per year.

How does the supply constraint affect mobile home park values?

Limited supply gives existing community owners significant pricing power over time. When demand grows and no new supply enters a market, occupancy rises and owners can raise lot rents without losing residents to new competing options. This dynamic supports both cash flow and asset appreciation, particularly in high-growth Sun Belt markets.

Does the mobile home park supply moat protect investors during recessions?

Yes, historically. During the Global Financial Crisis and COVID-19, manufactured housing community NOI remained positive while apartment NOI declined. The affordable housing segment tends to be counter-cyclical: when the economy weakens, demand for the most affordable housing option in a market increases rather than decreases. The supply constraint amplifies this dynamic by ensuring no new alternatives are built to absorb that demand.

Are there any markets where new mobile home parks are being developed?

Ground-up development does occur occasionally in rural markets with favorable land costs, lighter zoning requirements, and strong agricultural or workforce housing demand. Some developers are also exploring new “resort-style” manufactured housing communities targeting retirees. However, these remain rare exceptions. The overwhelming majority of mobile home park transactions involve acquiring and improving existing communities rather than developing new ones.

How do supply constraints affect my underwriting as a buyer?

When underwriting an acquisition, the supply constraint means you can reasonably model steady lot rent growth over your hold period without significant risk of a competing community opening nearby and forcing concessions. It also means occupancy improvements achieved through infill (filling vacant lots) are durable gains rather than temporary spikes. Both factors support more aggressive value-add underwriting relative to asset classes with higher new supply risk.

Get the top 20 lessons from two decades of mobile home park investing — free.