One of the most important skills in mobile home park investing isn’t knowing how to analyze the best-case scenario — it’s knowing how to survive the worst one.

Stress testing is the practice of deliberately modeling what happens to your investment when things go wrong: occupancy drops, expenses spike, interest rates climb, or the exit environment softens. Investors who skip this step often discover the downside after they’ve deployed capital. That’s the wrong time to learn.

This guide walks through a practical framework for stress testing any mobile home park deal before you commit — so you can size your risk accurately and enter every acquisition with open eyes.

Why Stress Testing a Mobile Home Park Deal Is Non-Negotiable

Mobile home parks are widely regarded as one of the more resilient real estate asset classes — and for good reason. Tenant turnover is extremely low, demand for affordable housing is structurally strong, and the land-lease model creates predictable, recurring revenue.

But resilient doesn’t mean bulletproof. Deals fail when buyers model only the upside and ignore how quickly net operating income can deteriorate if a few variables move the wrong way at once.

Stress testing answers the question every investor should ask before closing: What’s the worst realistic outcome — and can I survive it?

Done properly, a stress test won’t talk you out of a good deal. It will help you price risk accurately, set a disciplined maximum offer price, and structure your financing with the appropriate margin of safety. Learn more about the full investment thesis on our mobile home park investments overview.

The 5 Variables That Drive Mobile Home Park Investment Risk

A useful stress test isolates the inputs that have the biggest impact on cash flow and returns. For mobile home parks, five variables account for the vast majority of downside risk.

1. Occupancy Rate

Occupancy is the single most powerful lever in a mobile home park model. A 10-percentage-point drop in occupancy — say, from 90% to 80% — on a 50-lot park at $400 per month lot rent costs you roughly $24,000 per year in gross revenue. At a 6% cap rate, that’s $400,000 off your property value.

When stress testing occupancy, ask: What’s the park’s occupancy history? What’s the local housing market like? If the previous owner relied on park-owned homes that you plan to sell off, could occupancy temporarily dip as those homes transition to resident-owned? What’s your plan for filling vacant lots?

Stress scenarios to model: 80%, 70%, and 65% occupancy. The last one should feel uncomfortable — that’s the point.

2. Lot Rent and Revenue Growth

Most mobile home park underwriting assumes ongoing rent increases — typically 3–5% per year — based on local market rates and affordability. But what if rent increases stall due to political pressure, new state legislation, or local resistance?

Stress test your model with flat rent growth for 2–3 years. How does that change your projected IRR? If flat rents make the deal unworkable, that’s a warning sign that you’re buying too much “story” and not enough current income.

3. Operating Expense Ratio

Mobile home parks often underwrite to expense ratios of 30–40% — lower than most other commercial real estate — because tenants own their homes and utilities can be sub-metered or billed back. But expense ratios can expand quickly when:

- Infrastructure repairs are discovered post-close (water lines, septic, roads)

- Utility billing conversions take longer or cost more than expected

- Manager turnover leads to higher staffing costs

- Insurance premiums rise sharply (a real trend in 2025–2026)

Stress test to a 45–50% expense ratio. If the deal still pencils at those numbers, you have a legitimate cushion. If it doesn’t, your budget for surprises is thinner than you think.

4. Exit Cap Rate

Your projected return at sale depends heavily on what cap rate the market applies to your park at exit. If you buy at a 6.5% cap and sell into a 7.5% market, your equity erodes significantly even if NOI has improved.

Stress test your exit at 50–100 basis points above your entry cap rate. In a normalized or rising-rate environment, this is a realistic possibility. How does your projected equity multiple hold up? Is the deal still worth doing?

5. Debt Service Coverage Ratio (DSCR)

Most lenders require a minimum DSCR of 1.20–1.25x on mobile home park loans. If NOI drops — due to occupancy decline, expense increases, or flat rent — your ability to service debt tightens. In extreme cases, a covenant breach triggers a default.

