When real estate investors are looking to scale beyond single-family homes, two asset classes consistently rise to the top: mobile home parks and apartment complexes. Both offer recurring income, appreciation potential, and scalability. But they operate very differently — and understanding those differences could determine whether your portfolio thrives or stalls.

This guide breaks down both asset classes across eight key dimensions so you can decide which fits your investment goals.

Why This Comparison Matters

Apartment investing has long been the default “safe” choice for real estate investors. But mobile home park investing has quietly delivered some of the strongest risk-adjusted returns in commercial real estate over the past two decades — attracting growing attention from institutional capital and individual operators alike.

Before diving in, it’s worth noting: mobile home parks and apartments aren’t necessarily competitors. Some investors hold both. But if you’re allocating capital and need to decide where to focus, the differences matter more than most people expect.

For a full foundation on mobile home park investing, start with the Mobile Home Park Investing Guide — it covers everything from sourcing deals to underwriting and operations.

The Basics: What Each Asset Class Looks Like

Mobile home parks (also called manufactured housing communities) are land-lease communities where residents own their homes but rent the land beneath them. The operator collects lot rent — typically $250–$600/month per pad — and handles common-area maintenance and infrastructure. Residents are responsible for their own home upkeep.

Apartment complexes involve the operator owning both the land and every unit. Tenants rent the unit in its entirety, and the operator is responsible for all building maintenance, repairs, and capital expenditures inside the units.

That structural difference — own the land vs. own the units — has enormous implications for operating costs, tenant behavior, and long-term returns.

