Wisconsin may not be the first state that comes to mind when investors scan for mobile home park acquisition targets. North Carolina, Tennessee, and Georgia tend to get the headlines. But that relative obscurity is part of the appeal: Wisconsin offers higher cap rates, significantly below-market lot rents with substantial upside, a landlord-friendly regulatory environment, and an aging owner-operator base that creates real off-market deal flow for buyers willing to do the work.

This guide covers everything you need to know about mobile home park investing in Wisconsin in 2026 — from market fundamentals and top MSAs to regulatory considerations, due diligence priorities, and financing options.

Why Investors Are Taking a Closer Look at Wisconsin

Wisconsin’s manufactured housing market has several structural advantages worth understanding:

- No statewide rent control: Wisconsin prohibits local rent control ordinances (Wis. Stat. § 66.1015), giving mobile home park operators the flexibility to bring lot rents to market rates through measured increases.

- Strong blue-collar employment base: Manufacturing, logistics, agriculture, and paper/packaging industries drive steady demand for affordable workforce housing across Wisconsin’s mid-sized cities.

- Underserved mid-sized markets: Cities like Green Bay, Appleton, and Eau Claire have growing populations but limited new housing supply — supporting strong occupancy in manufactured housing communities.

- Higher cap rates than coastal and Southeast markets: Midwest mobile home parks typically trade at 7–9% cap rates, well above the 5–6% range now common in premium Southeast assets.

- Aging owner-operator base: Thousands of Wisconsin mobile home parks are still owned by families who acquired them 20–40 years ago. Estate sales, retirements, and tired landlords create an ongoing pipeline of off-market acquisition opportunities for buyers who invest in direct owner relationships.

Wisconsin Mobile Home Park Market Overview (2026)

Wisconsin has approximately 1,200–1,400 manufactured housing communities statewide, concentrated across its major metro areas and mid-sized cities. The state’s population of approximately 5.9 million is spread across several distinct markets, each with its own demand dynamics and pricing environment.

Key market indicators for 2026:

- Average monthly lot rent: $365–$425 depending on MSA (the national average is ~$752/month — Wisconsin’s below-market position represents significant revenue upside)

- Typical occupancy rates: 85–93% across stabilized communities

- Cap rate range: 7.0–9.5% for stabilized assets; 9–12% for value-add or turnaround opportunities

- Deal flow: Primarily off-market, driven by estate sales, aging owner-operators, and Midwest-focused manufactured housing brokers

The gap between Wisconsin lot rents and the national average is one of the central investment theses for the market. Operators who acquire parks with rents 30–40% below market have a clear, measurable path to NOI growth through systematic rent normalization — typically 3–5% annual increases over a 3–5 year hold period.

