If you’ve spent any time evaluating mobile home park deals, you’ve likely encountered the terms tenant-owned homes (TOH) and park-owned homes (POH). On the surface, the distinction seems simple — either the resident owns their home, or the mobile home park does. But beneath that simple difference lies one of the most important variables in mobile home park investing: it affects your operating expenses, your cap rate, your financing options, and ultimately, the long-term value of the asset.

Understanding the TOH vs. POH dynamic isn’t just a due diligence checkbox. It shapes your entire investment thesis. Here’s what every serious mobile home park investor needs to know.

What Is a Tenant-Owned Home (TOH)?

A tenant-owned home is exactly what it sounds like: the resident owns the physical structure of the home, and the mobile home park owner owns the land underneath it. The resident pays lot rent — a monthly fee for the right to place their home on the park’s land — but they are responsible for maintaining and insuring their own home.

This is the traditional model for manufactured housing communities and the structure that most experienced operators prefer. The park’s revenue stream is pure lot rent, the operating expenses are lower, and the relationship between the park and the resident more closely resembles a landlord-tenant relationship in a land-lease community than it does traditional property management.

TOH residents tend to stay put. Moving a manufactured home is expensive — often $5,000 to $10,000 or more — so once someone plants their home on a lot, they rarely leave. This is a core driver of one of mobile home park investing’s most powerful advantages: exceptionally low tenant turnover.

What Is a Park-Owned Home (POH)?

A park-owned home is a unit that the mobile home park owner purchased and rents out to a resident — similar to a traditional rental property, but located within the community. The resident pays a combined rent covering both the lot and the home itself.

Park-owned homes are common in communities that have gone through periods of high vacancy. When lots sit empty and no new homes are being brought in, operators sometimes purchase used manufactured homes and rent them out as a way to generate revenue from otherwise idle land. In some markets, park-owned home portfolios are intentional — designed to serve residents who can’t qualify for chattel financing.

The problem is that park-owned homes carry all the headaches of traditional property management: maintenance, repairs, tenant turnover, pest remediation, and unit-level capital expenditures. They significantly increase the operational complexity and expense of running a mobile home park.

Why the TOH/POH Ratio Is One of the Most Important Metrics in Mobile Home Park Investing

Experienced operators look at the TOH percentage almost immediately when evaluating a deal. The reason is straightforward: TOH communities are simply more profitable, more stable, and more valuable per dollar of NOI.

