If you’ve spent any time studying mobile home park investing, you’ve probably read plenty about cap rates, lot rent upside, and value-add strategies. But one topic that doesn’t get nearly enough attention? Mobile home park insurance. Get it wrong, and a single storm, slip-and-fall, or tenant dispute can wipe out years of cash flow — or worse, expose you to a judgment that exceeds your net worth.

This guide breaks down the coverage types every mobile home park owner and operator needs, what you should expect to pay, and the mistakes that cost investors real money every year.

Why Mobile Home Park Insurance Is Different from Other Real Estate

Mobile home parks don’t fit neatly into standard commercial real estate insurance buckets. Unlike an apartment building where you own every square foot, a mobile home park typically involves land you own, tenant-owned homes sitting on that land, shared infrastructure (roads, utilities, common areas), and in some cases park-owned homes you rent out directly.

That layered ownership structure creates unique liability exposures. A tenant slips on a pothole in your privately maintained road. A tree from your property falls on a tenant’s home. A contractor working on the infrastructure injures himself and names you in a suit. Each scenario requires the right coverage to be fully protected.

Standard residential or commercial property policies are often inadequate for this asset class. You need coverage built for mobile home park operations specifically — and that starts with understanding the core policy types.

The Core Coverages Every Mobile Home Park Owner Needs

Commercial General Liability (CGL)

This is non-negotiable. A commercial general liability policy covers bodily injury and property damage claims arising from your operations. If a tenant or visitor is injured on your common areas, your CGL responds first. Most lenders require at least $1 million per occurrence / $2 million aggregate as a minimum. Depending on your park’s size, location, and history, you may want to carry more.

A key detail: your CGL should include premises and operations coverage, and it should be an occurrence policy (not claims-made), so you’re covered for incidents that happened during the policy period regardless of when the claim is filed.

Commercial Property Insurance

Your property policy covers the physical assets you own: the land improvements, infrastructure, clubhouses, common buildings, park-owned homes, and equipment. It does not cover tenant-owned homes — that’s their responsibility (and worth including in your lease addendum).

Be specific about what’s included. Roads, water lines, electrical pedestals, and utility infrastructure can represent significant replacement value. Confirm your policy covers these items — some carriers exclude underground infrastructure or charge separately for it.

Workers Compensation

If you have employees — a full-time manager, maintenance staff, groundskeepers — workers’ compensation is legally required in most states. Even if you use contractors, be careful: misclassified workers or contractors without their own coverage can expose you to liability. Verify that any contractor you hire carries their own workers’ comp before they set foot on your property.

Specialty Coverages Worth Considering

Umbrella and Excess Liability

A commercial umbrella policy sits on top of your CGL and provides additional limits when underlying coverage is exhausted. For a mobile home park with 50+ lots, a $1 million umbrella is a modest investment that could be the difference between a manageable insurance payout and a judgment that threatens your entire operation.

Given today’s litigation environment, many experienced mobile home park operators carry $5 million or more in total liability limits.

Flood Insurance

If your park is in or near a FEMA-designated flood zone, your lender will require it. But even outside flood zones, many mobile home park communities are susceptible to localized flooding — low-lying lots, proximity to drainage areas, aging infrastructure. Standard property policies exclude flood damage. The National Flood Insurance Program (NFIP) is one option; private flood carriers often provide better terms and higher limits.

Equipment Breakdown Coverage

If your park has its own water or sewer system, lift stations, or other mechanical infrastructure, equipment breakdown coverage fills a gap in standard property policies. A failed pump or compressor can mean days of service disruption and tens of thousands in emergency repairs. The premium is typically modest relative to the exposure.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