Top Markets for Mobile Home Park Investing in Wisconsin

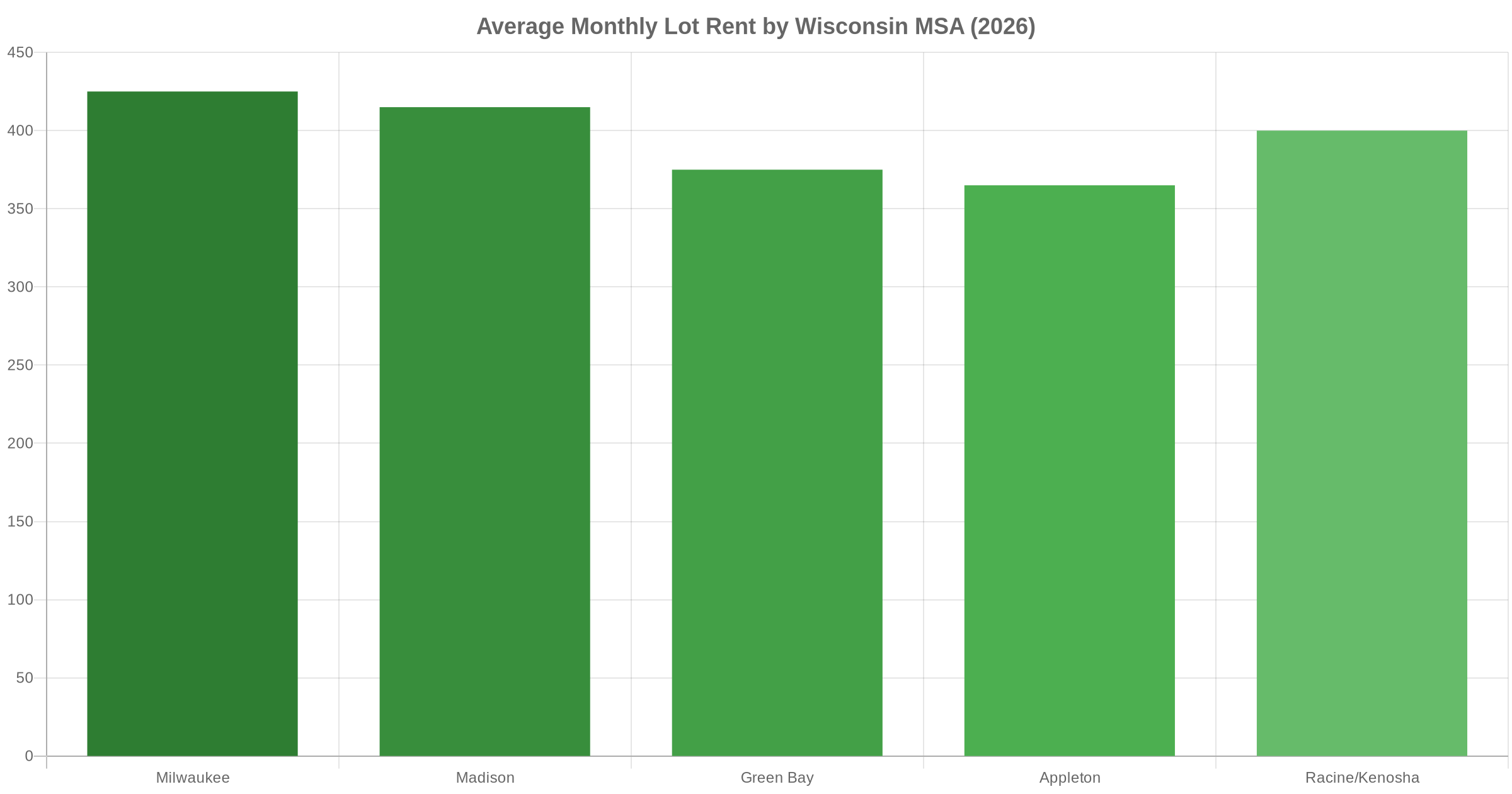

Milwaukee Metropolitan Area

The Milwaukee metro — including Waukesha, Ozaukee, and Washington counties — is Wisconsin’s largest market, with a combined population exceeding 1.6 million. Milwaukee has a deep manufacturing and logistics employment base, substantial affordable housing demand, and a growing professional population in its suburbs. Mobile home parks in the Milwaukee metro typically command lot rents of $400–$450/month. Cap rates on stabilized assets trend toward 7–7.5% due to greater institutional activity, but off-market opportunities in the 8–9% range still exist for operators with strong origination capabilities.

Madison (Dane County)

Madison is the fastest-growing major market in Wisconsin, driven by the University of Wisconsin flagship campus, state government employment, and a maturing tech sector. Population growth in Dane County has been consistent for two decades, creating persistent demand for affordable workforce housing. Lot rents average $400–$425/month in the Madison MSA. The tradeoff: fewer total mobile home park communities than Milwaukee, and properties trade more competitively due to land appreciation pressure near the city core.

Green Bay and the Fox Valley

Green Bay (population ~115,000) and the Fox Valley corridor — Appleton, Oshkosh, Fond du Lac — offer some of the most accessible entry points for mobile home park investors in Wisconsin. Lot rents in this region average $360–$390/month, with cap rates frequently landing in the 8–10% range for stabilized assets. These markets have strong manufacturing employment (particularly in the paper and packaging industry), lower competition from institutional capital, and a meaningful inventory of family-owned mobile home parks where direct-to-owner conversations can yield off-market acquisitions.

Racine and Kenosha

Located between Milwaukee and Chicago along Lake Michigan, Racine and Kenosha benefit from proximity to the Chicago metro while operating at Wisconsin pricing. Lot rents average $395–$420/month. The Illinois border creates both opportunity — workers priced out of northern Illinois seeking Wisconsin affordability — and concentration risk if Chicago employment patterns shift. Mobile home parks in this submarket consistently attract strong occupancy given the affordability premium relative to comparable communities in Illinois.

