When you invest passively in a mobile home park syndication, your capital goes to work — and eventually, it comes back to you. But how, when, and in what form depends almost entirely on the exit strategy your operator has planned from day one.

Exit strategies aren’t a footnote in a mobile home park syndication. They’re central to how returns are structured, how long your capital is tied up, and how much you ultimately walk away with. Understanding the mechanics of syndication exits before you commit capital can mean the difference between a smooth outcome and a frustrating surprise.

What Is an Exit Strategy in a Mobile Home Park Syndication?

An exit strategy is the planned method by which a syndicator monetizes the equity position and returns capital — plus profits — to investors. In a typical mobile home park syndication, the General Partner (GP) acquires the property, executes a business plan over a defined hold period, and then “exits” the investment through one of several mechanisms.

Most syndication offering documents specify a projected hold period — typically three to seven years — and identify which exit strategy the sponsor plans to use. Some deals have a clearly defined single path; others include contingency options depending on market conditions when the exit window arrives.

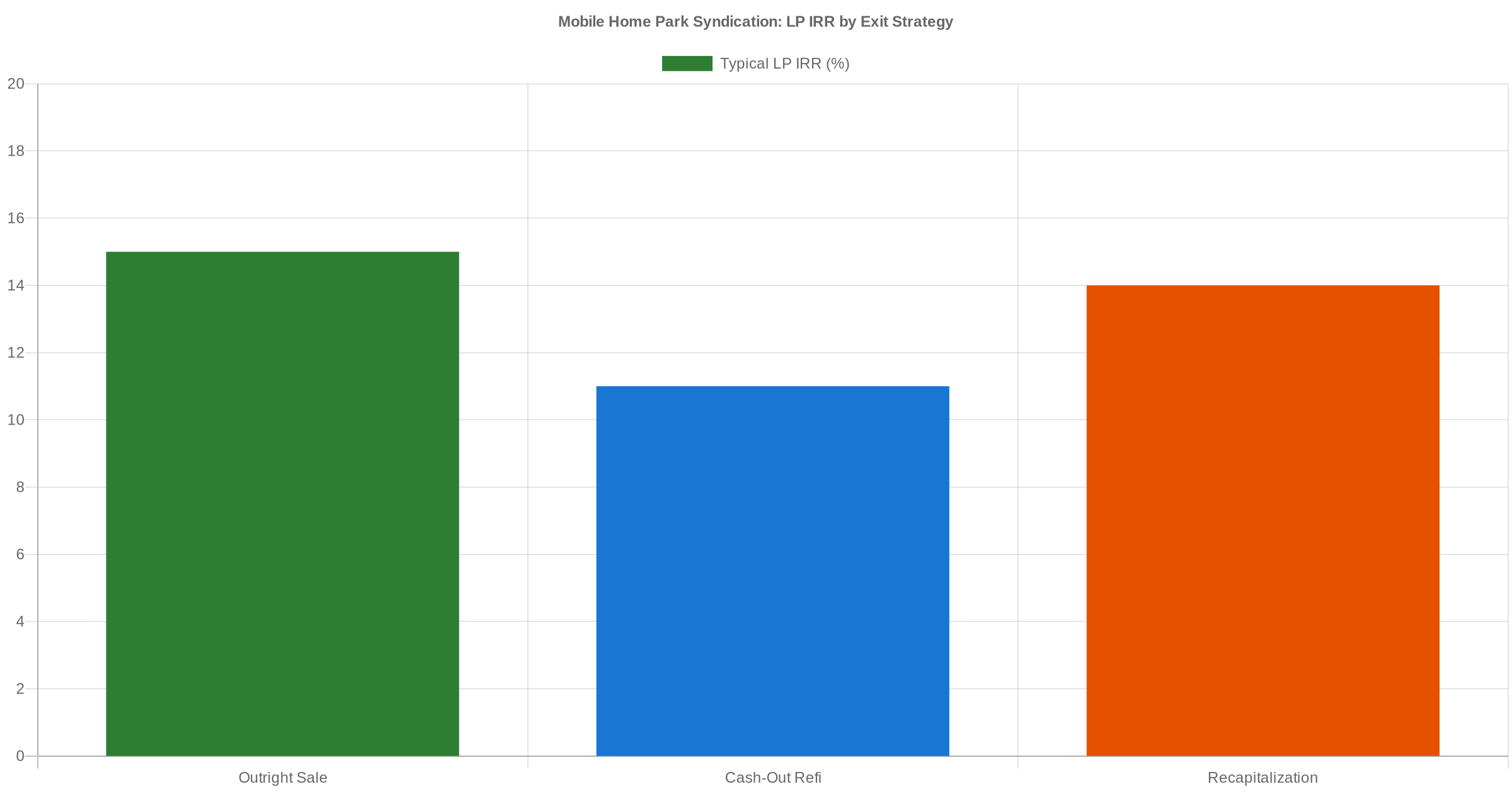

The Three Primary Exit Strategies in Mobile Home Park Syndications

1. Outright Sale

The most common exit strategy in mobile home park syndications is a straightforward sale of the property to a third-party buyer. After improving operations, raising lot rents, and filling vacant lots, the operator lists the mobile home park for sale — typically targeting institutional buyers, regional operators, or other syndicators.

