If you’re researching mobile home park investing, you’ll run into the term cap rate constantly. It’s the single most commonly used metric for valuing commercial real estate — and mobile home parks are no exception. Understanding cap rates is essential whether you’re buying your first mobile home park, evaluating a syndication deal, or simply trying to understand what drives value in this asset class.

This guide explains exactly what a mobile home park cap rate is, how to calculate it, what a good cap rate looks like in today’s market, and why cap rates alone don’t tell the whole story.

What Is a Cap Rate and Why Does It Matter?

A capitalization rate (cap rate) is a quick way to express the relationship between a property’s income and its value. The formula is simple:

Cap Rate = Net Operating Income (NOI) ÷ Purchase Price

For example, if a mobile home park generates $300,000 in net operating income and you’re buying it for $4,000,000, the cap rate is 7.5%.

Cap rates matter for two reasons. First, they give you a quick, apples-to-apples comparison across deals — a 5% cap rate in Charlotte is directly comparable to a 5% cap rate in Nashville. Second, cap rates function as a proxy for risk and market demand. Lower cap rates signal that buyers are willing to pay a premium (i.e., accept lower initial yields) because they believe in the market, the asset quality, or the growth prospects. Higher cap rates typically reflect higher perceived risk or a less competitive market.

How to Calculate Cap Rate on a Mobile Home Park

The math is straightforward, but the inputs require care. Here’s the correct process:

- Calculate Gross Income: Total lot rents collected — typically the primary revenue source in a mobile home park. Include any ancillary income (storage, laundry, late fees).

- Subtract Vacancy and Credit Loss: Use realistic vacancy based on current occupancy and market conditions.

- Calculate Operating Expenses: Property taxes, insurance, utilities, management fees, maintenance, and reserves. Do not include mortgage payments — cap rate is a pre-financing metric.

- NOI = Gross Income − Vacancy − Operating Expenses

- Cap Rate = NOI ÷ Value (or Purchase Price)

One important nuance: always underwrite mobile home parks on actual lot rents, not pro forma rents. Sellers frequently advertise cap rates based on optimistic rent projections. Your cap rate analysis should reflect today’s numbers, not a best-case scenario. For a deeper look at how to run the full numbers on a deal, see our guide on mobile home park underwriting.

What Is a Good Cap Rate for a Mobile Home Park in 2026?

There is no single “good” cap rate — it depends on the market, the asset quality, and your investment strategy. That said, here’s how cap rates generally break down in today’s mobile home park market:

Cap Rates by Market Tier (2026)

- Premium/Class A communities (150+ lots, city utilities, near major metros): 4.5–5.5%. These are institutional-quality assets in high-demand markets. Buyers accept lower initial yields in exchange for stability and appreciation potential.

- Stabilized/Class B communities (70–149 lots, good infrastructure, suburban markets): 5.5–7.0%. This is the most common range for privately-held mobile home parks transacting today. Strong fundamentals with room for value creation.

- Value-add/Class C communities (below-market rents, deferred maintenance, high vacancy): 7.0–10%+. Higher going-in cap rates reflect execution risk — the yield only materializes if you successfully execute the business plan.

The national average cap rate for manufactured housing communities is approximately 5.9% as of early 2026, down roughly 40 basis points from Q4 2024, reflecting continued investor demand for this asset class.

