If you’re exploring ways to put your retirement savings to work in real assets, self-directed IRA mobile home park investing deserves a serious look. A self-directed IRA (SDIRA) allows you to hold alternative investments — including real estate syndications — inside a tax-advantaged retirement account. For passive investors who want exposure to mobile home parks without active management, this combination can be remarkably powerful.

This guide breaks down exactly how SDIRAs work, the rules you need to follow, and why mobile home parks have become one of the most popular real estate asset classes for SDIRA investors.

What Is a Self-Directed IRA?

A self-directed IRA is a type of individual retirement account that gives you control over what you invest in — beyond the stocks, bonds, and mutual funds offered by traditional custodians like Fidelity or Vanguard.

With a self-directed IRA, eligible investments can include:

- Real estate (direct ownership or syndications)

- Promissory notes and private lending

- Private equity and LLC interests

- Tax liens and deeds

- Precious metals

The key distinction: your SDIRA must be held by a qualified custodian — a financial institution that specializes in alternative assets (e.g., Equity Trust, Alto IRA, Directed IRA, or Millennium Trust). Your traditional broker won’t handle this.

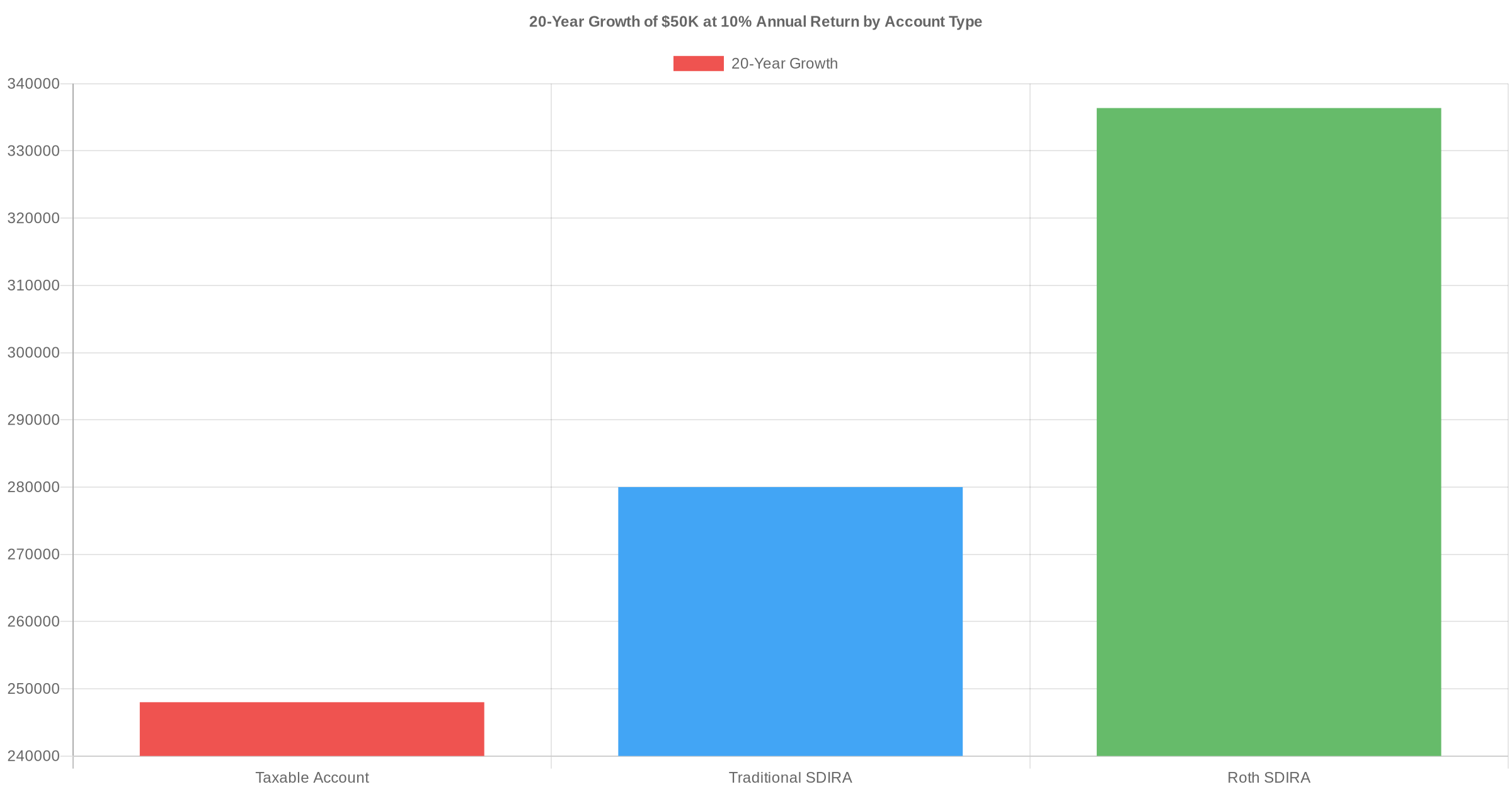

Traditional SDIRA vs. Roth SDIRA: Which Is Better for Mobile Home Park Investing?

