If you’ve ever researched passive investing in real estate syndications — or you’re about to write your first check — you may have come across the term capital call. It’s one of those phrases that can send a chill down a passive investor’s spine, and for good reason.

In this guide, we’ll break down exactly what a capital call is in the context of a mobile home park syndication, why it happens, how often it occurs, and what you should ask a sponsor before you ever wire a dollar.

What Is a Capital Call?

A capital call — sometimes called an “additional capital contribution” — is a request from the general partner (GP) of a real estate syndication asking limited partners (LPs) to contribute additional money beyond their original investment.

In a mobile home park syndication, this typically happens when the deal runs into unexpected costs or cash flow problems that the original equity raise didn’t account for. The GP contacts investors and says, in effect: “We need more capital to keep this deal alive. Can you put in more?”

Capital calls are one of the more uncomfortable realities of passive investing. They’re not common in well-structured deals with experienced operators — but they do happen. Understanding them before you invest protects you from being blindsided.

Why Do Capital Calls Happen in Mobile Home Park Syndications?

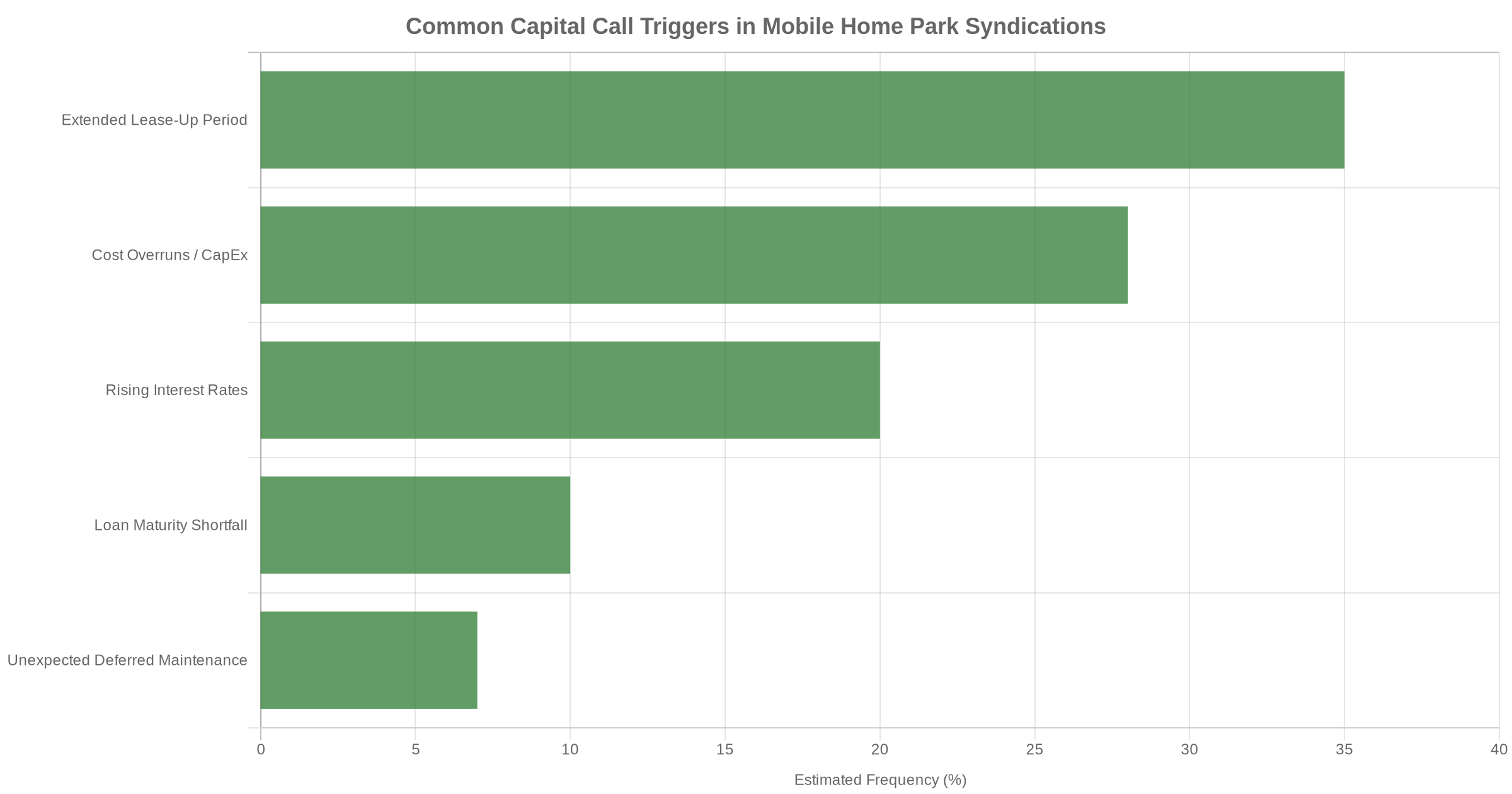

There are several scenarios that can trigger a capital call in a mobile home park deal:

1. Extended Lease-Up Periods

Many mobile home park syndications are value-add deals — the sponsor acquires a park below market and fills vacant lots to increase occupancy and income. If lease-up takes longer than projected due to home supply issues, permitting delays, or slower local demand, cash flow may be insufficient to cover debt service. The sponsor then has to choose between defaulting on the loan, selling the asset at a loss, or calling capital from investors.

2. Cost Overruns on Value-Add Projects

Infrastructure upgrades like water line replacement, road resurfacing, or bringing in new homes can go over budget. When costs exceed the capital reserves set aside at closing, a capital call may be the only way to fund the shortfall.

3. Rising Interest Rates on Floating-Rate Debt

