When most passive investors evaluate a mobile home park syndication, they focus on the projected returns, the operator’s track record, and the quality of the market. What often gets less attention — but deserves just as much scrutiny — is the debt structure.

How a mobile home park syndication is financed matters enormously. The type of loan, the term length, the interest rate environment, and the refinancing plan can all significantly affect whether a deal performs as projected — or runs into serious trouble. Understanding mobile home park syndication debt is one of the most important skills a passive investor can develop.

This guide breaks down how mobile home park syndications handle debt, what refinancing risk looks like in practice, and what questions every limited partner should ask before writing a check.

What Type of Debt Do Mobile Home Park Syndications Use?

Not all loans are the same, and the type of debt in a syndication deal has major implications for both risk and return. Most mobile home park deals use one of three primary loan structures.

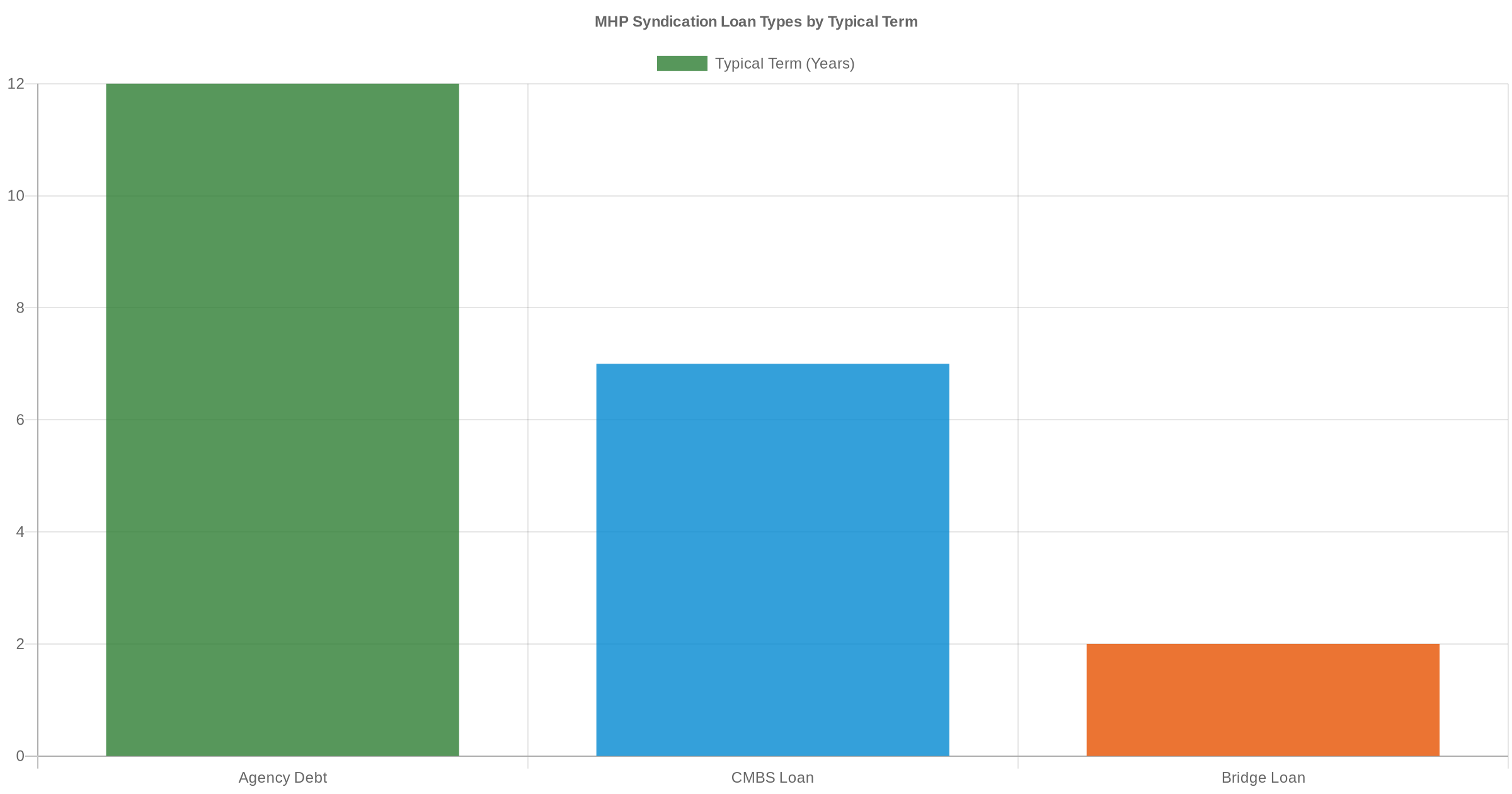

Agency Debt (Fannie Mae / Freddie Mac)

Agency loans through Fannie Mae or Freddie Mac are often the gold standard for stabilized mobile home park acquisitions. These loans typically offer:

- Fixed interest rates for 10 to 15 years

- Non-recourse structure (the loan is secured by the property, not the sponsor personally)

- Loan-to-value ratios of 65–75%

- Strong prepayment protections (yield maintenance or step-down)

Agency debt is ideal for stabilized properties where the operator isn’t planning major repositioning. The long fixed-term removes most near-term refinancing risk for passive investors.