You can use either a traditional or Roth IRA in self-directed form. The difference comes down to when you pay taxes:

Traditional SDIRA

- Contributions may be tax-deductible (income limits apply)

- Growth is tax-deferred — you pay ordinary income tax on withdrawals

- Required minimum distributions (RMDs) begin at age 73

- Best for investors who expect to be in a lower tax bracket at retirement

Roth SDIRA

- Contributions are made with after-tax dollars

- All growth and qualified withdrawals are completely tax-free

- No RMDs during the account holder’s lifetime

- Best for investors who expect tax rates to rise or want to pass wealth to heirs

For most mobile home park syndication investors with a long time horizon, the Roth SDIRA is the more compelling vehicle. The distributions, appreciation, and eventual exit proceeds all flow back into the Roth account — entirely tax-free.

How to Invest in a Mobile Home Park Syndication Through an SDIRA

The mechanics are straightforward once you’ve set up the account. Here’s the typical process:

Step 1: Open a Self-Directed IRA

Choose a custodian that specializes in alternative investments. Account setup typically takes one to two weeks and may involve a small annual fee. Roll over funds from an existing IRA or 401(k), or make new contributions up to the annual limit ($7,000 in 2026; $8,000 if you’re 50+).

Step 2: Fund the Account

Once the SDIRA is open, transfer or roll over funds. Direct rollovers from a 401(k) or traditional IRA avoid triggering taxes or penalties. Your custodian will handle the paperwork.

Step 3: Identify a Mobile Home Park Syndication

Work with a sponsor you’ve vetted. Under Regulation D 506(b) syndications, you typically need a pre-existing relationship with the sponsor and may need to be an accredited investor. Learn more about evaluating mobile home park operators in our guide to vetting operators.

Step 4: Direct Your Custodian to Invest

You don’t write a personal check. Your SDIRA custodian signs the subscription agreement and wires the funds on behalf of your account. The investment is titled in the name of your IRA (e.g., “Equity Trust Company FBO John Smith IRA”).

Step 5: Receive Distributions Back to Your SDIRA

All distributions — quarterly cash flow, refinance proceeds, and eventual sale proceeds — flow back into your SDIRA, not your personal bank account. This keeps the tax benefits intact.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

SDIRA Rules You Must Not Violate

The IRS places strict rules on SDIRAs. Violations can result in the entire account being treated as distributed — triggering immediate taxes and penalties. The most important rules:

Prohibited Transactions

You cannot do business with disqualified persons — which includes yourself, your spouse, lineal descendants, and certain businesses you control. This means your SDIRA cannot invest in a mobile home park syndication where you are personally a general partner or co-owner.

No Self-Dealing

Your IRA cannot benefit you personally outside of its designated retirement purpose. You can’t use property owned by your IRA, receive personal compensation, or guarantee loans with your personal assets.

Unrelated Business Income Tax (UBIT)

If a syndication uses debt financing (which most do), your SDIRA may owe Unrelated Business Income Tax (UBIT) on the leveraged portion of income. This is an important consideration — consult a tax professional familiar with SDIRAs before investing in leveraged deals. Roth SDIRAs are not exempt from UBIT.

Arm’s-Length Transactions

All SDIRA investments must be at fair market value with independent parties. The IRS scrutinizes related-party transactions closely.

Why Mobile Home Parks Are a Natural Fit for SDIRAs

Mobile home parks offer several characteristics that make them particularly well-suited for SDIRA investment:

- Passive income: Syndication distributions require no active involvement from the investor — ideal for an IRA where you can’t “work” for the asset.

- Recession resilience: Manufactured housing has historically maintained strong occupancy during downturns, which reduces the risk of extended periods without distributions.

- Long hold periods: Typical mobile home park syndications hold for five to seven years — well-matched to a retirement account’s long-term horizon.

- Limited supply: New mobile home park development is rare due to zoning restrictions, creating supply constraints that support valuations.

To understand how passive mobile home park investments are structured and what returns to expect, see our guide on passive investing in mobile home parks.

SDIRA Mobile Home Park Investing: Key Takeaways

- A self-directed IRA lets you invest retirement dollars into mobile home park syndications

- Roth SDIRAs offer tax-free growth and withdrawals — a major long-term advantage

- All transactions must go through a qualified SDIRA custodian

- Avoid prohibited transactions with disqualified persons

- Leveraged deals may trigger UBIT — consult a tax advisor

- Distributions flow back to your IRA, preserving the tax shelter

If you’re thinking about adding mobile home park exposure to your retirement portfolio, the SDIRA route is worth exploring carefully. Start by reviewing the differences between active and passive mobile home park investing to make sure passive syndication aligns with your goals.

And if you’d like to learn more about mobile home park investing from an educational standpoint, reach out and we’re happy to set up a call.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.