In 2026, passive investors face a familiar but increasingly urgent question: with stock market volatility, elevated valuations, and ongoing macroeconomic uncertainty, is there a better home for long-term capital than a brokerage account?

For a growing number of accredited investors, mobile home park investing has become a compelling answer. But comparing it to the stock market requires nuance — these are fundamentally different asset types, with different risk profiles, liquidity characteristics, and tax implications.

This post breaks down both asset classes honestly, so you can decide whether they have a place in your portfolio — separately or together.

The Case for Stocks: Why They Are Still the Default

The stock market has delivered remarkable long-term returns. The S&P 500 has averaged roughly 10-11% annually over the past century. For most investors, it is the default vehicle for good reason: accessible, highly liquid, low-cost via index funds, and requires almost no ongoing management time.

Tax-advantaged wrappers like IRAs and 401(k)s make stocks even more attractive, and diversification across thousands of companies is available with a single fund.

The downside? Volatility is real and often severe. The S&P 500 dropped more than 19% in 2022. It lost over 50% during the 2008-2009 financial crisis. For investors who need predictable cash flow or who are approaching retirement, that kind of drawdown is difficult to absorb.

Stocks are also tightly correlated to macroeconomic sentiment and Federal Reserve policy — forces largely outside any individual investor’s control. When markets sell off, they often sell off across all sectors simultaneously, limiting real diversification.

What Mobile Home Park Investing Offers Passive Investors

Mobile home park investing — particularly as a passive limited partner in a professionally managed syndication — offers a different set of characteristics entirely.

Here is what makes it attractive to passive investors:

- Stable, demand-driven income: Mobile home parks serve the largest underserved segment of the housing market — residents who need affordable, non-subsidized housing. Demand is structural and persistent, not driven by economic cycles or sentiment.

- Exceptionally low tenant turnover: Residents own their homes and rent the land beneath them. Moving a manufactured home typically costs $5,000-$10,000 or more. Mobile home park tenant turnover runs around 2-5% annually, compared to 40-60% for apartments. Low turnover means predictable occupancy and income.

- Supply constraints: New mobile home parks are nearly impossible to permit in most jurisdictions. That fixed supply, combined with growing affordable housing demand, creates durable pricing power for existing park owners.

- Recession resilience: During the 2008-2009 downturn, mobile home parks largely held their occupancy while other commercial real estate asset classes suffered. Affordable housing demand does not disappear in recessions — it often increases.

As a passive investor in a mobile home park syndication, you are not managing any of this yourself. The operator handles acquisitions, property management, capital improvements, and eventual disposition. You receive distributions and benefit from any appreciation at exit.