Secondary Markets: Eau Claire, La Crosse, Wausau

Smaller Wisconsin cities host modest manufactured housing inventories but often present the best pure value-add opportunities. Cap rates in these markets can reach 10–12% for operators willing to take on occupancy risk or near-term capital improvement projects. For investors with hands-on operational expertise, secondary Wisconsin markets offer high-return potential with minimal institutional competition.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Lot Rent Trends and Cap Rates in Wisconsin

Wisconsin lot rents have grown approximately 4–6% annually over the past three years — slightly below the national average of ~7% — but the trajectory is accelerating. The gap between Wisconsin lot rents and broader regional rental rates remains wide, supporting continued rent growth without pricing residents out of their communities.

Key data benchmarks:

- National average lot rent (2026): ~$752/month

- Wisconsin average lot rent (2026): ~$390/month (~48% below national average)

- Annual lot rent growth rate in Wisconsin: 4–6%

- Average cap rate for stabilized Wisconsin assets: 7.5–8.5%

- Value-add and turnaround cap rates: 9–12%

The below-market lot rent position is the most compelling feature of the Wisconsin opportunity. When operators acquire parks at rents 40–50% below the national average and implement disciplined annual increases, the compounding effect on property value is substantial. A 50-lot park at $380/month that moves to $450/month over five years adds roughly $350,000–$500,000 in asset value at an 8% cap rate, assuming expenses are well-controlled.

For a deeper look at how cap rates work in this asset class and what ranges to target by market type, see: Mobile Home Park Cap Rates Explained: What’s a Good Cap Rate in 2026?

Wisconsin Regulatory Environment for Mobile Home Park Owners

Understanding the regulatory landscape before acquiring any mobile home park is non-negotiable. Wisconsin is generally considered a favorable state for mobile home park operators — but there are specific rules to know.

No Statewide Rent Control

Wisconsin statute § 66.1015 prohibits municipalities from enacting rent control. This is a meaningful structural advantage compared to states like Oregon, California, and New Jersey, where local rent ordinances can severely constrain operational upside. Wisconsin operators can implement market-rate rent increases without local regulatory interference — though maintaining resident relationships and implementing changes thoughtfully is always sound practice.

Landlord-Tenant Law Under Chapter 710

Wisconsin’s manufactured housing landlord-tenant framework is governed by Chapter 710 of the Wisconsin Statutes. Key provisions for investors:

- Month-to-month tenancies require 28-day written notice to terminate

- Eviction for nonpayment of rent requires a 5-day cure notice before filing

- Park closure requires 180 days’ advance notice to residents

- Residents have the right to organize tenant associations

No Right of First Refusal (as of 2026)

As of this writing, Wisconsin has not enacted right-of-first-refusal (ROFR) legislation for manufactured housing community sales — meaning residents and tenant associations do not have a statutory right to purchase a park before it’s sold to a third party. This keeps Wisconsin transactions more straightforward than states that have passed ROFR laws. Investors should monitor legislative activity, however: ROFR proposals have been introduced in several Midwest state legislatures and the political climate is shifting. For context on how tenant protection legislation is affecting other markets, see our guide to mobile home park tenant protection laws in 2026.

Cold Climate Infrastructure Costs

Wisconsin winters introduce operational costs that simply don’t apply in warmer markets. Build these into your underwriting from day one:

- Winterized water and sewer systems (heat tape, insulation on exposed lines)

- Road and driveway maintenance under ice and snow conditions

- Higher utility costs for any park-owned homes (POH)

- Freeze-thaw cycle damage to older infrastructure (clay pipe, deteriorated joints)

A Wisconsin mobile home park that underwrites at 8.5% on paper may net to 6.5–7% once climate-related operating expenses are fully accounted for. Get actual historical expense records and verify them — don’t rely on pro formas that apply Southeast expense ratios to a Midwest asset.

Due Diligence Priorities for Wisconsin Mobile Home Parks

The standard mobile home park due diligence checklist applies in Wisconsin, but certain items warrant extra weight given the climate and market profile:

- City water and city sewer: Prioritize parks connected to municipal utilities. Private well and septic systems in Wisconsin carry elevated risk due to winter vulnerability, regulatory oversight, and potential capital costs. Lagoon systems are common in rural Wisconsin and should generally be avoided unless you have specific environmental expertise.

- Infrastructure age and condition: Ask for water main and sewer line ages and materials. Clay pipe from the 1950s–1970s is common in older Midwest parks and can represent significant capital exposure. Get a camera inspection of sewer lines before closing.

- Home ownership mix: Strongly prefer tenant-owned home (TOH) parks over those with significant park-owned home (POH) inventory. Wisconsin cold winters make POH maintenance costs substantially higher than in warmer climates.

