Most mobile home park investors start with a single property. But the investors who build real wealth don’t stop there. Building a mobile home park portfolio—owning and operating multiple parks across different markets—is how you compound cash flow, diversify risk, and create the kind of financial independence that a single asset can’t deliver.

This guide breaks down exactly how to scale, step by step, from your first mobile home park to a multi-property portfolio that works without you being on-site every day.

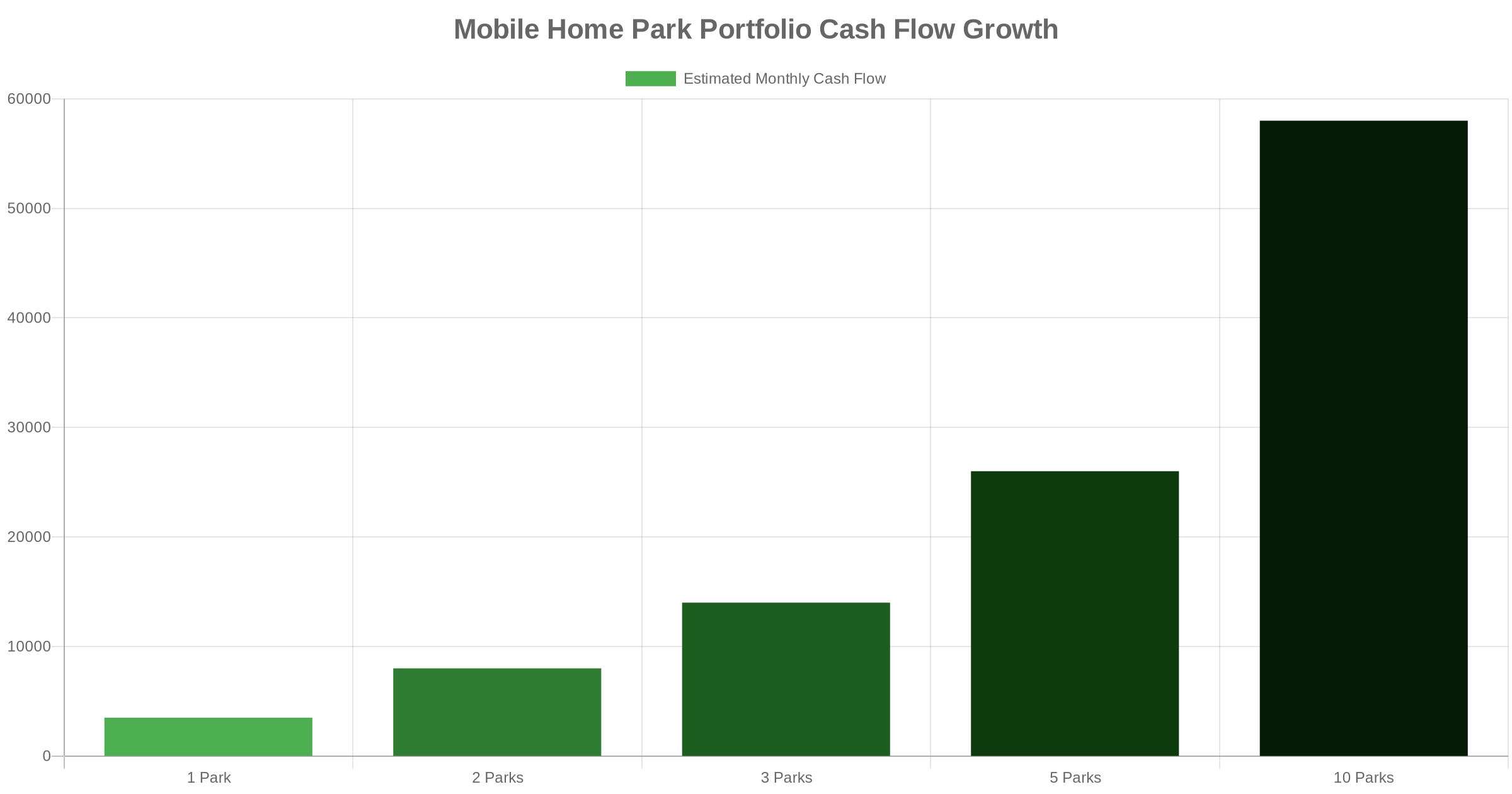

Why a Portfolio Approach Beats a Single-Asset Strategy

A single mobile home park is a business. A portfolio of mobile home parks is a platform. Here’s why the distinction matters:

- Diversified income: One park with one bad manager, one utility failure, or one local economic shock can wipe out your cash flow. Three parks in different markets provide a buffer.

- Economies of scale: Your third or fourth park costs far less to manage than your first. You’ve already built the playbook, the vendor relationships, and the systems.

- Financing leverage: A track record of successful mobile home park operations makes lenders far more comfortable writing larger loans at better rates.

- Valuation compounding: Every dollar of net operating income you add to a mobile home park portfolio gets multiplied by a cap rate. At a 7% cap rate, $10,000 of annual NOI increase equals $142,857 of value creation.

If you’re serious about mobile home park investing as a long-term wealth strategy, thinking in terms of a portfolio from day one will change how you make decisions at every stage.

Step 1: Master Operations at Your First Property

Before you add a second mobile home park, you need to fully understand the first. This isn’t about being conservative—it’s about building the operational foundation that makes scaling possible.

In your first 12–18 months, focus on:

- Stabilizing occupancy to 90%+ paying residents

- Optimizing lot rents to market rate using local comps and demand data

- Documenting your management system: rent collection, maintenance workflows, vendor contracts

- Building reporting structure so you can monitor performance remotely

The operators who scale fastest are the ones who treated their first mobile home park like a training ground, not just a cash flow machine. When you understand your first park deeply, you’ll know exactly what to look for—and what to avoid—in the next one.