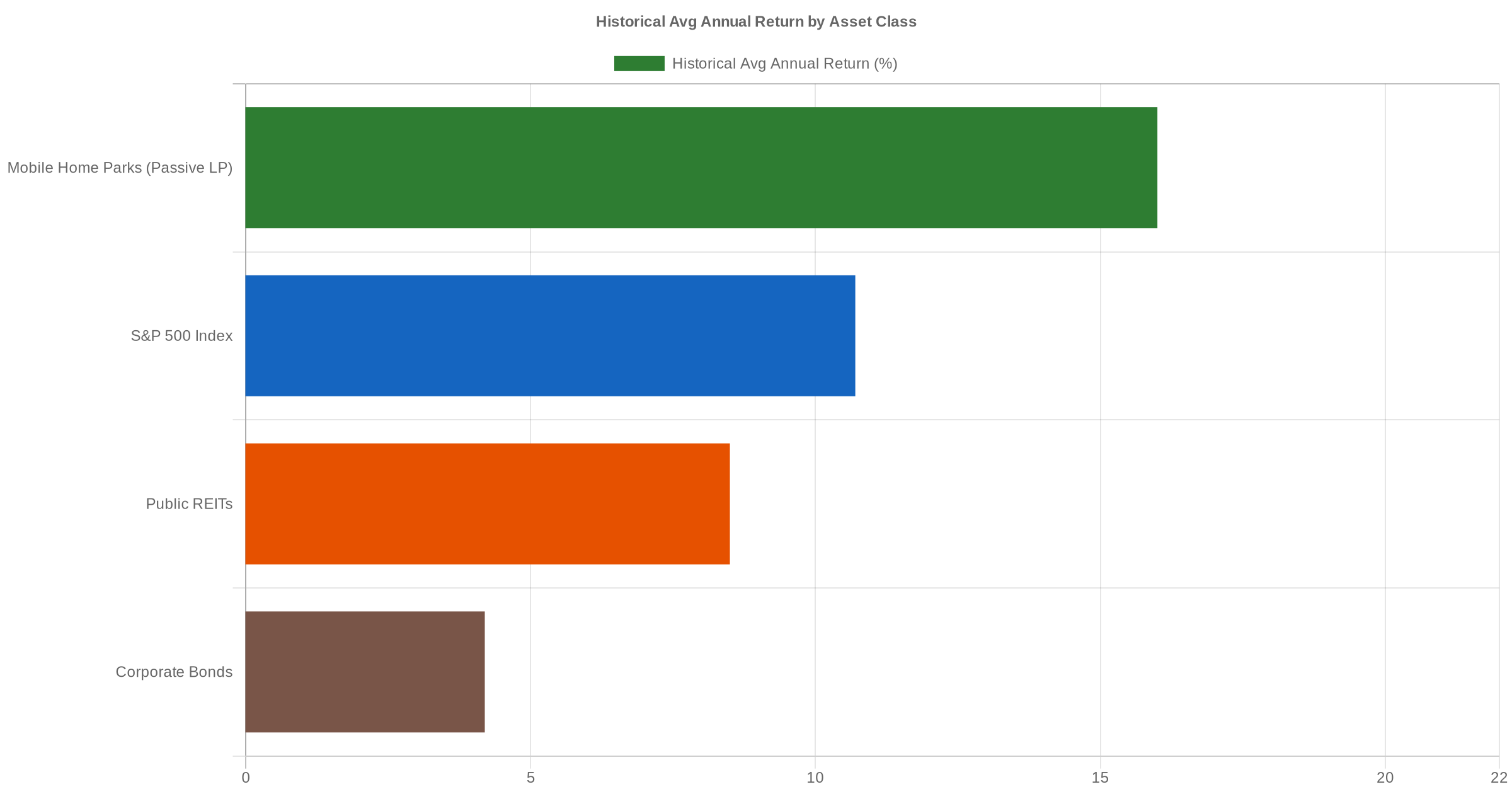

Returns Comparison: What the Data Shows

Comparing returns across asset classes requires some nuance, but here is a reasonable framework based on historical data:

- S&P 500 (index funds): Approximately 10-11% average annual return over the long term, with significant year-to-year volatility

- Public REITs: Approximately 8-10% average annual total return (dividends plus appreciation), with volatility similar to stocks

- Corporate bonds: Approximately 4-5% in the current rate environment, with lower risk and lower upside

- Mobile home park syndications (passive LP): Operators typically target 14-18% IRR on well-underwritten deals, including cash-on-cash distributions of 6-10% annually plus back-end equity at exit

These figures reflect well-executed deals by experienced operators — they are not guaranteed, and operator quality matters enormously. But mobile home parks have consistently ranked among the best-performing commercial real estate asset classes over the past two decades, driven by the supply/demand fundamentals described above.

Perhaps equally important: mobile home park returns are largely uncorrelated to stock market performance. When the S&P 500 dropped 19% in 2022, well-run mobile home parks continued generating lot rent and distributing cash to investors. That decorrelation is one of the most valuable characteristics of the asset class.

