If you’re exploring passive real estate investing, you’ve likely come across two primary structures for getting exposure to mobile home park investments: syndications and funds. Both allow you to invest as a limited partner without managing anything yourself — but they work very differently, carry different risk profiles, and suit different investor goals.

This guide breaks down exactly what each structure is, how they compare on key metrics, and how to decide which one fits your situation.

What Is a Mobile Home Park Syndication?

A mobile home park syndication is a deal-by-deal private investment structure. A general partner (GP) — typically an experienced operator — identifies a specific mobile home park, assembles a group of limited partners (LPs) to provide equity capital, closes on the property, operates it, and eventually sells it. Investors in the syndication own a fractional interest in that one property.

The syndication has a defined timeline: typically 3-7 years from acquisition to exit. During that hold period, limited partners receive periodic distributions (usually quarterly) generated from lot rent income. At exit, proceeds from the sale are distributed according to a waterfall structure — first returning capital, then paying preferred returns, then splitting remaining profits between the GP and LPs.

For a deeper look at how these structures work, read our guide: Mobile Home Park Syndication Explained: GP/LP Structure, Return Waterfalls, and What Passive Investors Need to Know.

What Is a Mobile Home Park Fund?

A mobile home park fund is a pooled investment vehicle that deploys capital across multiple properties over time. Instead of investing in one specific mobile home park, your capital goes into a blind pool or an assembling portfolio of mobile home parks. The fund manager makes acquisition decisions on your behalf based on a stated investment strategy.

Funds come in two primary forms:

- Blind pool funds: Capital is raised before properties are identified. Investors commit based on the manager’s track record and strategy, not a specific asset.

- Specified asset funds: Some properties are already identified at launch, giving investors partial visibility into what they’re buying into before fully committing.

Funds typically have a longer investment horizon (5-10 years) and deploy capital over a 1-3 year period. Because capital is spread across multiple mobile home parks, a single underperforming asset has less impact on overall portfolio returns.