Syndications that used floating-rate bridge loans were hit hard during the 2022–2023 rate cycle. When debt service obligations jumped sharply, many deals needed additional capital to avoid default. This remains a risk for deals carrying variable-rate financing.

4. Loan Maturity Without a Refinance Option

When a bridge loan matures and the property can’t refinance into permanent debt — because the business plan isn’t complete or values have declined — lenders may require a paydown or additional reserves as a condition of extending. That money has to come from somewhere, and often it comes from the LPs.

5. Unexpected Deferred Maintenance

Due diligence can uncover most major issues, but not all. A failing septic system, aging electrical infrastructure, or a private water system that needs significant repair can surface after closing. These unexpected capital expenditures can drain reserves quickly.

Are Capital Calls Mandatory?

This is the critical question — and the answer depends entirely on your syndication’s operating agreement.

In some syndications, capital calls are mandatory. If you don’t contribute, you face dilution (your ownership percentage is reduced) or, in extreme cases, partial forfeiture of your interest. In others, capital calls are voluntary — you can decline, but those who contribute receive preferential returns or additional equity at the expense of those who don’t.

Before investing in any mobile home park syndication, read the Private Placement Memorandum (PPM) carefully for language around additional capital contributions, dilution provisions, and what happens if you decline. If you’re not sure what you’re looking for, our guide on how to read a mobile home park syndication PPM is a good starting point.

How Common Are Capital Calls?

In well-underwritten mobile home park deals with conservative sponsors, capital calls are relatively rare. Experienced operators typically:

- Build larger capital reserves at closing

- Use conservative rent and occupancy projections

- Have lender relationships that allow for flexible terms

- Stress-test their deals against multiple scenarios, including rate hikes and slower lease-up

The deals most likely to result in capital calls are those underwritten with aggressive assumptions, thin reserves, or heavy floating-rate debt — particularly deals done at peak pricing in 2021 and 2022. The current market cycle has seen elevated distress in deals that were over-leveraged or under-reserved during that period.