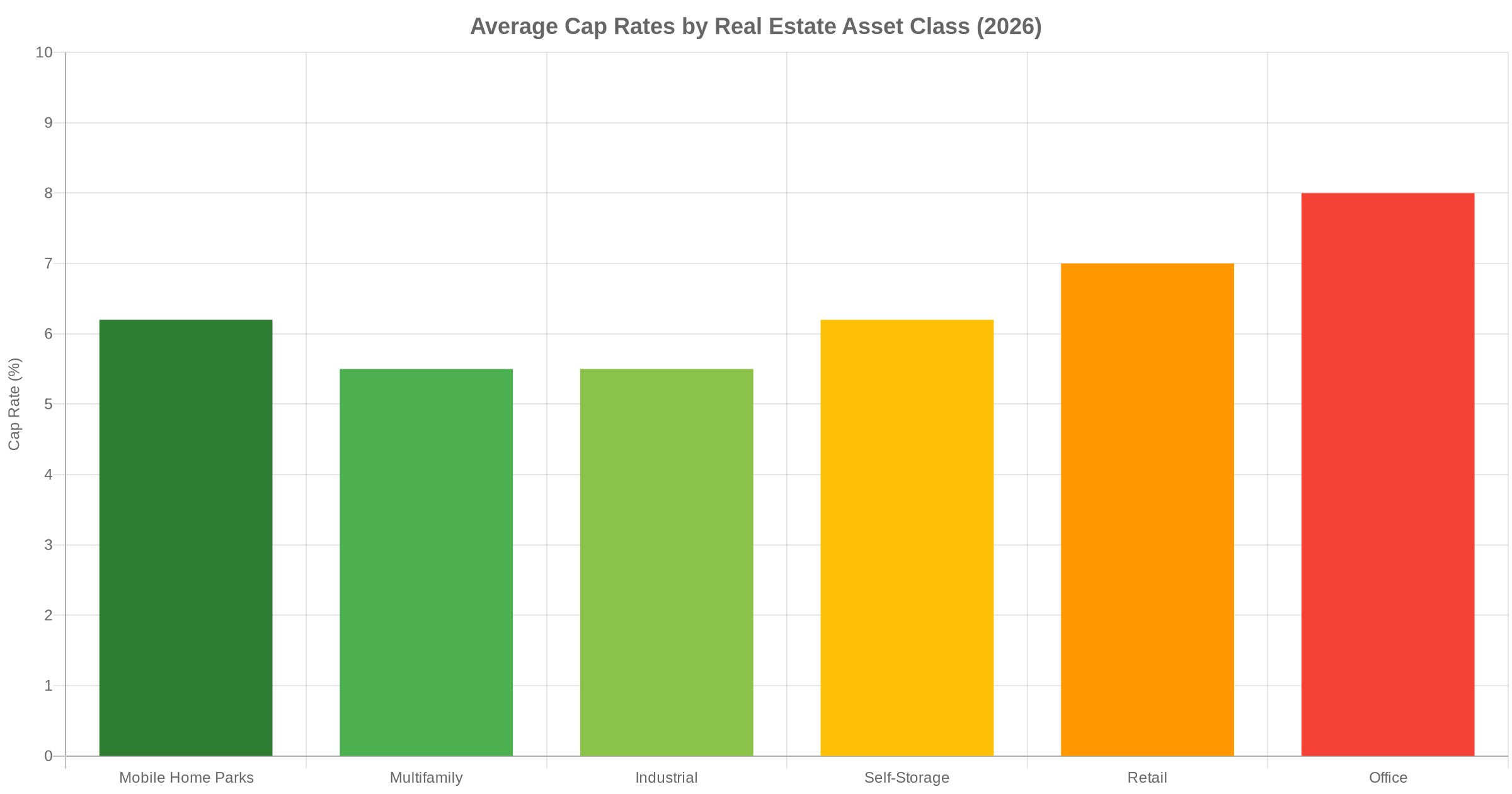

How Mobile Home Park Cap Rates Compare to Other Asset Classes

Mobile home parks sit in an attractive position relative to other commercial real estate sectors. Multifamily apartments currently trade around 5.5%, industrial is also near 5.5%, and office — still working through post-pandemic disruption — averages around 8.0%. Mobile home parks at roughly 6.2% average offer comparable or better yields to multifamily, with significantly better operating fundamentals.

The key differentiator: mobile home park tenants own their homes and rent only the land. Moving a manufactured home costs $5,000–$10,000 or more, which means turnover rates are dramatically lower. Annual tenant turnover in mobile home parks runs approximately 2.2% compared to 47% for apartment buildings. That stability directly supports NOI predictability — and NOI predictability is what drives cap rate compression over time.

For context on the full return picture, our analysis of mobile home park investment returns covers how cash-on-cash returns, appreciation, and tax benefits layer on top of cap rate income.

📋 The MHP Due Diligence Playbook

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — including how to verify the cap rate a seller is advertising.

Why Mobile Home Park Cap Rates Have Been Compressing

Cap rate compression — where buyers pay more for the same income, driving cap rates lower — has been the dominant trend in mobile home park investing over the past decade. Several structural forces drive this:

- Institutional demand: Large private equity firms, REITs, and pension funds have been moving into manufactured housing communities at scale. More capital chasing the same asset base compresses cap rates.

- Supply constraints: New mobile home park development is effectively prohibited in most jurisdictions due to zoning restrictions and community opposition. Approximately 20 new communities are created annually against a national stock of roughly 45,000. You cannot build your way out of the supply-demand imbalance.

- Recession resilience: Mobile home parks delivered positive NOI growth through both the 2008 financial crisis and the 2020 COVID downturn — a track record that commands a premium in uncertain economic environments.

- Rising lot rents: National average lot rents have been increasing 5–10% annually in many markets, with Florida seeing growth of 5.5–11% year-over-year. This rent growth supports continued NOI expansion even as values appreciate.