- Below-market rent documentation: Confirm current lot rents against comparable parks within a 15-mile radius. A rent survey will validate the upside thesis or reveal rents are already near market.

- Primary employment driver: Confirm the primary employers within a 30-minute commute haven’t announced plant closures or workforce reductions. Single-employer towns carry meaningful concentration risk.

For a comprehensive due diligence framework covering every major category, see: Mobile Home Park Due Diligence Checklist: 25 Things to Verify Before You Buy.

Financing a Wisconsin Mobile Home Park

Wisconsin mobile home parks are financeable through agency debt, community banks, CMBS, and seller financing. The right structure depends on deal size, asset condition, and your acquisition timeline.

- Agency debt (Fannie Mae/Freddie Mac): Available for parks meeting size and occupancy thresholds — typically 50+ lots, 85%+ occupancy, city utilities. Current rates in the 6.5–7.5% range with 25–30 year amortization. Best long-term terms but requires stabilized assets.

- Community banks: Particularly active in the Wisconsin mobile home park market. Expect 10-year terms, 20–25 year amortization, and more flexible underwriting than agency programs. Local banks with manufactured housing experience can move faster and accommodate smaller deals.

- Seller financing: Common in Wisconsin, particularly with aging owner-operators seeking installment sale tax treatment. A seller carryback on 20–30% of the purchase price can meaningfully improve early-year cash-on-cash returns.

- Bridge loans: For value-add acquisitions with occupancy below agency thresholds, short-term bridge financing funds the acquisition and initial stabilization before refinancing into permanent debt.

For a complete breakdown of mobile home park financing options across loan types, read: Mobile Home Park Financing Options in 2026: A Complete Guide.

If you’re interested in learning more about mobile home park investing or want to talk through what markets might fit your criteria, feel free to reach out — we’re happy to discuss.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Conclusion: Is Wisconsin Worth It for Mobile Home Park Investors?

Wisconsin belongs in the conversation for investors focused on the Midwest manufactured housing market. Higher cap rates, significantly below-market lot rents with a clear growth path, no rent control, a landlord-friendly statutory framework, and an aging owner base that generates ongoing off-market deal flow — these are real structural advantages that compound over a 5–7 year hold.

The cold climate introduces operational costs that require honest underwriting, and the market’s relative obscurity means deal flow takes consistent relationship-building to unlock. But for investors who do the work — who build direct owner relationships, underwrite for real climate costs, and focus on city-utilities parks in growing employment markets — Wisconsin can deliver strong risk-adjusted returns in a competitive landscape that institutional capital has largely bypassed at the deal sizes that matter to independent operators.

To see how Wisconsin stacks up against North Carolina, Tennessee, Georgia, and other target markets, see our full comparison: Best Markets for Mobile Home Park Investing in 2026: A State-by-State Guide.

Frequently Asked Questions: Mobile Home Park Investing in Wisconsin

What is the average lot rent in Wisconsin mobile home parks?

Average lot rents in Wisconsin range from approximately $365–$425 per month depending on the market — significantly below the national average of ~$752/month. This below-market positioning is one of the primary investment theses: operators can implement steady annual rent increases while still delivering exceptional affordability value to residents.

Are Wisconsin mobile home parks subject to rent control?

No. Wisconsin statute § 66.1015 prohibits municipalities from enacting rent control ordinances, including for manufactured housing communities. Wisconsin mobile home park operators can set and adjust lot rents to market rates without local regulatory restrictions.

What cap rates can I expect on Wisconsin mobile home parks?

Stabilized Wisconsin mobile home parks with city utilities and 85%+ occupancy typically trade at 7.5–8.5% cap rates. Value-add assets with occupancy or infrastructure issues may be available at 9–12% cap rates for operators with the expertise to execute a turnaround business plan.

What are the biggest due diligence risks in Wisconsin?

Cold climate infrastructure is the most Wisconsin-specific risk: aging water and sewer lines, freeze-thaw damage, high park-owned home maintenance costs, and winterization requirements all affect operating expenses in ways that don’t apply in warmer markets. Always obtain actual historical expense data and verify infrastructure ages and materials before closing.

Is Wisconsin a good state for off-market mobile home park acquisitions?

Yes. Wisconsin has a large inventory of family-owned and aging-operator parks where estate situations, retirements, and tired landlords generate ongoing off-market deal flow. Direct mail, skip tracing, and county record searches are all productive origination channels in this market. For acquisition strategies that work across all markets, see our guide to finding off-market mobile home parks.

Get the top 20 lessons from two decades of mobile home park investing — free.