Side-by-Side: 8 Key Investing Metrics

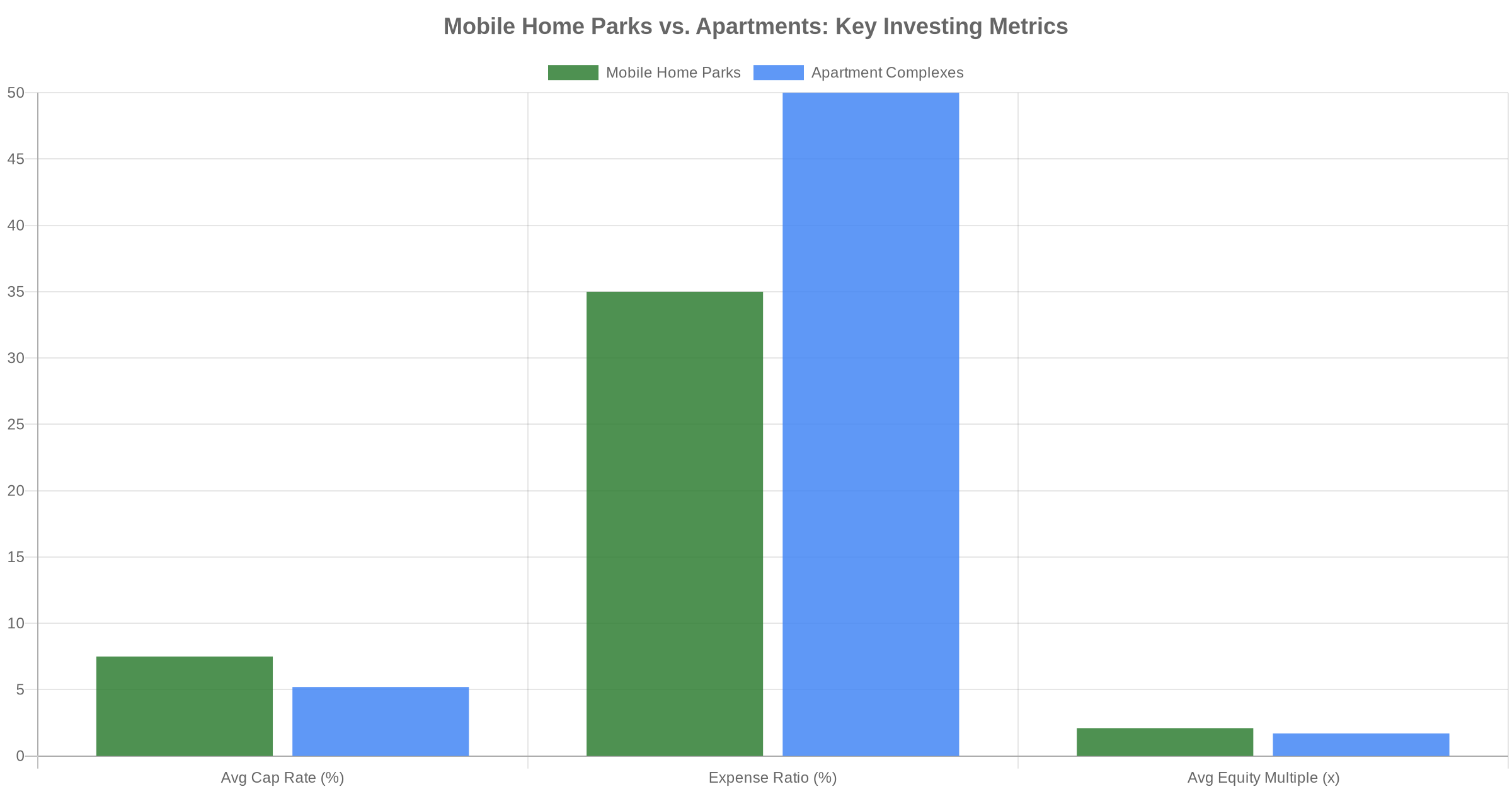

1. Cap Rates

Mobile home parks have historically traded at higher cap rates than apartments. In 2026, well-located mobile home parks in the Southeast and Midwest are trading at 6.5%–8.5% cap rates, while comparable apartment deals often land between 4.5%–6%.

Why the gap? Apartments are more familiar to institutional capital, which drives prices up and compresses yields. Mobile home parks still carry a perception discount — one that sophisticated investors are increasingly exploiting.

→ See our full breakdown: Mobile Home Park Cap Rates Explained: What’s a Good Cap Rate in 2026?

2. Tenant Turnover

This is one of the most dramatic differences between the two asset classes. Apartment turnover runs 40%–60% annually in many markets — meaning you’re replacing nearly half your tenants every year, with associated vacancy loss, cleaning, painting, leasing costs, and lost rent.

Mobile home park turnover? Typically under 5% annually. When a resident owns their home and moving it costs $5,000–$15,000, they don’t leave over modest rent increases. That retention has a compounding effect on cash flow that’s hard to overstate.

3. Operating Expenses

Mobile home parks typically run expense ratios of 30%–40% of gross income vs. 45%–55% for apartments. The reason is simple: residents own their homes. The operator isn’t responsible for HVAC systems, leaking roofs, appliance replacements, or interior repairs. Core operating expenses are property management, road and landscaping maintenance, utility infrastructure, taxes, and insurance.

In apartments, the operator owns everything inside the unit — which means every broken dishwasher, worn carpet, and failed water heater is your expense.

4. Entry Cost and Competition

Apartments in growing markets have become intensely competitive. Institutional capital — REITs, private equity firms, and large syndicators — has aggressively bought up multifamily supply, pushing valuations higher and compressing yields.

Mobile home parks still have a fragmented ownership landscape. The majority are owned by mom-and-pop operators, many approaching retirement age with no succession plan. That creates a real opportunity for off-market deals at favorable valuations — especially in target states like North Carolina, Tennessee, and Georgia.

Entry prices vary: smaller parks (under 50 lots) can trade for $500K–$2M, while institutional-quality parks (100+ lots, city utilities, high occupancy) commonly transact at $3M–$15M+.

5. Financing Options

Both asset classes have access to agency debt (Fannie Mae/Freddie Mac), CMBS loans, and bank financing. Historically, mobile home parks were harder to finance — fewer lenders understood the asset class, and parks with older homes, well/septic infrastructure, or high park-owned home ratios faced tighter lending standards.

