Most inherited wealth doesn’t last. A lump-sum payout — whether it’s a stock portfolio, a savings account, or the proceeds from selling a family business — tends to get spent, diluted across siblings, or eroded by lifestyle inflation within a generation or two. The problem isn’t the size of the inheritance. It’s the structure.

Real estate changes the equation. Income-producing real estate, specifically, turns a one-time asset into a cash flow machine that can sustain your heirs for decades. And among all real estate asset classes, mobile home parks may be the most durable legacy asset you can own — for reasons that have little to do with luck and everything to do with structure.

The Problem with Traditional Inheritance Models

Consider what most people leave to their heirs: retirement accounts, investment portfolios, life insurance proceeds, or real estate that gets liquidated upon sale. Each of these generates a one-time event — a check. Once that check is cashed, the income stream is gone.

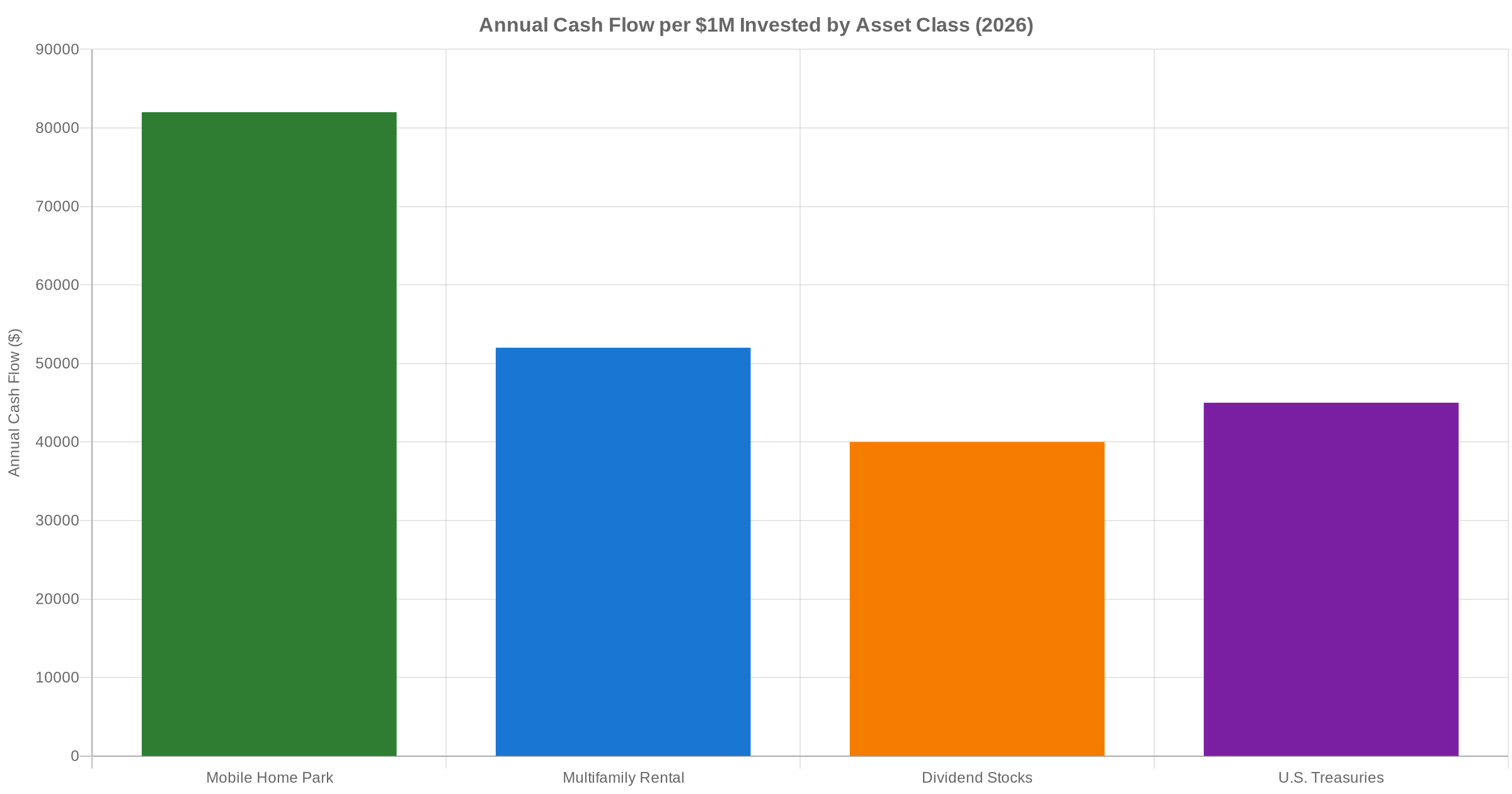

Contrast that with a well-run mobile home park. A 100-lot community generating $700 per lot in monthly lot rent produces approximately $70,000 in gross revenue per month — before expenses. After operating costs, debt service, and reserves, a healthy park might generate $25,000 to $45,000 in monthly cash flow. That income does not disappear when you die. It transfers to your heirs.

The difference is the same reason a pension beats a 401(k) lump sum for retirees who want income security: recurring beats one-time, every time.

Why Mobile Home Parks Generate Such Durable Cash Flow

The lot rent model is the key. In a typical mobile home park, the operator owns the land and leases individual lots to residents who own their own homes. This creates an unusually sticky tenant relationship: moving a manufactured home costs between $3,000 and $10,000 or more, so residents have a strong financial incentive to stay put.

The result? Annual tenant turnover in mobile home parks averages approximately 2.2% — compared to roughly 47% for apartment communities. That translates directly into lower vacancy losses, lower marketing costs, and a more predictable income stream year over year.

National occupancy for manufactured housing communities sits at approximately 93–94% (per Berkadia’s 2025 Manufactured Housing Annual Report), with Pacific region markets running as high as 99%. Lot rents have grown an average of 7% year-over-year nationally, well ahead of inflation. These are not speculative projections — they reflect two-plus decades of demonstrated performance through recessions, pandemics, and interest rate cycles.