This is why evaluating the sponsor is as important as evaluating the deal itself. A seasoned operator with a track record of navigating multiple market cycles is far less likely to come back asking for more money. Knowing how to evaluate a mobile home park operator before you invest is one of the most important skills a passive investor can develop.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

How to Protect Yourself as a Passive Investor

You can’t eliminate the risk of capital calls entirely, but you can substantially reduce it with the right due diligence upfront.

Ask About Capital Reserves

What reserves are being set aside at closing? A deal with only 3–6 months of reserves is far more vulnerable than one with 12+ months. Ask the sponsor to walk you through their reserve assumptions and what scenarios could exhaust them.

Understand the Debt Structure

Is the loan fixed-rate or floating? When does it mature? What are the extension options? A 3-year bridge loan with two 1-year extensions gives far more breathing room than a loan with limited flexibility. Understanding the full GP/LP structure of the deal — including how debt is structured — is essential before committing capital.

Review Business Plan Assumptions

What occupancy rate is the deal underwritten to? What rent growth is projected year over year? Conservative deals model below-market rent growth and leave room for error. If a sponsor is projecting 20%+ rent increases in year one, that’s a yellow flag worth probing before you invest.

Check the Sponsor’s Track Record

Has the sponsor ever issued a capital call on a prior deal? If so, what happened, and how did they handle it? Sponsors who have navigated difficult deals successfully have demonstrated something valuable. Sponsors who haven’t been tested yet are an unknown quantity.

Know Your Own Liquidity

Could you meet a capital call if one came? Passive investing in mobile home parks should be done with capital you don’t need in the short term. If a capital call would put you in financial difficulty, that’s critical to understand before you invest — not after.

Red Flags That Increase Capital Call Risk

Certain deal characteristics and sponsor behaviors increase the probability of a capital call down the road. Watch for:

- Thin or no capital reserves: Any deal with less than 6 months of operating reserves at closing is taking on unnecessary risk.

- Aggressive rent growth projections: Pro formas that assume large year-over-year rent increases leave little margin for error.

- Heavy floating-rate bridge financing: Variable-rate debt amplifies interest rate risk and can be a capital call trigger if rates move against you.

- Sponsor overextension: A GP managing too many deals simultaneously may not catch problems early enough to course-correct before they become capital events.

- Vague PPM language: If the operating agreement is unclear about your rights and obligations in the event of a capital call, clarify before you sign — not after.

For a broader look at deal-level warning signs, see our guide on mobile home park syndication red flags to watch for before you invest.

What Happens If You Can’t or Won’t Meet a Capital Call?

The outcome depends on the operating agreement, but common scenarios include:

- Dilution: Your ownership percentage is reduced in proportion to your non-contribution. Those who do contribute get a larger share of the deal going forward.

- Preferred returns for contributors: Some agreements give capital call contributors a preferred return on the new capital before distributions flow to non-contributors.

- Full dilution or forfeiture: In extreme cases, failing to meet a mandatory capital call can result in significant reduction or total loss of your interest. This is uncommon in well-structured deals but does happen.

None of these outcomes are favorable for passive investors who don’t participate. That’s why understanding the capital call provisions before investing — not after — is so important.

Final Thoughts: Capital Calls Are Rare in the Right Deals

Capital calls are a legitimate risk in mobile home park syndication investing — but they’re not inevitable. The best operators build deals that can weather storms without going back to investors for more money. Conservative underwriting, adequate reserves, and disciplined debt structures are the hallmarks of sponsors who know how to protect their limited partners.

As a passive investor, your job is to ask the right questions before you commit. Understand the capital call provisions in your operating agreement. Know the debt structure. Evaluate the sponsor’s track record. And only invest capital you can afford to have illiquid — or potentially called back into the deal — if things don’t go perfectly.

The best mobile home park syndications deliver strong, consistent returns precisely because the operators running them build in the margin of safety to handle the unexpected. Those are the deals — and the sponsors — worth finding.

To learn more about how mobile home park syndications are structured from top to bottom, visit our complete guide to mobile home park syndication.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.