When a High Cap Rate Is a Red Flag

A high cap rate is not automatically a bargain. In mobile home park investing, an above-market cap rate often signals one or more of the following problems:

- Private utilities: Parks on well/septic or private wastewater systems carry significant capital expenditure risk. Buyers discount heavily because of potential replacement costs.

- High park-owned homes concentration: If the seller owns a large percentage of the homes in the park, those home rentals inflate NOI artificially. Once you strip out home-related income, the true lot rent NOI is much lower.

- Inflated pro forma rents: Sellers often advertise cap rates based on “market rate” rents rather than actual collected rents. Verify every rent on the rent roll.

- Deferred maintenance: Infrastructure issues (aging roads, failing utilities, deteriorating common areas) will show up as capital expenditures post-close that erode your actual returns.

- Location risk: A 9% cap rate in a shrinking rural market with declining population may reflect a permanently impaired asset, not an opportunity.

Verifying the real cap rate — not the advertised one — is one of the most critical steps in the due diligence process. Our mobile home park due diligence checklist walks through exactly how to audit the financials before you commit.

What Cap Rate Should You Target?

This depends on your investment thesis. If you’re acquiring a stabilized, cash-flowing asset in a growing market with no upside, you need the going-in cap rate to clear your return hurdles on day one. If you’re buying value-add — below-market rents, under-occupied lots, private utility conversion opportunity — then the going-in cap rate is less important than what you can drive it to over a 3–5 year hold.

Most experienced mobile home park investors think in terms of going-in cap rate vs. exit cap rate. If you buy at a 7.5% cap and improve the asset to where it would trade at a 6.5% cap, the cap rate compression alone creates significant value — even before accounting for NOI growth.

As a general framework for 2026: buying a stabilized mobile home park below 5% cap rate requires a strong conviction in rent growth or appreciation to generate acceptable returns. Anything in the 6–7.5% range for a well-located, city-utility community with upside is a reasonable target in today’s market. Above 8% should prompt serious questions about what risk you’re being compensated for.

Final Thoughts

Cap rates are a useful starting point, but they’re never the whole story. A mobile home park at a 6.5% cap rate with city utilities, below-market rents, and strong occupancy in a growing southeastern city is a fundamentally different investment than a 6.5% cap rate park on a well/septic system with stagnant lot rents and a declining tenant base. The cap rate is the same; the investment is not.

Use cap rates as a screening tool and a benchmark. Combine them with cash-on-cash return analysis, NOI growth projections, and a thorough review of the physical and financial condition of the asset. That’s how experienced investors separate the good deals from the ones that look good on paper.

📋 Ready to Evaluate Your Next Deal?

Get the MHP Due Diligence Playbook — the complete system for analyzing mobile home park acquisitions with confidence. Includes cap rate verification templates, rent roll audits, and a 55-page master checklist.

Frequently Asked Questions

What is the average cap rate for a mobile home park in 2026?

The national average cap rate for manufactured housing communities is approximately 5.9% in early 2026, down from around 6.3% in 2024. Premium, institutional-quality communities can trade at 4.5–5.5%, while stabilized smaller parks in secondary markets typically trade in the 6–7.5% range.

Is a higher cap rate always better for a mobile home park investor?

Not necessarily. A higher going-in cap rate can signal higher risk — private utilities, high vacancy, deferred maintenance, or weak market fundamentals. Experienced investors evaluate the source of the cap rate as much as the number itself. A 7.5% cap rate with clear value-add upside can be better than a 6% cap rate on a stabilized asset with no room to grow.

How does the mobile home park cap rate formula work?

Cap Rate = Net Operating Income ÷ Purchase Price. NOI is gross income minus vacancy and operating expenses (not including mortgage payments). For a mobile home park generating $250,000 in NOI purchased for $3,500,000, the cap rate is 7.1%.

How do mobile home park cap rates compare to apartment cap rates?

Mobile home parks (averaging ~6.2%) generally offer higher cap rates than multifamily apartments (~5.5%) while providing superior tenant retention and lower operational volatility. Apartment turnover averages around 47% annually; mobile home park turnover averages around 2.2%.

What factors cause mobile home park cap rates to vary by location?

Market size and population growth are the biggest drivers. Parks near major MSAs (100,000+ population) in growing Sun Belt states command lower cap rates (higher prices) due to stronger demand and appreciation potential. Rural or shrinking markets offer higher cap rates but carry more risk. Utility infrastructure (city water/sewer vs. private systems) also significantly affects where a park prices within a market range.