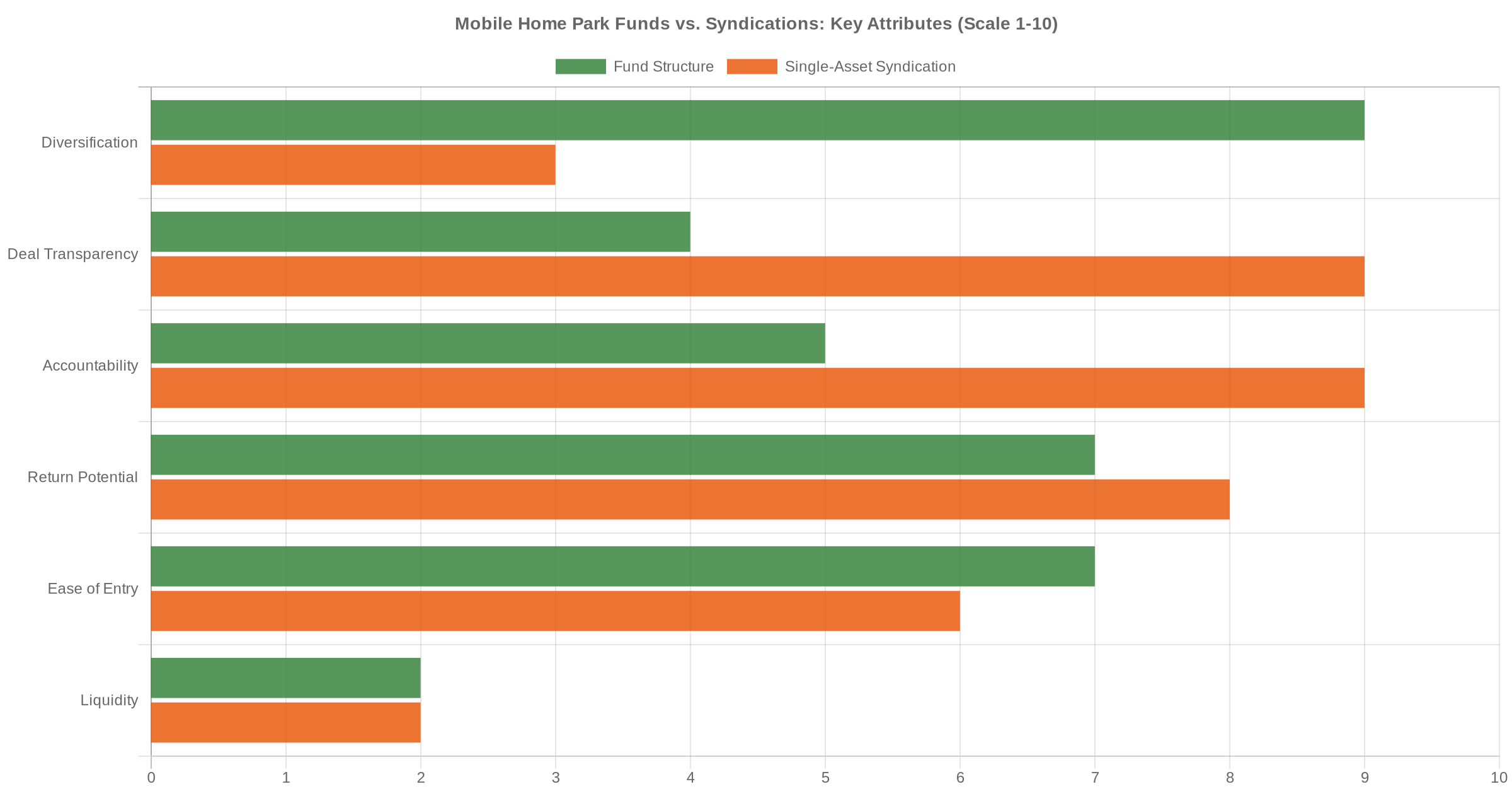

Side-by-Side Comparison: Key Differences

Here’s how mobile home park funds and syndications compare across the dimensions that matter most to passive investors:

| Attribute | Syndication | Fund |

|---|---|---|

| Number of Properties | 1 (single asset) | Multiple (5–20+ parks) |

| Deal Transparency | High — review the specific property | Low — blind pool structure |

| Typical Hold Period | 3–7 years | 5–10 years |

| Minimum Investment | $25,000–$100,000 | $50,000–$250,000+ |

| Diversification | Concentrated (1 property) | Diversified (multiple markets) |

| Manager Accountability | High — clear single-asset performance | Moderate — blended across portfolio |

| Liquidity | Very low (illiquid) | Very low (illiquid) |

Pros and Cons of Mobile Home Park Syndications

Advantages of Syndications

- Full visibility into the deal: You can review the specific property’s financials, location, occupancy history, and business plan before committing capital. You know exactly what you’re buying.

- Shorter time horizon: Syndications often have 3-5 year holds, which means you get your capital back faster than a typical fund structure.

- Direct accountability: If the property underperforms, it’s immediately apparent. The GP’s compensation is directly tied to the performance of that single asset.

- Lower minimums: Many syndications accept investments starting at $25,000–$50,000, making them accessible to a wider range of accredited investors.

Disadvantages of Syndications

- Concentrated risk: If that one mobile home park has a significant issue — a major capital expenditure surprise, a local market downturn, or management problems — it directly impacts your returns with no cushion from other assets.

- Timing dependency: Your returns depend heavily on when the property was acquired and when it exits. A deal that closes at the wrong point in the market cycle can compress returns significantly.

- Ongoing due diligence burden: Each new deal requires a fresh evaluation. Active syndication investors may review dozens of deals per year to deploy capital consistently.

Pros and Cons of Mobile Home Park Funds

Advantages of Funds

- Built-in diversification: Spreading capital across 5–20+ mobile home parks in multiple states significantly reduces single-asset risk. One underperforming park won’t tank the portfolio.

- Hands-off by design: Once you’re in the fund, you don’t evaluate individual deals. This suits passive investors who want true passivity with minimal ongoing involvement.

- Geographic diversification: Funds often operate across multiple markets, reducing exposure to any single state’s regulatory environment or economic conditions.

- Vintage year averaging: Deploying capital over time across multiple acquisition years averages out market timing risk — a key advantage in uncertain market conditions.

Disadvantages of Funds

- Less transparency: In a blind pool structure, you’re investing in the manager’s judgment, not a specific asset. If you want to know exactly what property your capital is in, a fund won’t satisfy that need.

- Higher minimums: Fund structures typically require $100,000–$250,000+ minimum investments, limiting access for newer or smaller investors.

- Longer capital commitment: Capital is locked up for 7–10 years in many fund structures — significantly longer than most single-asset syndications.

- Fee layering risk: Some funds include both fund-level and property-level fees, which can erode net returns compared to a lean single-asset syndication.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Which Structure Delivers Better Returns?

This is the question every passive investor asks — and the honest answer is: it depends on the manager, the vintage, and the specific deals.

That said, some general patterns hold across the industry:

- Top-quartile syndications tend to outperform top-quartile funds because concentration allows the GP to optimize one deal rather than average results across a portfolio. A skilled operator with a compelling value-add thesis and a strong market can generate 15–20%+ IRRs on a single deal.

- Median funds tend to outperform median syndications because diversification smooths out single-deal blowups. A poorly executed syndication can produce negative returns; a diversified fund rarely does.

- Both structures typically target 7–12% preferred returns for limited partners, with total IRR targets in the 12–18% range depending on strategy and leverage.