That’s changed considerably. Agency lenders now actively pursue manufactured housing community loans, and financing for well-operated mobile home parks is more accessible than it was even five years ago.

→ Related: How to Finance a Mobile Home Park: Loan Options Explained

6. Recession Resilience

Mobile home parks tend to outperform apartments during economic downturns for a few key reasons:

- Lot rents represent the most affordable housing option in most markets

- Residents can’t easily move their homes, creating strong retention even under financial stress

- Demand for affordable housing increases during recessions, not decreases

Apartments — particularly Class A and B properties — can see meaningful rent softening as tenants trade down or double up. Mobile home parks, by contrast, often see increased demand and lower vacancy when the broader economy contracts.

→ Deep dive: How Mobile Home Parks Perform During a Recession

7. Value-Add Potential

Both asset classes offer genuine value-add opportunities, but the playbooks look different.

Mobile home parks: Fill vacant lots (infill), raise below-market rents, transition from park-owned homes to tenant-owned homes, sub-meter utilities to bill back residents, and improve management operations. A 100-lot park with 30 vacant lots has massive upside if those pads can be filled at $400/month — that’s $144,000 in additional annual gross income without adding any new structures.

Apartments: Renovate units (kitchen and bath upgrades), add amenities, rebrand the property, reduce vacancy through better leasing systems, and improve operational efficiency.

Mobile home park infill is one of the most powerful value-add levers in real estate — filling a pad costs a fraction of what adding a new apartment unit would cost, and it creates a long-term paying tenant who owns their own home.

8. Regulatory Risk

Both asset classes face increasing regulatory attention, but the risks look different.

Apartment operators face rent control legislation in many metros, tenant protections limiting evictions, and zoning changes affecting new supply.

Mobile home parks face a specific and growing risk: state legislatures are passing tenant protection laws that restrict lot rent increases, require longer notice periods before closure, and create right-of-first-refusal rights for resident associations. These regulations vary dramatically by state. North Carolina, Tennessee, and Georgia currently have more operator-friendly regulatory environments, though that landscape continues to evolve.

Before you choose an asset class, get the inside track on what experienced operators know. This free guide covers the lessons that matter most — from underwriting to operations to exit strategy.

Which Investment Type Is Right for You?

There’s no universal answer — but here’s a practical framework.

Mobile home park investing may be a better fit if you:

- Want higher initial yields and strong day-one cash flow

- Prefer lower operating complexity (residents own their homes)

- Are comfortable operating in a fragmented, less liquid market

- Want exposure to the affordable housing demand tailwind

- Are willing to learn a niche asset class with less institutional competition

Apartment investing may be a better fit if you:

- Want greater liquidity and a larger buyer pool at exit

- Prefer a more institutional, well-understood asset class

- Are operating in markets where multifamily has strong rent growth dynamics

- Have or can hire experienced multifamily management teams

Many of the most sophisticated real estate investors we speak with hold both — using apartments for liquidity and mobile home parks for yield, recession resilience, and long-term tenant stability.

The Bottom Line

Mobile home park investing and apartment investing each have genuine strengths. But for investors focused on cash flow, lower operating expenses, and recession resilience, mobile home parks offer a compelling combination that’s difficult to match in today’s multifamily market.

The trade-off is a steeper learning curve, a more fragmented market, and operational nuances that require the right knowledge to navigate. The good news: the educational resources available today make it easier than ever to get started.

If you want to go deeper on evaluating mobile home park deals, our Mobile Home Park Investing Guide covers underwriting, due diligence, and what separates a great deal from a costly mistake.

Ready to evaluate your first (or next) mobile home park deal? The Due Diligence Playbook includes 10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of vetting a mobile home park investment.

Download Top 20 Things I’ve Learned from Investing in Mobile Home Parks — a practitioner’s guide packed with real lessons from the field.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.