The United States is short somewhere between 3.8 million and 5.5 million housing units. That gap has been widening for 15 years, driven by a combination of under-building, zoning restrictions, rising construction costs, and surging demand from a growing population that keeps household formation running ahead of supply.

Everyone in real estate knows this. What far fewer people understand is the specific role that manufactured housing communities play in this crisis — and what the current data tells us about where things are headed for operators and investors navigating this space.

The Affordability Math Doesn’t Work Without Manufactured Housing

Let’s start with the numbers that matter most.

The median new stick-built home in the United States now costs approximately $408,100. The average new manufactured home costs $109,400 — a 73% discount for comparable square footage in many markets. That gap hasn’t narrowed; it’s widened as construction costs for site-built homes have climbed roughly 9% per year for the past five years.

For a family earning the median US household income of around $78,000, a $408,100 home requires a down payment of more than $80,000 and a monthly mortgage payment that consumes 40%+ of gross income. A manufactured home on leased land can often be financed for $600–$800 per month all-in, including lot rent.

This is not a marginal difference. It is the difference between housing being accessible and housing being out of reach. And it explains why approximately 20.6 million Americans currently live in manufactured or mobile homes — roughly 6% of all housing units in the country, but a disproportionately large share of affordable housing stock.

Production Is Climbing — But Still Far Below What’s Needed

Manufactured home shipments hit 103,314 units in 2024, representing a 161% increase from the 39,574 units shipped in 2014. That’s significant growth, but it still represents a fraction of the millions of housing units the country needs.

The constraint isn’t demand. The constraint is supply — specifically, where manufactured homes can go.

There are approximately 44,000 manufactured housing communities in the United States. In 2024, roughly 20 new communities were developed — meaning the supply of land-lease communities is growing at approximately 0.04% per year. That’s not a typo. While apartment developers delivered 588,000 new units in 2024 alone, the manufactured housing community pipeline is essentially flat.

Why? Zoning. Permitting. Community opposition. The regulatory and political barriers to creating new manufactured housing communities are, in many markets, nearly insurmountable. As Frank Rolfe, one of the country’s most prolific mobile home park operators, put it in his 2026 expansion playbook: “Most denials are not about your grading plan. They are about trust, optics, and whether the city believes you will keep your promises after the vote.”