The Estate Planning Advantages of Mobile Home Park Ownership

Land Ownership Is Permanent

Unlike manufactured homes, which depreciate over time, the land beneath them does not. Mobile home park operators own the land — the scarce, finite resource. With approximately 45,000 mobile home park communities in the United States and new zoning making it nearly impossible to build new ones, existing land in desirable locations only becomes more valuable over time.

LLC Structures and Stepped-Up Basis

For mobile home park estate planning, ownership through a properly structured LLC provides several advantages. Pass-through taxation keeps things simple — income flows directly to members without corporate-level taxation. And when the park passes to heirs at death, the cost basis resets to current fair market value under the stepped-up basis rules of IRC Section 1014.

Here’s why that matters: if you purchased a mobile home park for $2 million twenty years ago and it’s worth $5 million at the time of your death, your heirs inherit it at a $5 million cost basis. If they sell it immediately, they owe zero capital gains tax on that $3 million of appreciation. This is one of the most powerful tax-transfer mechanisms in the U.S. tax code — and income-producing real estate is uniquely positioned to take advantage of it.

The tax benefits of mobile home park investing extend well beyond estate planning, but the inheritance dimension is often underappreciated even by sophisticated investors.

Inflation Protection Built In

Unlike a bond or a fixed annuity, mobile home park lot rent income grows over time. As lot rents rise with inflation — or ahead of it — the income stream your heirs receive in year 10 is likely larger than in year 1. This built-in growth protects multi-generational purchasing power in a way that fixed-income assets cannot.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

What Passive Investors Should Know About Legacy Planning

Not every investor wants to own and operate a mobile home park directly. For passive investors who participate as limited partners in mobile home park syndications, legacy planning works differently — but is still very achievable.

Limited partner interests can be transferred through trusts, wills, or beneficiary designations on the entity. Distributions from the syndication continue flowing to whoever holds the LP position. Understanding what returns to expect from passive mobile home park investments helps heirs understand what they’re receiving and why the income is sustainable.