Model your stressed NOI scenarios against your actual debt service. Know your break-even occupancy: the occupancy level at which your mobile home park no longer covers its debt payments. That number should be well below what you consider a realistic floor.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

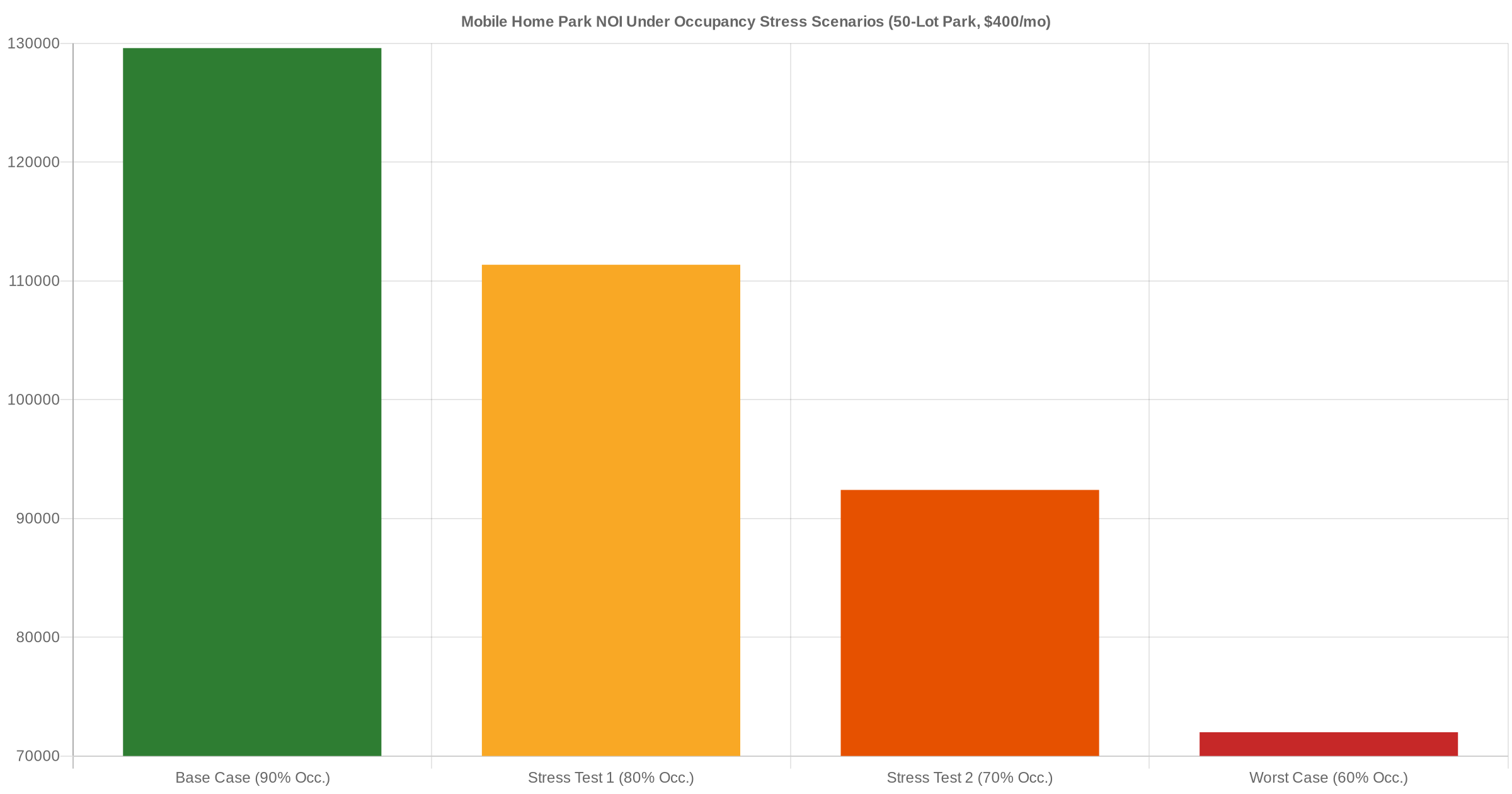

Stress Test Example: 50-Lot Mobile Home Park at $400/Month Lot Rent

Let’s walk through a concrete example to show how fast NOI — and therefore value — can move under stress.