When the sale closes, proceeds follow the waterfall structure outlined in the operating agreement: debt gets paid off, then investors receive their equity back, then profits are split between the LP and GP according to agreed terms — typically after the LP has cleared a preferred return threshold.

This is the simplest exit for passive investors to understand: your capital returns, your profit share is calculated, and the investment closes.

2. Cash-Out Refinance

Some operators choose to refinance the property rather than sell it. If a mobile home park has appreciated significantly — through a combination of lot rent increases and improved occupancy — the sponsor may refinance into new debt at a higher loan amount, pulling out equity in the process and distributing it to investors.

The key difference from a sale: the investment continues. Passive investors receive a distribution from the refinance proceeds, but their equity position remains in the deal and continues generating cash flow. This is a partial return of capital, not a full exit — but it can deliver meaningful liquidity while preserving long-term upside.

3. Recapitalization

A recapitalization (“recap”) brings in new equity partners — often at the institutional level — to buy out existing investors and fund the next phase of the business plan. Original LP investors are paid out, and the deal continues under a new ownership structure.

Recaps are more common in larger deals or when the operator wants to execute a longer-term strategy beyond the original hold period. For passive investors, a recap functions similarly to a sale — you receive your equity and profit distributions — but the mechanics are more complex and timing can be less predictable.

How Returns Are Distributed at Exit

In most mobile home park syndications, exit distributions follow the waterfall established in the operating agreement. A typical structure works like this:

- Step 1: Remaining debt is paid off from sale proceeds

- Step 2: Closing costs, disposition fees (typically 1–2%), and any remaining reserves are deducted

- Step 3: LP investors receive return of their original capital contribution

- Step 4: LP investors receive any accrued but unpaid preferred return

- Step 5: Remaining profits are split — commonly 70/30 or 80/20 (LP/GP) after clearing an IRR hurdle

The exact mechanics vary by deal. Some structures have a single profit split; others use tiered splits where the GP earns a larger share after the LP clears certain return thresholds (known as a “promote”). Understanding the waterfall before you invest is essential — the difference between an 80/20 and 70/30 split can meaningfully affect your total return. For a detailed breakdown, read our guide on mobile home park syndication GP/LP structure and return waterfalls.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

What Drives Exit Timing?

Hold periods in mobile home park syndications are projections, not guarantees. Several factors can push an exit earlier or later than planned:

- Interest rate environment: Rising cap rates compress valuations and may push operators to hold longer before selling at target returns

- Business plan completion: If infill or lot rent increases take longer than projected, the operator may need additional time to optimize the property before sale

- Buyer market conditions: Institutional demand for mobile home parks fluctuates. A strong seller’s market may prompt an early exit; a slow market may require patience

- Loan terms: Prepayment penalties and loan maturity dates often drive timing — a loan with significant defeasance penalties won’t be paid off early without real cost

- Operational performance: Well-run deals tend to hit their projections; deals with execution challenges may require more time before the property reaches target value

Most experienced sponsors build flexibility into their operating agreements to extend hold periods by one to two years if market conditions warrant. This is standard and reasonable — but it’s worth confirming the extension provisions before you invest.

Red Flags: When Exit Strategies Change Mid-Deal

A change in exit strategy isn’t always a warning sign — markets shift, and experienced operators adapt. But certain changes should prompt deeper questions from passive investors:

- Switching from a planned sale to a refinance without explanation may signal the property isn’t at a value that supports a profitable sale

- Repeated hold period extensions beyond the operating agreement’s stated provisions may indicate operational problems or projections that were too aggressive from the start

- A proposed recapitalization that rolls your equity into a new vehicle without a full distribution deserves careful scrutiny — it can be a legitimate strategic move, but it can also obscure underperformance

- Lack of investor communication as the projected exit date approaches is a red flag regardless of which strategy the operator ultimately chooses

The best mobile home park operators communicate proactively — months before a projected sale, not weeks. Regular updates, transparent timelines, and honest reporting about market conditions are signs of a sponsor who respects your capital. Learn more about evaluating operators at our mobile home park syndication resource hub.

How to Evaluate a Sponsor’s Exit Track Record Before You Invest

Before writing a check into any mobile home park syndication, ask the operator directly about their exit history:

- How many deals have you fully exited?

- What was the average actual hold period compared to your original projection?

- What was the actual LP IRR versus projected IRR at exit?

- Have you ever changed exit strategies mid-deal? Why, and what was the outcome for investors?

- What is your disposition process — do you list on the open market, work with brokers, or target specific buyer types?

Track record matters more than projections. An operator who has successfully exited multiple deals — and can walk you through the specifics with real numbers — demonstrates the execution ability that pro forma projections alone can’t prove. See our full guide on how to evaluate a mobile home park operator for a comprehensive framework.

Conclusion: Exit Strategy Is Where Your Returns Actually Live

Every element of a mobile home park syndication — the business plan, the debt structure, the hold period, the waterfall — ultimately flows through the exit. It’s where the projections either prove out or they don’t.

As a passive investor, your job isn’t to execute the exit — it’s to evaluate whether the sponsor’s strategy is realistic, the timeline is defensible, and the track record backs it all up. Ask the right questions before you invest, and you’ll have a much clearer picture of what to expect when the deal finally closes.

If you’re interested in learning more about mobile home park investing, feel free to reach out and set up a call — we’re happy to walk through the landscape with you.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.