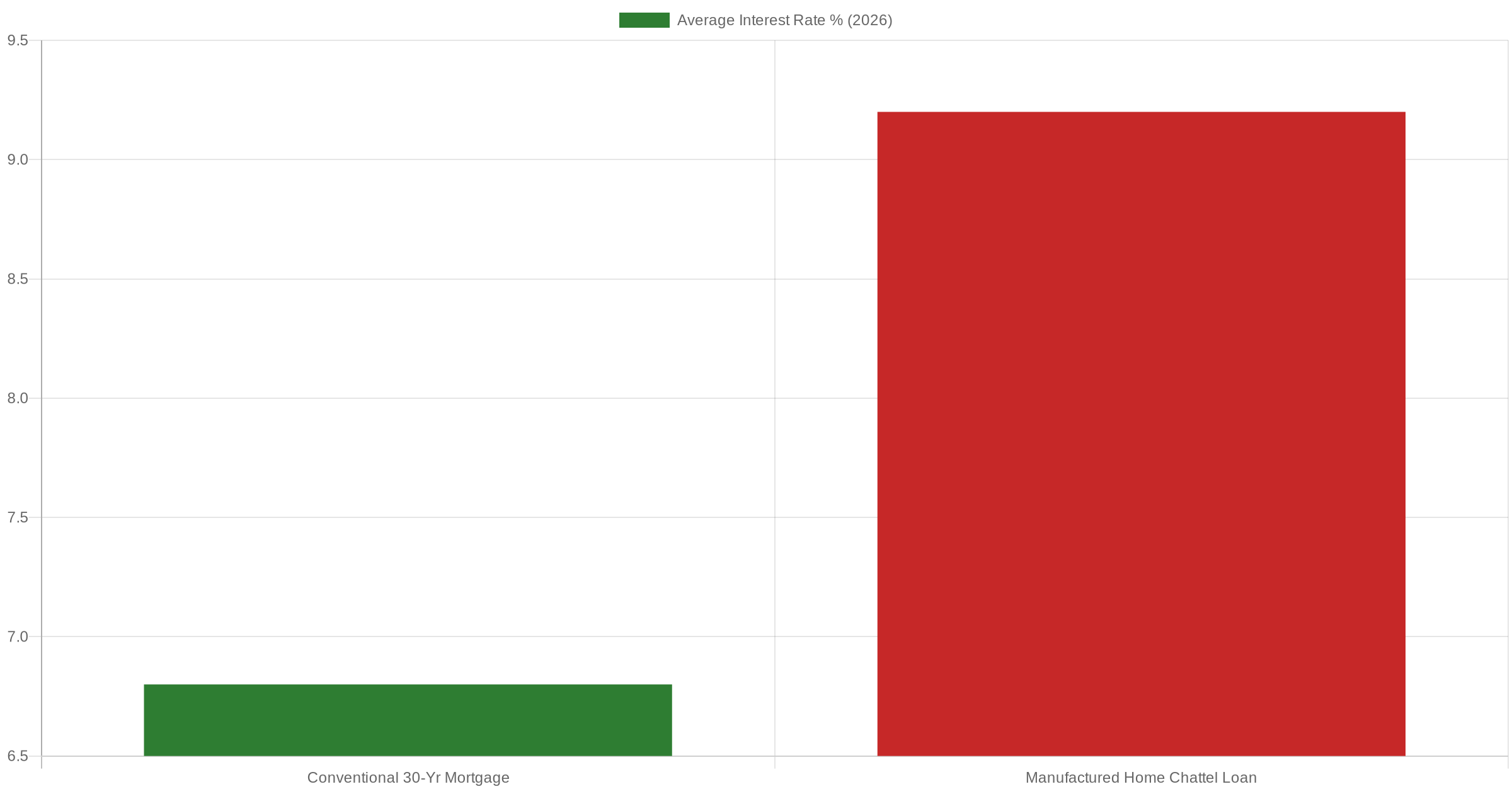

The Financing Gap Makes the Problem Worse

Even when a family wants to buy a manufactured home in an existing community, they face a financing system that hasn’t kept up with the need.

76% of new manufactured homes are titled as personal property — chattel loans, not real estate mortgages. Chattel lenders like 21st Mortgage and Triad Financial Services typically charge 7–10%+ interest versus 6–7% for conventional mortgages. And until very recently, the credit scoring models used by lenders entirely ignored rental payment history — meaning a renter who had reliably paid $750/month for five years got zero credit for that track record.

The April 22, 2026 FHFA announcement expanding credit scoring to include VantageScore and FICO 10T — models that count rental and utility payment history — is a meaningful step forward. But it applies primarily to conventionally financed homes, not chattel. The chattel lending gap remains one of the core structural problems keeping manufactured housing residents from the wealth-building that comes with homeownership. (We covered this in detail in our recent post on the FHFA credit scoring changes.)

What This Means for Mobile Home Park Operators

Here’s where the data gets operationally relevant.

National occupancy across manufactured housing communities reached approximately 94% in 2025, up from 86.5% a decade earlier. Average lot rent nationally is around $752/month, up 7% year-over-year. In premium markets — Florida, Arizona, Colorado — lot rent growth has been running 9–12% annually.

These numbers reflect the supply-demand imbalance playing out in real time. When you can’t build new communities, existing communities fill up and pricing power increases. That’s the moat that makes the asset class attractive.

But the same supply constraint creates a serious problem for operators trying to grow occupancy in parks that have vacant lots. You can’t just snap your fingers and fill a vacant lot. The home supply chain — dealers, transport crews, used home inventory, financing programs — is fragmented and under-resourced. (We go deep on this in our complete lot infill strategy guide.)

The affordable housing crisis is simultaneously what makes mobile home park investing compelling and what makes operating one hard. There is enormous demand. There is limited supply. But getting demand connected to supply — qualified residents into available lots with workable financing — requires active, systematic effort that most operators aren’t doing well.

📋 The MHP Due Diligence Playbook

Before you buy a mobile home park, make sure you’re evaluating it correctly. The MHP Due Diligence Playbook gives you 10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of analyzing a deal — from occupancy verification to utility infrastructure review to financing structure.

Where the Industry Is Heading: The Data Says Optimism Is Warranted

A few data points from 2026 suggest the industry is moving in the right direction, even if slowly.

Institutional interest is growing fast. A national commercial mortgage broker reports a 170% increase in manufactured housing transaction volume over the past five years compared to the prior five. Lenders who once wouldn’t touch chattel paper are now building dedicated teams to originate it.

Industry participation is at record levels. The Manufactured Housing Institute’s Congress & Expo in Las Vegas in April 2026 drew 1,500+ professionals — a 59% increase from 2019 attendance. That’s not the footprint of a dying or marginal asset class. That’s an industry finding its footing as a legitimate, institutional-grade sector.