CMBS Loans (Commercial Mortgage-Backed Securities)

CMBS loans are another common option for larger mobile home park acquisitions. They offer fixed rates and are also non-recourse, but typically carry shorter terms (5–10 years) and can have inflexible prepayment terms that make early exits costly.

Bridge Loans and Value-Add Financing

Many value-add mobile home park syndications — where the operator plans to fill vacant lots, raise rents, or improve infrastructure — use short-term bridge loans. These typically run 2–3 years with options to extend and often carry floating interest rates tied to benchmarks like SOFR.

Bridge loans are higher risk. They assume the business plan will be executed within the loan term, and they’re often refinanced into permanent agency debt once the park stabilizes. If the business plan takes longer than expected, the operator may need to extend the loan or refinance at unfavorable terms.

What Happens When a Syndication Loan Matures?

Every loan has a maturity date — the point at which the principal balance comes due in full. For passive investors in mobile home park syndications, loan maturity is one of the most consequential events in the investment timeline.

When a loan matures, the operator has a few options:

- Refinance: Replace the existing loan with a new one — ideally at favorable terms — and continue holding the asset.

- Sell the asset: Use the sale proceeds to pay off the loan and distribute profits to investors.

- Request an extension: Some lenders offer loan extensions, typically with modified terms and additional fees.

The challenge arises when a loan matures in a difficult interest rate environment, when the property hasn’t yet stabilized, or when market values have declined. In those scenarios, refinancing can be expensive or difficult — which is why passive investors should always understand the loan maturity date and the operator’s backup plan before investing.

Refinancing Risk: The Risk Passive Investors Often Overlook

Refinancing risk is the possibility that when a loan comes due, the operator cannot refinance on favorable terms — or at all. This can happen for several reasons:

- Rising interest rates: If market rates are significantly higher at maturity than when the loan was originated, the new loan payment may not be supportable by the property’s net operating income.

- Underperformance: If the property hasn’t reached projected occupancy or income levels, lenders may not approve a refinance at the same loan balance.

- Tightening credit markets: Economic downturns can make lenders more conservative, requiring larger down payments or better debt service coverage ratios.

In the worst-case scenario, refinancing risk can lead to a forced sale at an inopportune time — potentially reducing passive investor returns or resulting in a loss of capital. Understanding how your operator plans to manage this risk is not optional; it’s essential due diligence.

For more on how to evaluate an operator’s approach before investing, see our guide to mobile home park syndication red flags.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Interest Rate Risk and How Experienced Operators Manage It

Interest rate risk is closely related to refinancing risk, but distinct. Even before a loan matures, floating-rate bridge loans can see their payment obligations rise significantly if benchmark rates move higher — squeezing cash flow and potentially suspending distributions to passive investors.

Experienced mobile home park operators use several tools to mitigate interest rate risk:

- Interest rate caps: A common requirement on bridge loans, interest rate caps function like an insurance policy. If rates rise above a set ceiling, the cap pays the difference. Caps have a cost — often $50,000 to $150,000 or more — and need to be renewed if the loan is extended.

- Fixed-rate agency debt: Operators who can secure agency financing at acquisition avoid floating-rate exposure entirely.

- Conservative underwriting: Operators who underwrite deals at stressed interest rates (modeled higher than today’s rates) provide a buffer if rates rise.

Always ask whether a deal uses a floating rate loan, and if so, whether an interest rate cap is in place and how its renewal cost is budgeted. For a deeper look at how returns work in these deals, see our breakdown of what returns to expect from passive mobile home park investments.

Key Questions to Ask Your Syndicator About the Debt

Before investing in any mobile home park syndication, passive investors should ask their operator the following questions about the deal’s debt structure:

- What type of loan is being used — agency, CMBS, or bridge? Each carries different risk profiles and term lengths.

- What is the loan term, and when does it mature? Does the maturity align with the projected hold period?

- Is the interest rate fixed or floating? If floating, is an interest rate cap in place, and what happens if it needs to be renewed?

- What is the loan-to-value ratio and the debt service coverage ratio? Higher leverage means more risk; lower DSCR means less cushion if income dips.

- What is the refinancing plan at maturity? Does the operator have a lender relationship in place, and what are the assumptions around future cap rates?

- Is the loan recourse or non-recourse? Non-recourse loans limit the downside for both the sponsor and investors.

A good operator will answer these questions clearly and directly. If you get vague answers or pushback, treat it as a red flag. For more on the full GP/LP structure and how syndication economics work, see our guide to mobile home park syndication explained: GP/LP structure and return waterfalls.

How Debt Structure Affects Passive Investor Returns

At the end of the day, debt is a tool. Used well, leverage amplifies returns for passive investors — allowing a mobile home park to generate significantly higher cash-on-cash returns than an all-cash purchase would. Used poorly, it introduces risk that can turn a good deal into a painful one.

The best mobile home park operators are conservative with debt. They structure loans with terms that match or exceed their projected hold periods, use fixed rates where possible, and model stress scenarios before committing capital. Understanding their debt philosophy is one of the most revealing things you can learn during the evaluation process.

For a full overview of what passive investors should look for in a mobile home park syndication, visit our mobile home park syndication guide.

Final Thoughts

Debt structure is not a footnote in mobile home park syndication underwriting — it’s a central driver of risk and return. Passive investors who understand loan types, refinancing timelines, and interest rate risk are better equipped to evaluate deals and ask the right questions. Before you invest in any mobile home park syndication, make sure you understand exactly how the deal is financed and what happens if the environment changes.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.