For investors focused on downside protection, funds may offer more peace of mind. For investors who can do thorough due diligence and want maximum transparency, syndications offer a cleaner, more accountable structure where you know exactly how your capital is performing.

How to Choose Between a Fund and a Syndication

The right structure depends on your goals, experience level, and how involved you want to be in the investment decision process.

Consider a mobile home park syndication if:

- You want to review the specific property before investing

- You’re comfortable analyzing a deal or working with a trusted operator you know well

- You prefer shorter hold periods and faster capital recycling

- You’re starting with $25,000–$75,000 to deploy

- You want direct accountability — your returns reflect that one deal’s performance

Consider a mobile home park fund if:

- You want maximum diversification and don’t want to evaluate individual deals

- You have $100,000+ to deploy and want to keep it simple

- You’re comfortable with a longer investment horizon (7–10 years)

- You’re newer to mobile home park investing and want broader exposure before going deep on a single deal

Many experienced passive investors use both structures simultaneously — building a diversified portfolio that includes one or two syndications for concentrated upside alongside a fund for stable, diversified cash flow. This approach combines the best of both worlds: transparency and concentration in deals you’ve vetted thoroughly, plus diversification and passivity through a fund.

For a deeper look at evaluating operators before committing capital, read: Mobile Home Park Passive Investment Due Diligence: What Every LP Must Review Before Writing a Check.

Red Flags to Watch for in Both Structures

Whether you’re evaluating a fund or a syndication, certain warning signs apply across the board:

- Unrealistic return projections: If projected IRRs are consistently above 20% without a clear value-add thesis and supporting underwriting, ask hard questions.

- Excessive fee layers: Watch for acquisition fees above 3%, asset management fees above 2%, or disposition fees above 2%. These compound over a 5-7 year hold and can meaningfully erode LP returns.

- No track record of full-cycle deals: Anyone can show you projections. Ask for actual closed deals with documented LP returns. If the GP has never exited a deal, you’re taking significantly more risk.

- Vague market selection criteria: The best operators have specific, defensible reasons for buying in certain markets. “We look for opportunities nationwide” is a yellow flag.

- Poor communication during the hold: Quarterly investor updates should be substantive — occupancy trends, capital expenditure updates, distribution schedules. Silence after closing is not a good sign.

For a complete list, see our post on Mobile Home Park Syndication Red Flags: 7 Warning Signs Before You Invest.

Frequently Asked Questions

What is the minimum investment for a mobile home park fund?

Most mobile home park funds require minimum investments of $100,000 to $250,000, though some emerging managers accept $50,000. Single-asset syndications often have lower minimums starting at $25,000–$50,000, making them more accessible for first-time passive investors looking to get started in the asset class.

Are mobile home park funds regulated differently than syndications?

Both structures typically rely on Regulation D exemptions under SEC rules. Syndications commonly use 506(b) or 506(c) exemptions, while funds may use the same or similar structures. In either case, only accredited investors (or sophisticated investors under some 506(b) offerings) may participate. Always review the Private Placement Memorandum carefully with a qualified securities attorney before making any investment decision.

Can I invest in both a mobile home park fund and a syndication at the same time?

Yes — and many experienced passive investors do exactly that. Pairing a fund’s diversification with the targeted upside potential of a well-underwritten syndication is a sound portfolio construction strategy, provided you understand the illiquidity of both positions and have appropriate capital reserves outside of these investments.

How do preferred returns work in a mobile home park fund?

Most mobile home park funds offer a preferred return — commonly 7–9% annually — that must be paid to limited partners before the general partner receives any profit participation. This preferred return typically accumulates during the hold period and is paid out from cash flow distributions or at exit. For a full explanation, read our guide on What Is a Preferred Return in Real Estate Syndication?

Which structure is more tax-efficient for passive investors?

Both mobile home park funds and syndications can pass through depreciation benefits — including bonus depreciation from cost segregation studies — to limited partners. The specific tax treatment depends on the deal structure, the amount of leverage used, and whether the manager conducts a cost segregation study. In both cases, passive losses from depreciation may offset passive income, subject to IRS passive activity loss rules. Always consult a tax advisor familiar with real estate syndications before investing.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

The Bottom Line

Neither mobile home park funds nor syndications are universally superior — they’re different tools built for different investor profiles. Syndications give you transparency, direct accountability, and shorter timelines at the cost of concentration. Funds give you diversification and simplicity at the cost of visibility and longer lock-ups.

The most important factor in either structure isn’t the vehicle itself — it’s the operator. A mediocre fund manager with poor market selection and bloated fees will underperform a disciplined, experienced syndicator every time, regardless of structure. Do your diligence on the person, not just the paperwork.

Get the top 20 lessons from two decades of mobile home park investing — free.