If you’ve owned a mobile home park for more than three years, you remember when property insurance was a line item you thought about once a year and mostly ignored. Renew. Pay. Move on.

That era is over.

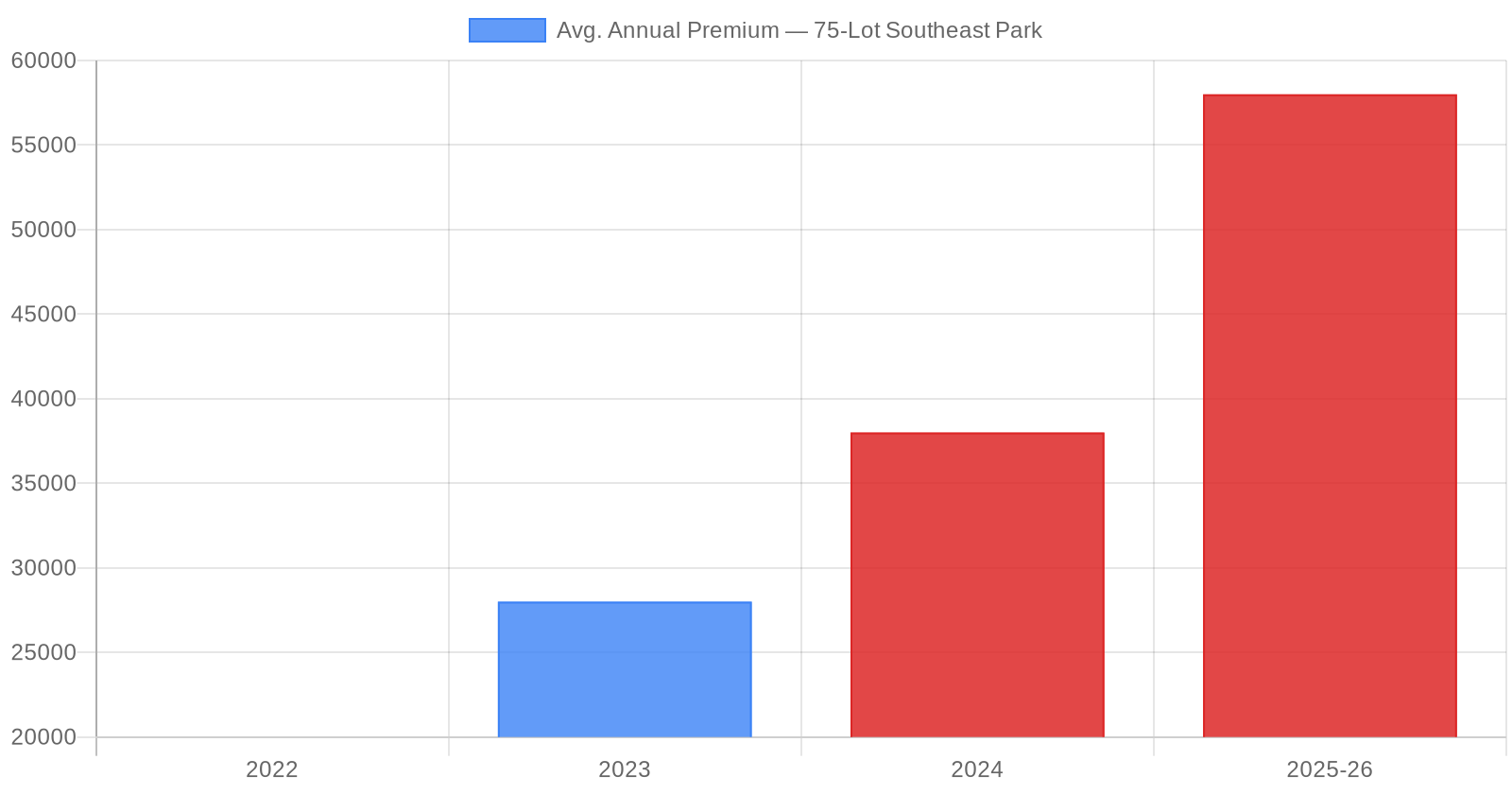

I’ve been operating manufactured housing communities across the Southeast for years, and what I’m seeing in the insurance market right now is genuinely alarming. Parks that were insured for $20,000 a year are getting renewals at $55,000. Carriers that wrote mobile home park policies without blinking are now sending non-renewal letters. Deals that penciled out beautifully at underwriting are blowing up at closing because the insurance quote comes in three times higher than projected.