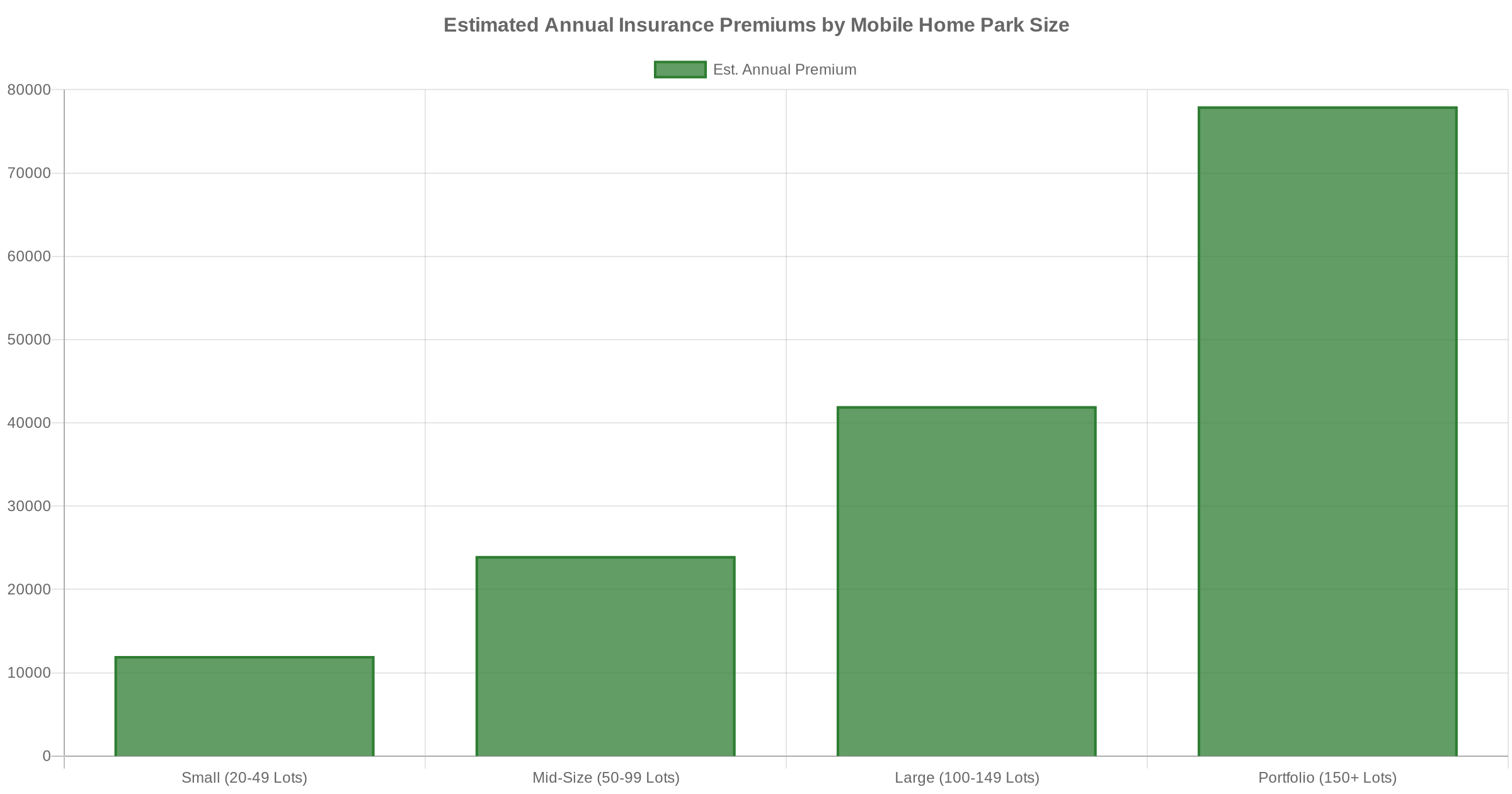

How Much Does Mobile Home Park Insurance Cost?

Premiums vary significantly based on park size, location, claims history, infrastructure type (city utilities vs. private), and whether you have park-owned homes. The chart below shows rough estimated annual premium ranges based on park size:

As a rough rule of thumb, budget $150–$350 per lot per year for a combined property and liability package. Parks with private wells or septic systems, older infrastructure, or coastal exposure will be at the higher end. Parks on city utilities with newer electrical systems in low-risk states will trend lower.

Get quotes from at least 3 carriers — and ideally work with a broker who specializes in manufactured housing. Standard commercial real estate brokers often struggle to place mobile home park coverage competitively.

Common Insurance Mistakes Mobile Home Park Operators Make

1. Underinsuring infrastructure. The replacement cost of roads, utility lines, and electrical pedestals is often higher than owners realize. Confirm your policy covers these assets at full replacement value — not actual cash value (which factors in depreciation).

2. Not requiring tenants to carry renters insurance. Your property policy does not cover tenant belongings or tenant-owned homes. If a fire damages a tenant’s home and your park’s negligence is alleged, you’re exposed. Requiring renters insurance (or a minimum liability policy) in your lease reduces that risk and can shift claims away from your carrier.

3. Using residential coverage on park-owned homes. If you own homes in your park and rent them out, they need to be scheduled on your commercial policy, not covered under a standard residential landlord policy. Insurers can deny claims on homes that are not properly disclosed as commercial rental properties.

4. Skipping the annual review. Your park evolves — you add homes, upgrade infrastructure, change managers. Your policy needs to reflect your current exposure. Review coverage limits and exclusions with your broker every year, not just at acquisition.

5. Ignoring the claims history before buying. As part of your mobile home park due diligence process, request a 5-year CLUE (Comprehensive Loss Underwriting Exchange) report on the property. A history of frequent claims — especially water, fire, or liability — will affect your ability to get coverage and what you pay for it. This is one of those first-time investor mistakes that is easy to avoid once you know to look for it.

How to Find the Right Insurance Broker

Not every commercial insurance broker understands the manufactured housing space. Look for brokers who specifically list mobile home parks or manufactured housing communities in their areas of expertise. Organizations like the Manufactured Housing Institute (MHI) or state manufactured housing associations sometimes maintain broker directories.

The best brokers in this space have relationships with specialty carriers — companies like Foremost, Great American, and select Lloyd’s syndicates that regularly underwrite mobile home park risks. They will also know how to structure coverage for parks with a mix of tenant-owned and park-owned homes, which requires careful coordination between policy types.

What Passive Investors Should Know About Insurance

If you are evaluating a mobile home park deal as a passive investor — reviewing a syndication or fund opportunity — insurance is part of your due diligence on the operator. Ask to see current certificates of insurance, confirm the limits are appropriate for the park’s size and age, and verify the operator’s policy covers park-owned homes if applicable.

An operator who cuts corners on insurance is cutting corners elsewhere too. Adequate coverage is a baseline sign of professional operations.

The Bottom Line

Mobile home park insurance is not the most glamorous part of the business — but it is one of the most consequential. The right coverage protects your cash flow, your equity, and your ability to keep operating through the inevitable unexpected events. Treat it as seriously as you treat your underwriting.

Take the time to find a specialized broker, get competitive quotes, and review your coverage every year as your portfolio grows. It is one of the areas where a few hours of attention can save you six figures in losses. For a deeper look at the full investment framework, explore our comprehensive mobile home park investing guide.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.