Federal policy is moving toward manufactured housing, not away from it. The April 2026 FHFA credit score expansion, combined with HUD Secretary Turner’s public prioritization of manufactured housing affordability, signals that the political environment is increasingly favorable to regulatory reform in this space.

The demographic math is inescapable. The millennial generation — now mostly in their 30s — is hitting peak household formation age. They’re priced out of the entry-level stick-built market. They have student debt. They are the natural demand driver for affordable manufactured housing, and their numbers are massive.

The Honest Operator’s Take

Running mobile home park communities in a housing crisis is not a comfortable thing to write about from a purely financial perspective. The people living in these communities are there because housing costs have put everything else out of reach. That creates a real responsibility for operators.

The way we see it at Keel Team: the best thing we can do for residents is run communities that are clean, well-maintained, properly managed, and financially sustainable. That means investing in infrastructure, staying current on utility compliance, maintaining homes properly, and treating residents as long-term community members rather than month-to-month revenue sources.

The operators who approach manufactured housing with this mindset tend to have higher occupancy, lower turnover, fewer regulatory headaches, and better community reputations — which translates directly to the ability to fill lots, retain residents, and grow asset value over time.

The operators who treat it as a raw cash-extraction business are the ones generating the regulatory backlash — the tenant protection laws, right-of-first-refusal legislation, and local government scrutiny — that the entire industry is now navigating. See our recent breakdown of the North Carolina Mobile Home Park Act (SB 518) for a concrete example of how operator behavior drives regulatory response.

What Operators and Investors Should Take From This

A few practical implications from the data:

- Location selection still matters above everything else. The communities that will benefit most from the affordability crisis are those within commuting distance of employment centers — specifically, within one hour of a metro area with 100,000+ population. Rural parks in markets without jobs don’t benefit from housing demand pressure the same way.

- Lot fill is the lever. National occupancy at 94% doesn’t mean your park is at 94%. If it’s at 75%, you’re leaving serious money on the table and you need a systematic approach to fixing it. The demand is there; the pipeline to connect residents to lots is what’s broken.

- Infrastructure quality is becoming a differentiator. As institutional capital enters the space and regulatory scrutiny increases, parks with city water, city sewer, and maintained roads attract both better residents and better acquisition bids. Parks with well/septic are increasingly priced for their problems, not just their income.

- The financing landscape is shifting. The April 2026 credit scoring changes, growing chattel lender competition, and increasing Fannie/Freddie engagement with manufactured housing all point toward better resident financing options in the next 3–5 years. Underwrite conservatively today; the tailwind is real.

The affordable housing crisis is not going away. Mobile home parks sit at the intersection of the problem and the solution — communities that provide critical housing stock, operating within a market structure that rewards disciplined, long-term-oriented operators. Understanding the macro data isn’t just intellectual exercise. It’s the foundation for making better investment and operating decisions.

📋 Ready to Evaluate Your Next Deal?

Get the MHP Due Diligence Playbook — the complete system for analyzing mobile home park acquisitions with confidence. 10 video modules, a 55-page master checklist, and 9 deal-ready templates. Built from real deals, not textbook theory.

Frequently Asked Questions

How many people live in manufactured housing communities in the US?

Approximately 20.6 million Americans live in manufactured or mobile homes — roughly 6% of all housing units. Manufactured housing communities are the single largest source of unsubsidized affordable housing in the country.

Why aren’t more manufactured housing communities being built?

Zoning and permitting barriers are the primary obstacle. Many municipalities zone against manufactured housing, and new community development frequently faces intense community opposition. In 2024, only approximately 20 new manufactured housing communities were developed nationwide — roughly 0.04% of the total stock of 44,000 communities.

What is a chattel loan and why does it matter for mobile home park operators?

A chattel loan is a personal property loan used to finance manufactured homes that are not permanently affixed to real estate. 76% of new manufactured homes are financed this way. Chattel loans carry higher interest rates (7–10%+) than conventional mortgages, which affects resident affordability and limits the pool of qualified buyers. This directly impacts a park operator’s ability to fill vacant lots.

What is the current national occupancy rate for manufactured housing communities?

National occupancy for manufactured housing communities was approximately 94% as of 2025, up from 86.5% a decade earlier. This reflects the tight supply of available lots relative to demand for affordable housing.

How does the affordable housing crisis affect mobile home park valuations?

The housing shortage increases the demand for affordable rental alternatives, including mobile home park lot rent. Higher occupancy and stronger lot rent growth support higher net operating income, which drives asset values up. Parks in supply-constrained markets near strong employment centers have seen cap rate compression to 5–7% for stabilized assets and 4–5% for institutional-quality communities.