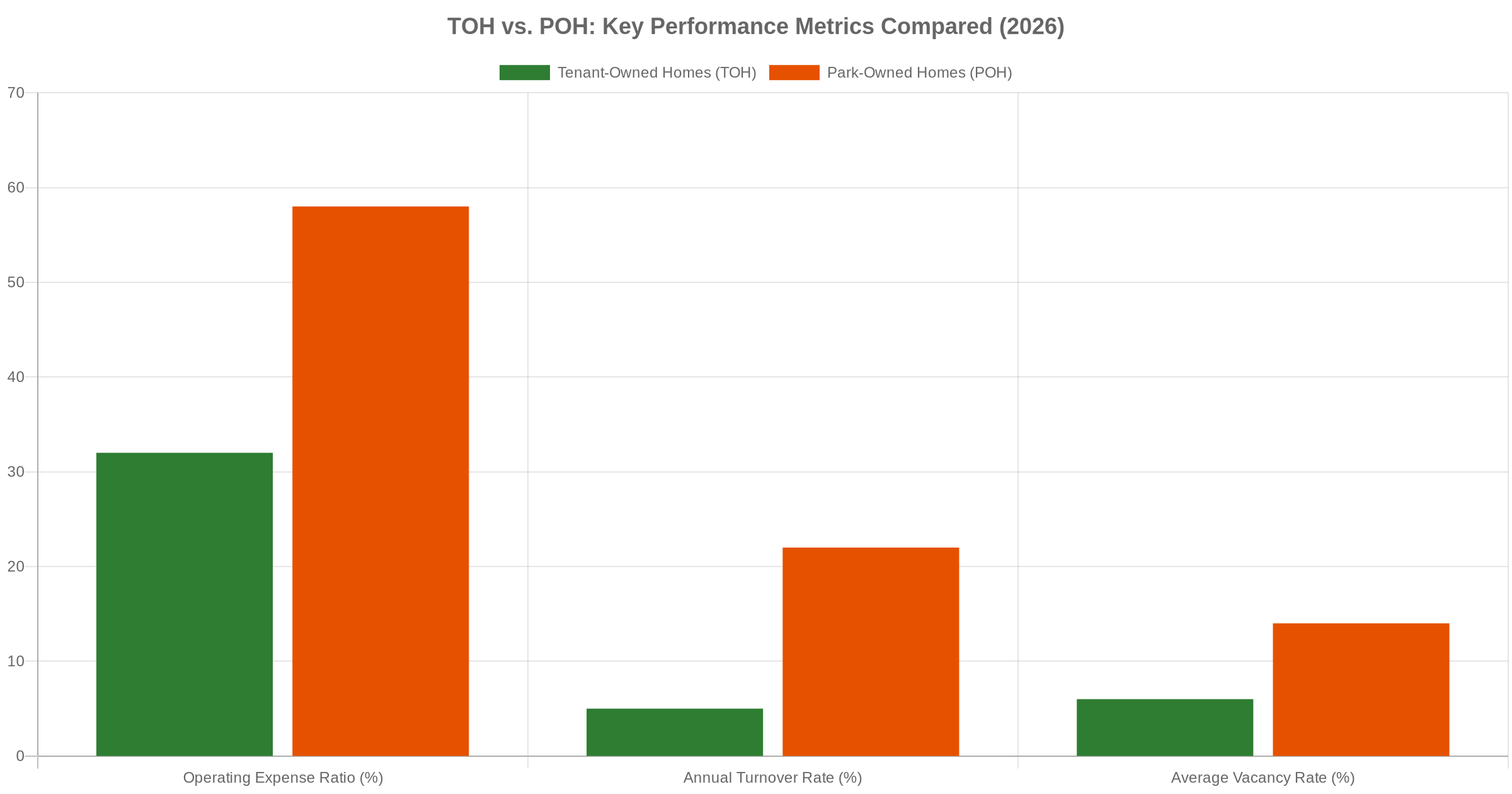

Here’s what the data shows for the typical TOH-dominant community vs. a POH-heavy community:

- Operating expense ratio: TOH communities average 30–35% of gross revenue. POH-heavy communities can run 55–65% or higher once you factor in maintenance, unit repairs, and elevated turnover costs.

- Annual turnover rate: TOH residents move out at roughly 3–7% per year. POH tenants, who have no ownership stake in their home, turn over at rates of 15–25% or more.

- Vacancy risk: When a TOH resident leaves, they typically sell their home to the next occupant. When a POH resident vacates, the operator is left holding a unit that may need repairs and is sitting idle — with no lot rent income until the next tenant moves in.

These differences compound over time. A 100-lot mobile home park that is 90% TOH and 80% occupied will almost always outperform a 100-lot park that is 50% POH at 95% occupancy — both in terms of NOI consistency and exit value.

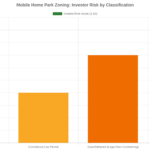

How POH-Heavy Portfolios Affect Cap Rates and Valuation

When a mobile home park has a significant park-owned home component, buyers — and lenders — apply a haircut. There are two reasons for this.

First, POH revenue is inherently less stable than lot rent. Lot rent is contractual and tied to the land; POH income depends on continuous occupancy, unit condition, and the operator’s ability to manage individual rentals. Buyers discount this revenue accordingly.

Second, POH-heavy communities trade at higher cap rates (meaning lower prices per dollar of NOI) because buyers must factor in the ongoing capital expenditure requirements to maintain the housing stock. A community that is 40% POH may trade at a 9–10% cap rate even if its NOI looks attractive, while a comparable TOH-dominant park might trade at a 6–7% cap rate.

This matters for underwriting. If you’re evaluating a deal and the seller is using blended POH rent in the NOI calculation without discounting it, you may be overpaying. Separate the lot rent revenue from the home rent revenue and evaluate them independently. Our mobile home park due diligence checklist walks through exactly this kind of revenue disaggregation.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Financing Implications: What Lenders Think About Park-Owned Homes

Lenders care about the TOH/POH ratio too — and for similar reasons. Agency lenders (Fannie Mae and Freddie Mac) have clear guidelines around community loan programs, and POH-heavy parks often don’t qualify for the most favorable loan products.

Fannie Mae’s manufactured housing community loan program, for example, generally requires that a community derive the majority of its income from lot rent — not unit rental. If a community’s NOI is substantially driven by POH rents, it may be ineligible for agency financing entirely, pushing borrowers into more expensive conventional bank or CMBS products. Our complete guide to mobile home park financing covers all loan types and their requirements in detail.

This financing gap between TOH-dominant and POH-heavy parks further widens the cap rate spread — because the universe of qualified buyers is smaller for POH communities, which means less competition and lower prices.

The POH-to-TOH Conversion: One of the Best Value-Add Plays in Mobile Home Park Investing

Here’s where the POH situation becomes interesting from an investment standpoint: converting park-owned homes to tenant-owned homes is one of the clearest value-add strategies in the asset class.