Step 2: Build the Financial Foundation for Your Next Acquisition

Capital is the limiting factor for most mobile home park investors. Here’s how experienced operators build equity and liquidity to fund future acquisitions:

- Cash-out refinance: Once your first mobile home park has been stabilized and seasoned (typically 2–3 years), a cash-out refinance can unlock equity to deploy into a second deal without selling.

- Retained cash flow: Don’t spend every distribution. Bank a portion as reserves for future down payments.

- Bring on limited partners: Many operators grow from single-asset owners into syndicators when they realize LP capital lets them scale faster than their own balance sheet allows. If you want to learn more about mobile home park investing, reach out and we’ll set up a call.

Step 3: Choose Your Next Market Strategically

Your second mobile home park shouldn’t just be the next deal that crosses your desk. Deliberate market selection is what separates a collection of random properties from a true mobile home park portfolio.

Key market criteria for portfolio growth:

- Population growth: Target metros with 3–5%+ population growth over the last decade. Demand for affordable housing rises with population.

- Employment diversification: Avoid single-employer markets. When the plant closes, your residents leave.

- Regulatory environment: Some states have more tenant-friendly legislation that can complicate operations. Know the rules before you buy. (See our state guides for North Carolina and Tennessee.)

- Cap rate vs. growth trade-off: Higher-growth markets often have compressed cap rates. Lower-growth markets offer better entry yields. Your portfolio should balance both. Learn how cap rates affect your return in our guide to mobile home park cap rates explained.

Many experienced operators concentrate in 2–3 regional markets rather than spreading coast-to-coast. Depth of market knowledge is a competitive moat—it helps you find deals others miss and manage more efficiently with local vendor networks.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Step 4: Structure Your Financing for Scale

The way you finance your first mobile home park probably won’t work for your fifth. Here’s how financing evolves as a portfolio grows:

- Community bank loans: Strong for your first 1–3 deals. Relationship-driven, flexible underwriting, but limited by the bank’s balance sheet.

- Agency debt (Fannie Mae/Freddie Mac): Non-recourse, long amortization, lower rates. Requires stabilized properties and a proven operator track record. This is the engine of most large mobile home park portfolios.

- CMBS loans: Non-recourse and available at scale, but less flexible for management changes or early payoff.

- Seller financing: Often available from retiring mom-and-pop operators who prefer installment income to a lump sum. Excellent for off-market deals where the seller values terms over price.

Our full breakdown covers everything you need to know about mobile home park financing options.

Step 5: Build the Team Before You Need It

One of the biggest scaling mistakes is adding a second or third mobile home park before your team is ready. Here’s what a growth-ready operator team looks like:

- Onsite manager (per property): Handles rent collection, minor maintenance coordination, and resident communication

- Regional manager (every 3–5 parks): Oversees onsite staff, handles escalations, and drives performance across properties

- Bookkeeper/accountant: Mobile home park accounting has nuances—pass-through utilities, lot vs. home income—that require someone familiar with the asset class

- Maintenance vendor network: Pre-vetted plumbers, electricians, and general contractors in each market

- Property management software: Tools like Rent Manager or Buildium centralize lease management, maintenance tracking, and financials as your portfolio scales

The best operators hire for the portfolio they want, not the one they have. Bringing on a regional manager before you’re stretched is often what makes the next acquisition operationally feasible.

Step 6: Know When (and When Not) to Add Another Property

Portfolio growth isn’t always the right move. Here are the signals that tell you it’s time—and the ones that say wait:

You’re ready to acquire when:

- Current properties are at 90%+ occupancy for 12+ consecutive months

- You have 6+ months of operating reserves across all properties

- Your management team can handle the current portfolio without you daily

- You have a clear debt strategy and the equity or LP capital to execute

You should wait when:

- You have unresolved operational issues at existing properties

- You’re overleveraged or running thin cash reserves

- You don’t have experienced management lined up for the new market

- The deal doesn’t meet your underwriting criteria but you want to grow

Discipline in deal selection is what protects a portfolio. One bad acquisition can consume the cash flow from three good ones. See our guide on mobile home park underwriting for the framework we use to evaluate every deal before moving forward.

Common Mistakes Investors Make When Scaling a Mobile Home Park Portfolio

- Growing too fast: Adding properties before mastering existing ones leads to operational chaos and compressed returns across the board.

- Geographic overextension: Operating parks in five different states before you have regional management is a recipe for poor oversight and expensive surprises.

- Ignoring infrastructure risk at acquisition: A mobile home park with aging water lines or failing electrical infrastructure can turn a promising deal into a money pit. Always include infrastructure due diligence in your underwriting.

- Undercapitalization: Thin reserves at one property become a portfolio-level crisis when unexpected capital expenditures hit. Maintain adequate reserves across all properties before acquiring more.

- Misaligned management incentives: Managers need compensation structures tied to occupancy, collections, and resident satisfaction—not just showing up.

Final Thoughts: Think Like a Portfolio Operator from Day One

The most successful mobile home park operators think about portfolio construction from their very first acquisition. They choose markets with room to grow, build systems that scale, and approach every deal with an eye on how it fits into the bigger picture.

Whether you’re evaluating your first mobile home park or planning your tenth, the principles are the same: buy right, operate well, build team depth, and let the compounding do its work.

For a deeper look at what separates good mobile home park investments from great ones, visit our comprehensive guide to mobile home park investments.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.