Consult an estate attorney familiar with private placement interests to ensure your LP position is properly structured for transfer without triggering unnecessary tax events or administrative complications.

Planning for a Successful Ownership Transfer

Operational Knowledge Transfer

One of the most important — and most overlooked — aspects of mobile home park estate planning is the transfer of operational knowledge. A mobile home park isn’t a passive brokerage account; it requires management, vendor relationships, resident communication, and compliance oversight.

If your heir intends to take over operations, involve them early. Shadow visits, introductions to the on-site manager and key vendors, and familiarity with financial reporting systems all matter. If they don’t want to operate, professional property management companies specializing in manufactured housing communities exist and can take over seamlessly.

Legal Structure Matters Before You Need It

Don’t wait until your health is in question to structure your ownership for transfer. Family limited partnerships, irrevocable trusts, and LLCs with clear operating agreements and succession clauses make an enormous difference in how smoothly — and how affordably — ownership changes hands.

An estate attorney experienced in real estate holding structures is worth the investment. The legal cost of proper planning is a fraction of the estate litigation, forced sale, or tax exposure that can result from an unplanned transfer.

Is a Mobile Home Park the Right Legacy Asset for Your Family?

Not every family situation calls for the same solution. But for investors who want to build generational wealth through real estate that produces income for their children and grandchildren — rather than a one-time check — mobile home parks offer a compelling combination of:

- Durable, recurring lot rent income with below-average vacancy risk

- Land ownership that appreciates over time without depreciation drag

- Stepped-up basis benefits that eliminate decades of built-up capital gains at transfer

- Inflation-adjusted income growth that preserves purchasing power across generations

- Structural defensibility from new supply — no one is building new mobile home parks at scale

Explore the complete mobile home park investing guide to understand the full scope of how this asset class works before building your legacy strategy around it.

Frequently Asked Questions

Can I put a mobile home park in a trust?

Yes. Mobile home parks held in LLCs can be placed in a revocable living trust, which avoids probate and allows for a smoother transfer to beneficiaries. Irrevocable trusts are also used for more advanced estate planning strategies that reduce estate tax exposure. Work with an estate attorney experienced in real property holdings to determine which structure is most appropriate for your situation.

Does my heir need to actively manage the mobile home park?

No. Professional property management companies specialize in manufactured housing communities and can handle day-to-day operations — from rent collection and maintenance coordination to resident relations and regulatory compliance. Your heir can receive the income as a passive beneficiary without any operational involvement.

What is stepped-up basis and how does it apply to mobile home parks?

Stepped-up basis refers to the IRS rule (IRC Section 1014) that resets an inherited asset’s cost basis to its fair market value at the date of the original owner’s death. For a mobile home park that has appreciated significantly, this eliminates the capital gains tax on all appreciation that occurred during the original owner’s lifetime. It is one of the most valuable tax advantages in the estate planning toolkit for real estate investors.

How do mobile home park distributions work when a passive LP position is inherited?

When a limited partner interest in a mobile home park syndication is inherited, the heir steps into the same position — receiving distributions according to the same waterfall and schedule as before. The syndication’s operating agreement governs the mechanics of how LP interests can be transferred, so reviewing that document (and notifying the general partner) is an important step when the position changes hands.

Are mobile home parks taxed differently when inherited?

The inheritance itself is generally not a taxable event for the heir (federal estate tax only applies to estates above the federal exemption threshold). The heir receives a stepped-up basis, which reduces or eliminates capital gains tax on future appreciation. Ongoing income from the mobile home park is taxed as ordinary income or pass-through income at the heir’s rate, though depreciation deductions can offset a significant portion of that income — just as they did for the original owner.

The Bottom Line

Most assets get inherited once and then spent. A well-structured mobile home park gets inherited and then generates income for a decade or more — potentially indefinitely. The combination of sticky tenancy, land scarcity, inflation-linked lot rent growth, and estate planning tools like stepped-up basis makes the asset class unusually well-suited for investors who think in generations, not just years.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.