Buying your first mobile home park can be one of the most rewarding real estate investments you’ll ever make — or one of the most expensive lessons. The difference often comes down to a handful of avoidable mistakes that trip up nearly every first-timer who skips the foundational work.

Mobile home park investing has attracted serious attention from both individual investors and institutional players in recent years, and for good reason: strong cash flow, resilient demand for affordable housing, and low tenant turnover make these assets genuinely compelling. But the learning curve is real. This guide covers the most common mistakes first-time mobile home park investors make — and what to do instead.

Mistake 1: Confusing Physical Occupancy with Economic Occupancy

A seller tells you the park is 85% occupied. That sounds solid. But what they may not be telling you is how many of those occupied lots are actually paying rent on time.

Physical occupancy counts homes sitting on lots. Economic occupancy counts homes generating actual rent. These two numbers can diverge dramatically — especially in parks where delinquencies have been allowed to slide, where residents are on informal payment plans, or where park-owned homes sit occupied but uncollected.

Before you close, get 12 months of actual rent rolls and bank statements. Verify every unit that is supposedly paying. If a park claims 80% physical occupancy but only 63% of lots are producing income, your pro forma is built on sand.

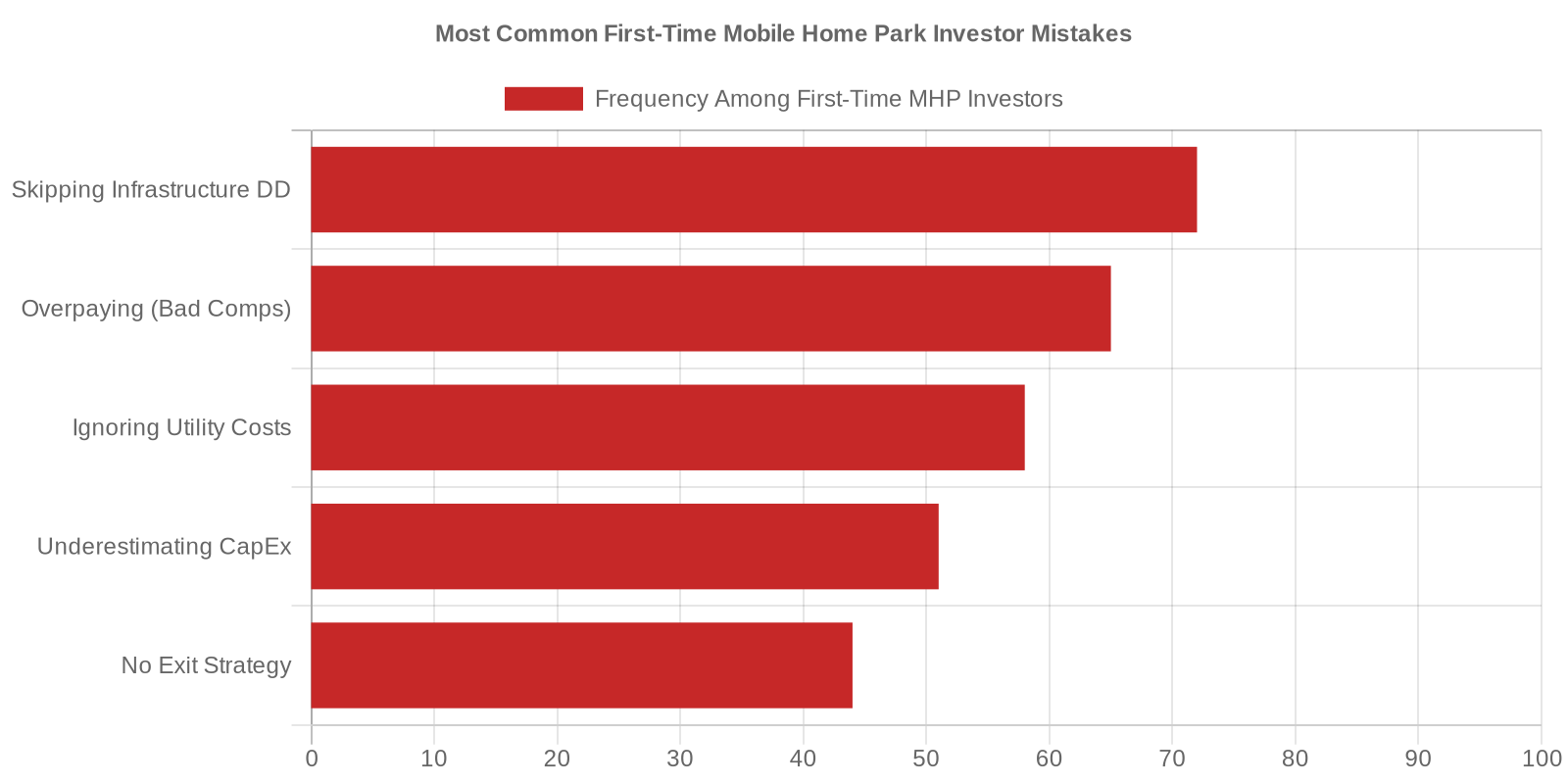

Mistake 2: Ignoring the Utility Infrastructure

Nothing derails a mobile home park acquisition faster than an infrastructure problem that was not caught in due diligence. Water, sewer, and electrical systems in older parks are often aging — and repairs can run into the hundreds of thousands of dollars.

The most dangerous scenarios:

- Well and septic systems: These are the operator’s responsibility, expensive to maintain, and subject to regulatory scrutiny. City water and city sewer is almost always the better bet for a first acquisition.

- Master-metered utilities: If you are paying the entire park’s water or electricity bill and charging residents a flat fee, you are bleeding money. Sub-metering or converting to resident-responsible utilities is a major value-add play — but it costs capital and time.