Base assumptions: 50-lot mobile home park, $400/month lot rent, 40% expense ratio on collected revenue.

- Base Case (90% occupancy): Gross revenue = $216,000. Expenses (40%) = $86,400. NOI = $129,600. Implied value at 6.5% cap = ~$1,993,000.

- Stress Test 1 (80% occupancy): Revenue = $192,000. Expenses (42%) = $80,640. NOI = $111,360. Implied value = ~$1,713,000.

- Stress Test 2 (70% occupancy): Revenue = $168,000. Expenses (45%) = $75,600. NOI = $92,400. Implied value = ~$1,421,000.

- Worst Case (60% occupancy): Revenue = $144,000. Expenses (50%) = $72,000. NOI = $72,000. Implied value = ~$1,108,000.

If you paid $1,700,000 for this mobile home park, Stress Test 1 still gets you out even. But by Stress Test 2, you’ve lost roughly $279,000 in implied equity — before accounting for debt service. A worst-case scenario at 60% occupancy puts your equity deeply underwater if you leveraged the acquisition at 70% LTV.

That’s not a reason not to buy — it’s a reason to buy at the right price with the right equity cushion.

How to Build a Simple Mobile Home Park Stress Test Model

You don’t need a complex spreadsheet to run a useful stress test. The basics are:

- Build your base case using the seller’s rent roll, trailing 12-month financials, and your due diligence findings. (See our mobile home park underwriting guide for a step-by-step approach.)

- Create three scenarios: base, moderate stress, severe stress. Vary occupancy (±10%, ±20%), expense ratio (add 5–10 points), and exit cap rate (add 50–100bps).

- Calculate NOI for each scenario and model your equity position at exit under each.

- Identify your floor: At what occupancy level do you hit your minimum acceptable return? At what occupancy level does your DSCR fall below 1.0x?

- Back into your maximum offer price: The highest price at which even your moderate stress scenario still produces an acceptable equity multiple and maintains DSCR above 1.10x.

This exercise takes 30–60 minutes and can save you from a six-figure mistake.

Using Your Stress Test to Set a Maximum Offer Price

Here’s the practical payoff: once you’ve run your stress scenarios, you have a defensible maximum offer price — not just the number that makes your base case look good.

Experienced mobile home park operators often negotiate with sellers using their stress test results. “Here’s what we see in the financials. Here’s our base case. Here’s our downside. At your asking price, our downside scenario produces an unacceptable return. At this price, we can absorb the risk and still close.” It’s a conversation, not a confrontation.

The due diligence process is the right time to sharpen your stress test inputs — physical inspection, utility audit, rent roll verification, and title review all produce data that tightens your assumptions.

What Experienced Investors Know About Downside Risk

The operators who have been through multiple market cycles in mobile home park investing share a consistent mindset: the upside takes care of itself if you manage the downside carefully.

Mobile home parks are genuinely resilient assets. When underwritten correctly and purchased at the right basis, they tend to outperform expectations over time. But “tends to” isn’t good enough when you’re deploying significant capital. You want to know that even if things go sideways — a slow infill process, unexpected infrastructure costs, a softer exit market — you can absorb the hit and keep the asset cash-flowing.

Stress testing is how you build that confidence before you sign the closing documents, not after.

The Bottom Line

A mobile home park investment is only as strong as the assumptions behind it. The best operators don’t just model their hopes — they stress test their fears.

Before you make any offer on a mobile home park, run your occupancy, expense, and exit cap rate scenarios to their realistic worst cases. Know your floor. Know your break-even occupancy. Price the risk, not just the return.

If your deal still works under stress, you’ve found something worth pursuing. If it doesn’t, you’ve just saved yourself a very expensive lesson.

If you’re interested in learning more about mobile home park investing and how we evaluate deals, reach out and we’ll set up a call.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.