The playbook works like this. You acquire a community with a meaningful POH percentage — say, 25–40% of units. You then work to sell those homes to qualified residents, either for cash or through a third-party chattel lender. Once the home transfers to resident ownership, your operating expenses drop (no more maintenance liability for that unit), your NOI becomes more predictable, and the cap rate the community deserves improves — which directly increases the value of the asset.

This isn’t a theoretical strategy. It’s one of the most repeatable value-add levers available to active mobile home park operators, particularly in communities that have been under-managed or where a previous owner accumulated homes through defaults. Learn more about value-add strategies that consistently improve mobile home park NOI.

The key variables to evaluate when underwriting a POH-to-TOH conversion:

- Home condition: Are the units in good enough shape to sell, or will they need significant rehab investment first?

- Market demand: Is there adequate demand from prospective residents who can qualify for chattel financing?

- Chattel lender relationships: You’ll need a lending partner — companies like 21st Mortgage, Triad, or Vanderbilt — who can underwrite buyers in your market.

- Pricing and timeline: How much can you realistically net per home sale, and how long will the full conversion take? Underwrite conservatively.

What to Look for During Due Diligence

When reviewing a potential acquisition, here’s how to assess the TOH/POH situation properly:

- Request a unit-by-unit rent roll that identifies each lot as TOH or POH, along with the monthly revenue attributable to each.

- Walk the community and visually assess POH units. Age, condition, and size matter enormously when estimating conversion costs or long-term cap-ex.

- Review title records to confirm which homes are actually on the park’s title. Some communities have units that are effectively park-operated but technically titled to deceased residents or LLCs — a red flag that requires legal cleanup.

- Analyze maintenance expense history for POH units specifically. Request work orders or maintenance logs broken out by unit.

- Model both scenarios: Stabilized NOI as-is (current POH mix) vs. projected NOI after full conversion. This gives you the value-add upside in dollar terms.

Conclusion: Prioritize TOH — But Don’t Walk Away from POH Opportunities

All else equal, you want to buy mobile home park communities with a high TOH percentage. They’re more efficient to operate, more stable in their revenue, easier to finance, and command premium valuations at exit. For passive investors evaluating syndication sponsors, asking about a portfolio’s average TOH percentage is a smart due diligence question.

That said, POH-heavy communities can represent genuine opportunity — if the price reflects the risk, the homes are in sellable condition, and the operator has a credible conversion plan. Some of the best value-add deals in the mobile home park space come from communities where a previous owner accumulated a large park-owned home inventory and let the NOI suffer as a result.

The key is entering with eyes open. Understand exactly what you’re buying, model the conversion math carefully, and account for both the time and capital required to execute. When it works, a successful POH-to-TOH conversion can dramatically increase a community’s value in a relatively short hold period.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Frequently Asked Questions

What percentage of a mobile home park should be tenant-owned homes?

Most experienced operators prefer communities where 75% or more of homes are tenant-owned. Communities with 90%+ TOH are considered premium and command the tightest cap rates. That said, markets vary — in some regions, a 60–70% TOH community may be typical and acceptable, especially if priced correctly and if a conversion strategy is feasible.

Can you get agency financing on a park with a lot of park-owned homes?

It depends on the ratio. Fannie Mae and Freddie Mac community lending programs generally require that the majority of a community’s income comes from lot rents, not unit rents. Communities where park-owned home revenue is a large share of total income often cannot qualify for agency debt and must rely on conventional bank loans, CMBS, or seller financing — which typically carry higher rates and shorter terms.

How do you convert park-owned homes to tenant-owned homes?

The most common path is to sell the home directly to the current resident (who may finance it through a chattel lender) or to a new resident purchasing the home as part of their move-in. Operators work with chattel lenders like 21st Mortgage, Triad Financial Services, or Vanderbilt Mortgage to qualify buyers. In some cases, operators use seller-financed note structures when chattel lenders aren’t available in a market.

Do park-owned homes affect the sale price of a mobile home park?

Yes, significantly. Buyers apply a discount to POH revenue in their NOI calculations because it’s less stable than lot rent. POH-heavy communities also face a smaller buyer pool due to financing constraints, which reduces competitive bidding and pushes cap rates higher (meaning lower sale prices relative to NOI). A community in the process of a successful POH-to-TOH conversion can see meaningful value appreciation as the ratio improves.

Is it ever worth buying a mobile home park that is mostly park-owned homes?

It can be — if the price is right and you have a clear execution plan. The critical factors are home condition (are they sellable?), local demand (can buyers qualify for chattel financing?), and lender relationships. Operators who have successfully executed POH-to-TOH conversions multiple times often seek out these deals specifically because the value-add upside is well-defined and repeatable.

Get the top 20 lessons from two decades of mobile home park investing — free.