- Aging underground lines: Cast iron sewer lines, galvanized water mains, and aluminum wiring are not visible in a drive-through inspection. Budget for a sewer scope, water pressure test, and electrical audit.

First-time investors often budget for the purchase price and miss the infrastructure capital stack entirely. Get an independent inspection — not just the seller’s representations.

Mistake 3: Not Understanding Park-Owned Homes vs. Tenant-Owned Homes

This is one of the most consequential distinctions in mobile home park investing, and first-time investors routinely underestimate it.

Tenant-owned homes are the ideal model. The resident owns the home; you collect lot rent. You are essentially a land landlord — low maintenance, low liability, high margin. If a tenant does not pay, the eviction process is typically simpler and faster than a traditional rental eviction.

Park-owned homes are more complex. You own the home, you are responsible for maintenance, and you are exposed to the same headaches as any rental landlord — repairs, tenant damage, vacancy. Park-owned home income looks good on paper, but the expense load is significantly higher.

A mobile home park with 40% park-owned homes requires a very different underwriting model than one that is fully tenant-owned. Many first-time investors underwrite both the same way and get burned when maintenance costs arrive.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Mistake 4: Choosing the Wrong Market

Mobile home park investing is hyperlocal. A park in a growing metro with strong employment and population growth is a fundamentally different asset than the same-sized park in a shrinking rural county — even if the cap rates look similar at first glance.

First-time investors often chase yield. A 10% cap rate in a struggling market looks more attractive than an 8% cap in a growing one. But the risks are not equal. Infill is nearly impossible without local housing demand. Lot rent growth stalls. Exit options narrow significantly in thin markets.

A sound market selection framework focuses on locations within one hour of a major metro with 100,000 or more in population, in states with landlord-favorable regulatory environments. That is not arbitrary — it is a framework built from years of deal analysis and market-level underwriting.

Mistake 5: Rushing Due Diligence

Sellers set deadlines. Brokers create urgency. And first-time investors, afraid to lose a deal, sometimes let due diligence get compressed or incomplete.

