I talk to a lot of mobile home park operators. And lately, almost every conversation eventually gets to the same frustration:

“I have qualified buyers. They want the home. They can afford the lot rent. But I can’t get them financed.”

This is the dirty secret of mobile home park investing right now: the manufactured home financing market has quietly collapsed for a huge segment of buyers, and operators are paying the price in persistent vacancy that their business plans never accounted for.

The Numbers Tell the Story

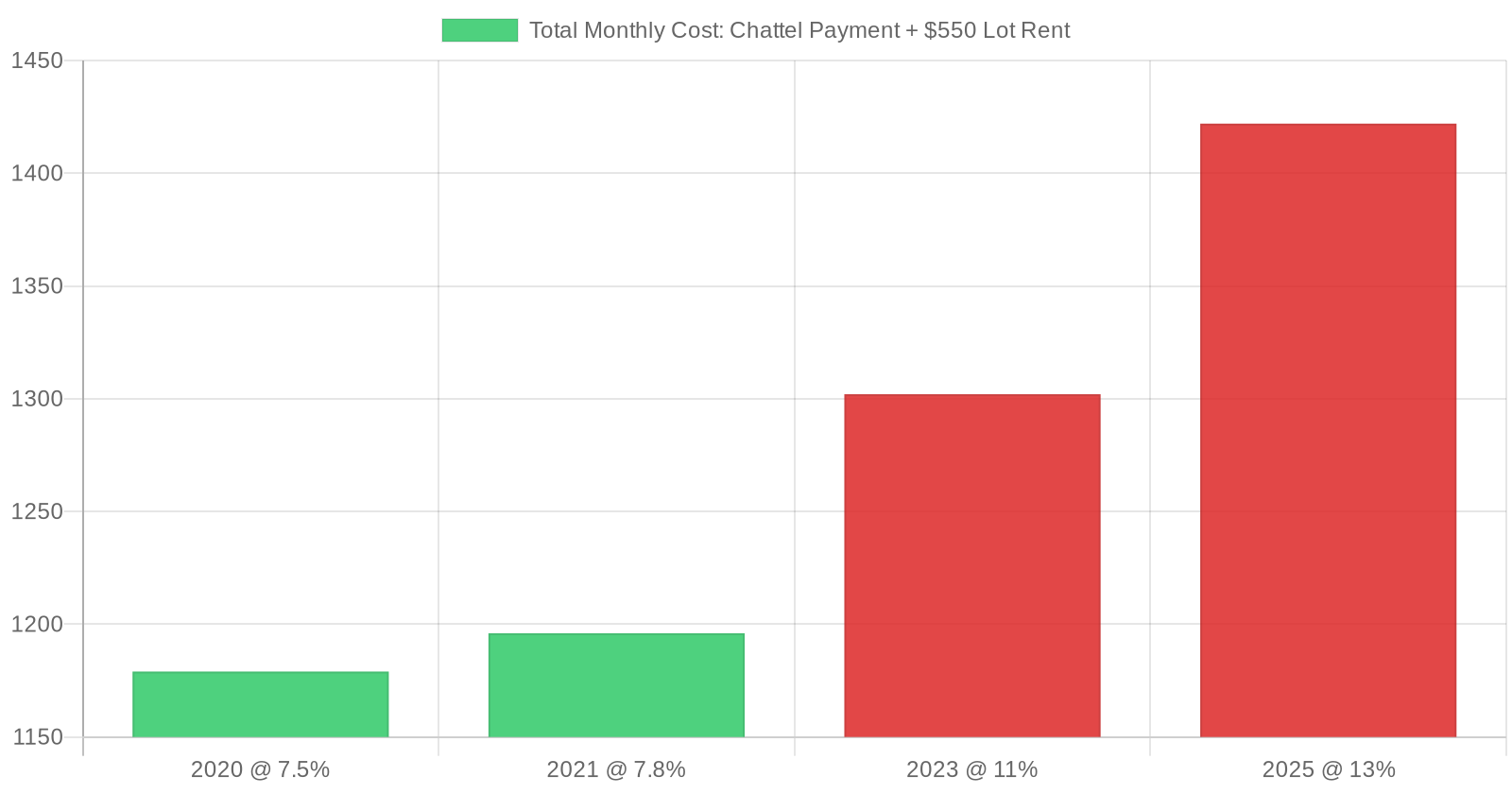

A few years ago, a manufactured home buyer with decent credit could get a chattel loan — a personal property loan for a mobile home — at 7–8%. Today, the same buyer is looking at 10–14%, depending on the lender and market. That doesn’t sound catastrophic until you run the math.