Two decades of hard-won lessons distilled into one free guide. Whether you are evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Volatility and Risk Profile: A Different Kind of Risk

Stock market investments are marked to market daily. If you log into your brokerage on a bad day, you see real losses in real time. The psychological pressure of watching your portfolio fluctuate is underestimated by most investors until they have lived through a significant drawdown. Many sell at exactly the wrong moment.

Mobile home park syndications are private, illiquid investments. There is no ticker price updated daily. The value of your investment is not marked to market — it is realized over a 3-7 year hold period when the property is refinanced or sold. This illiquidity can feel like a disadvantage, but it also removes the temptation to panic-sell during market turbulence.

That said, mobile home park investments carry their own distinct risks:

- Operator execution risk: The deal is only as good as the team running it. A bad operator can underperform even in a favorable market.

- Capital lock-up: You generally cannot exit before the hold period ends without significant friction.

- Financing risk: Interest rate changes affect refinancing timelines and exit valuations.

- Market-specific risks: Local economic conditions, regulatory changes, and infrastructure issues can affect specific deals.

For passive investors, mitigating these risks comes down to diligent vetting of operators before committing capital — reviewing track records, past deals, communication practices, and deal structure carefully. Our passive investing guide walks through exactly what to look for.

Tax Efficiency: Where Real Estate Has a Clear Edge

For high-income investors, this is often the most compelling argument for mobile home park investing over stocks.

Real estate — and mobile home park investments specifically — offer several tax advantages that public markets cannot match:

- Depreciation: The IRS allows investors to depreciate real estate improvements over time, generating paper losses that can offset passive income. Many mobile home park deals use cost segregation to accelerate this depreciation, producing significant paper losses in early years of ownership.

- Pass-through losses: As a limited partner in a syndication, you receive a K-1 each year that may reflect depreciation-driven losses, potentially sheltering other passive income from tax.

- 1031 exchange potential: Proceeds from a property sale can often be rolled into another real estate investment on a tax-deferred basis under Section 1031 — a strategy unavailable to stock investors.

- Long-term capital gains treatment: Just like stocks held over one year, long-term real estate gains are taxed at capital gains rates rather than ordinary income rates.

For investors in higher income tax brackets, the after-tax return advantage of mobile home park investing is often meaningfully larger than the pre-tax figures suggest. A CPA or financial advisor familiar with real estate can help model this for your specific situation.

Liquidity: The Key Trade-Off

Stocks win here decisively. Public equities can be sold in seconds. Mobile home park syndications typically require a 3-7 year capital commitment, with limited ability to exit early.

This means mobile home park investing is not appropriate for capital you may need in the near term. Most operators require investors to meet accredited investor standards and commit to the full hold period.

The right framework: think of mobile home park investing as a place for long-term capital — money you do not need to access for at least five years. Liquidity-sensitive funds belong in stocks, money market accounts, or other liquid vehicles.

Portfolio Fit: Can You Own Both?

Absolutely — and for many investors, owning both is the right answer.

A portfolio that includes both public equities and private real estate gets meaningful benefits from both worlds: liquidity from stocks, income stability and tax efficiency from real estate, and genuine diversification across uncorrelated asset classes.

A common approach for accredited investors is to allocate 10-30% of investable assets to alternatives like real estate, with the remainder in public markets. The right split depends on your income needs, risk tolerance, time horizon, and liquidity requirements.

Mobile home park investing is not a replacement for the stock market. It is a complement — one that has historically provided strong, tax-efficient cash flow with low correlation to public market volatility.

Bottom Line

Neither mobile home parks nor the stock market is universally better. They serve different purposes and work differently in a portfolio.

If you are an accredited investor looking for stable cash flow, meaningful tax advantages, and exposure to an asset class with structural demand and limited new supply, mobile home park investing deserves a serious look alongside — not instead of — your public market holdings.

To go deeper on how passive mobile home park investing works, explore our full passive investing guide or our comprehensive mobile home park investing guide. If you are interested in learning more about mobile home park investing, reach out and we would be glad to have a conversation.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.