This isn’t a regional blip. It’s a structural shift — and if you’re not actively managing it, it’s going to quietly destroy your returns.

Why Is This Happening?

The mobile home park insurance crisis is the collision of several forces:

Catastrophic loss events. Hurricane Helene and back-to-back storm seasons across the Carolinas, Georgia, and Tennessee have hit manufactured housing communities hard. Insurers absorbed massive losses and responded the only way they know how: repricing the entire category.

Reinsurance cost pass-through. The global reinsurance market — the insurance that insurance companies buy — has gotten significantly more expensive. Those costs flow downstream directly to property owners.

Carrier pullbacks. Many A-rated admitted carriers have quietly exited Southeast mobile home park coverage entirely. When you lose admitted market options, you get pushed into surplus lines — which costs more, has worse terms, and sometimes doesn’t satisfy lender requirements.

Aging housing stock. The average manufactured home in a community is 20–30 years old. Insurers are pricing that age-related risk more aggressively than ever.

What This Means for Deal Underwriting

Here’s the number that should scare you: the difference between $25,000/year and $65,000/year in insurance on a 75-lot park is $40,000. At a 7-cap, that’s $571,000 of value. Gone.

If you’re underwriting deals and using the seller’s current insurance costs as your baseline, you’re potentially setting yourself up for a painful surprise. I’ve seen deals close, insurance renew 90 days later at 2× the cost, and the entire business plan collapse.

Due diligence now requires getting actual insurance quotes — not estimates — before you close. Call 3–4 brokers who specialize in manufactured housing. Ask specifically for admitted carrier options vs. surplus lines. Understand your wind/hail deductible structure. If a park in North Carolina or Tennessee is being insured for under $500/lot/year, that number warrants a hard look. (Our Mobile Home Park Due Diligence Playbook includes an insurance review checklist that walks through exactly what to request from brokers before you close.)

What Smart Operators Are Doing Right Now

1. Diversifying broker relationships. Don’t have one insurance agent. Have three, and make sure at least one specializes in manufactured housing. Brokers with mobile home park-specific books of business have access to programs the generalists don’t.

2. Requiring tenant home policies. Almost every mobile home park lease includes a clause requiring residents to carry their own homeowner or renter policy. Most parks aren’t enforcing it. When tenants carry HO-7 policies — with the park named as additional insured — it reduces the park’s risk profile and can shave 15–25% off the master policy premium. Start enforcing it.

3. Documenting risk improvement. Underwriters reward documented risk management. Replace electrical panels on park-owned homes. Install hurricane tie-downs on older units. Create a formal maintenance log for infrastructure. Send that documentation to your broker. Carriers have offered meaningful premium discounts in exchange for a simple 20-page risk improvement plan.

4. Building broker relationships before you need them. The worst time to find an insurance broker is 30 days before your policy expires. Get connected now with 2–3 manufactured housing-specialized brokers, even if you’re not shopping coverage immediately. When you need them, they’ll already know your portfolio.

5. Pricing insurance correctly in acquisition models. We use $750–$1,200/lot/year as our current benchmark for Southeast mobile home park insurance — higher for coastal/storm exposure, lower for inland markets with newer homes. That range may feel aggressive compared to what a seller is paying today, but it’s closer to what reality looks like at renewal.

The Bigger Picture

Insurance is one of those “boring” problems that doesn’t get attention until it blows something up. The mobile home park operators who will come out ahead in the next 3–5 years are the ones who treat insurance as a strategic asset management issue, not a commodity to renew and forget.

The good news: this is a solvable problem. It requires more attention and better broker relationships than most operators currently invest. But operators who get ahead of it will have a meaningful cost advantage over those who don’t.

If you want to talk through what we’re seeing in insurance markets for Southeast manufactured housing communities, feel free to reach out. This is something our team at Keel Team tracks closely, and we’re happy to share what we’re learning.

Andrew Keel is the founder of Keel Team, a mobile home park investment and operating company focused on manufactured housing communities across the Southeast.