Take a $90,000 manufactured home. Old world: ~$800/month payment at 8%. New world: $1,050+/month payment at 12–13%. Add lot rent of $500–$600/month, and your resident is suddenly paying $1,600/month total.

In many of the markets we operate in — smaller Southeast cities, rural North Carolina and Tennessee — that payment competes directly with apartment rent. And apartments have granite countertops and a maintenance man. The value proposition of manufactured housing is affordability. When financing makes it no longer affordable, the buyer walks.

Why Is This Happening?

Rising interest rate environment. Chattel lending rates moved up faster and higher than conventional mortgage rates — and haven’t come down as much.

Lender consolidation. The chattel lending space is dominated by a handful of large lenders. When those lenders tighten underwriting or pull out of specific geographic markets, there’s no fallback — and they’ve been tightening.

No GSE backstop. Fannie Mae and Freddie Mac support conventional mortgages through their secondary market operations. Chattel loans don’t have that same backstop — lenders hold them on balance sheet, which limits capacity and keeps pricing elevated.

Credit score tightening. Post-COVID, lenders raised minimum FICO requirements. Many manufactured home buyers — working-class, often with thin credit files — are being screened out at the application stage before they ever see a loan offer.

How This Shows Up in Your Portfolio

If you’re experiencing any of the following, you’re feeling this problem:

- You bring in new homes but they sit for 3, 6, even 12 months without selling

- Prospects tour the home, love it, then disappear when they hit the financing wall

- Your park-owned homes are generating thin margins because you can’t convert to tenant-owned

- You’re getting pushed toward rent-to-own arrangements you’re not sure are legally compliant

This isn’t a marketing problem. It’s a financing access problem. The fix requires understanding what options actually exist for your buyers in each specific market you operate.

What’s Actually Working

Land-home packages. In some cases, you can title a manufactured home as real property instead of personal property — “retiring the title” and converting to real estate. This allows buyers to access 30-year FHA or conventional mortgages at dramatically lower rates. It requires that the home be on a permanent foundation and meet certain HUD standards, but for newer homes, it’s increasingly viable. The per-lot setup cost runs $2,000–$5,000 but can cut a buyer’s monthly payment by 25–35%.

Know which lenders are still active in your state. This sounds obvious, but the chattel lending landscape changes frequently. A lender that was writing loans in rural Tennessee six months ago may have quietly stopped. Staying current on who’s lending where — and having a list of 3–4 active options per market — is worth real money in conversion rates.

Seller financing, done right. Many operators are moving toward installment sale agreements or contract-for-deed arrangements. Structured properly — and this is key, because state laws vary significantly — this can unlock a buyer segment that conventional lenders ignore entirely. Do not do this without a housing attorney familiar with your specific state’s regulations.

Require credit-building as a lease condition. Before a tenant occupies one of your homes on a rent-to-own path, require them to enroll in a credit-building program. In 12–18 months, many residents can improve their FICO enough to qualify for conventional chattel financing. Services like Self or local credit union credit-builder loans work well for this.

Build relationships with local credit unions. Some credit unions — particularly those with community development mandates — are still writing manufactured home personal property loans at below-market rates as part of their CRA requirements. These relationships take time to build but are worth pursuing in each market you operate.

For a structured checklist of the due diligence questions you should be asking about financing access before acquiring a park with significant vacancy, the Keel Team Mobile Home Park Due Diligence Playbook covers lending market analysis as part of the pre-close process.

The Bigger Picture

The chattel financing problem isn’t going away next quarter. Solving it for your portfolio requires treating it as a strategic challenge, not a deal-by-deal headache.

The mobile home park operators who win over the next five years will be the ones who have built systems around this: they know which lenders are active in each of their markets, they have compliant seller finance programs where it makes sense, and they have a documented path to ownership that attracts and retains long-term residents.

Vacancy is always a lagging indicator. The leading indicator is whether your buyers can actually afford to buy. Start there.

Andrew Keel is the founder of Keel Team, a mobile home park investment and operating company focused on manufactured housing communities across the Southeast. He owns and operates 50+ parks across multiple states.