This is where deals go sideways. Thorough due diligence on a mobile home park includes:

- 12 months of actual bank statements (not just seller-provided profit and loss statements)

- Individual review of every lease or lot agreement

- Physical inspection of every home and all common areas

- Sewer scope and water/utility infrastructure audit

- Title search and lien check on every park-owned home

- Review of all local ordinances and zoning compliance

- Verification of permits and any outstanding code violations

Cutting this process short costs far more than any time savings at closing. One undetected septic issue or a title problem on a bank-titled home can blow up your returns for years.

The MHP Due Diligence Playbook

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal. Built from real acquisitions, not theory.

Mistake 6: Getting the Cap Rate Wrong

Mobile home park cap rates are frequently misrepresented — not always intentionally, but often because sellers present seller-adjusted net operating income figures that do not survive scrutiny.

Common cap rate inflation tactics include:

- Pro forma rents: Using market-rate lot rents rather than what tenants are actually paying today

- Excluding management fees: If you plan to self-manage, a seller might omit an 8-10% management expense. The moment you hire a professional manager, that expense appears immediately.

- Understating maintenance: One below-average expense year does not represent normalized costs

- Capitalizing vacant lot income: Infill projections presented as present value, when infill is not free, fast, or guaranteed

Always underwrite to actual trailing 12-month income and normalized expenses. Add back a management expense even if you plan to self-manage initially. Our detailed breakdown of how mobile home park cap rates work walks through the mechanics and what a good cap rate actually looks like in 2026.

Mistake 7: Underestimating Infill Complexity

Vacant lots are both the biggest opportunity and the biggest trap in mobile home park investing. Every vacant lot is lost revenue — but filling it requires capital, time, and the right market conditions.

First-timers often underwrite infill too optimistically. The reality is that sourcing affordable manufactured homes, arranging resident financing, completing site preparation, and connecting utilities typically takes 18-24 months per lot tranche — at a cost of $5,000-$15,000 or more per lot to execute properly.

Model infill as upside, not base case. Do not underwrite income from vacant lots until it is contracted and the homes are physically delivered to site.

Mistake 8: Underestimating the Importance of Management

Mobile home parks are not passive investments if you own them directly. They require active management — rent collection, maintenance coordination, community rules enforcement, and relationship management with long-term residents who have often lived in the community for decades.

Many first-time investors either try to self-manage from a distance or hire a property manager without vetting their mobile home park-specific experience. General residential property management does not always translate to the unique dynamics of a land-lease community.

Budget for professional management from day one. An 8-10% management fee on gross revenue is a legitimate operating expense. If you are interested in how experienced operators approach this question, our post on active vs. passive mobile home park investing covers the tradeoffs in detail.

What to Do Instead: A First-Timer’s Framework

Most of these mistakes share a common root: not knowing what you do not know before making an offer. The fix is building a systematic, checklist-driven evaluation process before you go under contract on any deal.

The complete mobile home park investing guide is the right starting point for building that foundation — covering market selection, deal analysis, financing, and operations in one place.

From there, learning to read the numbers correctly — particularly how to build a proper pro forma and stress-test your assumptions — is the next critical step. Our post on mobile home park underwriting walks through the deal analysis process from first look through final model.

The Bottom Line

First-time mobile home park investors do not fail because mobile home parks are bad investments. They fail because they skip steps, trust unverified seller numbers, and underestimate the operational complexity of what looks like a simple asset class.

The investors who do well consistently do three things: they build a repeatable due diligence process, they underwrite conservatively, and they either have experienced management in place or partner with operators who do.

If you are learning more about mobile home park investing and want to understand how experienced operators think about deal evaluation, reach out — we are happy to have a conversation.

Ready to Evaluate Your Next Deal?

Get the MHP Due Diligence Playbook — the complete system for analyzing mobile home park acquisitions with confidence. 10 video modules, 55-page master checklist, and 9 deal-ready templates.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.