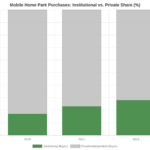

Private equity has discovered mobile home parks — and it’s changing the competitive landscape faster than many smaller operators anticipated.

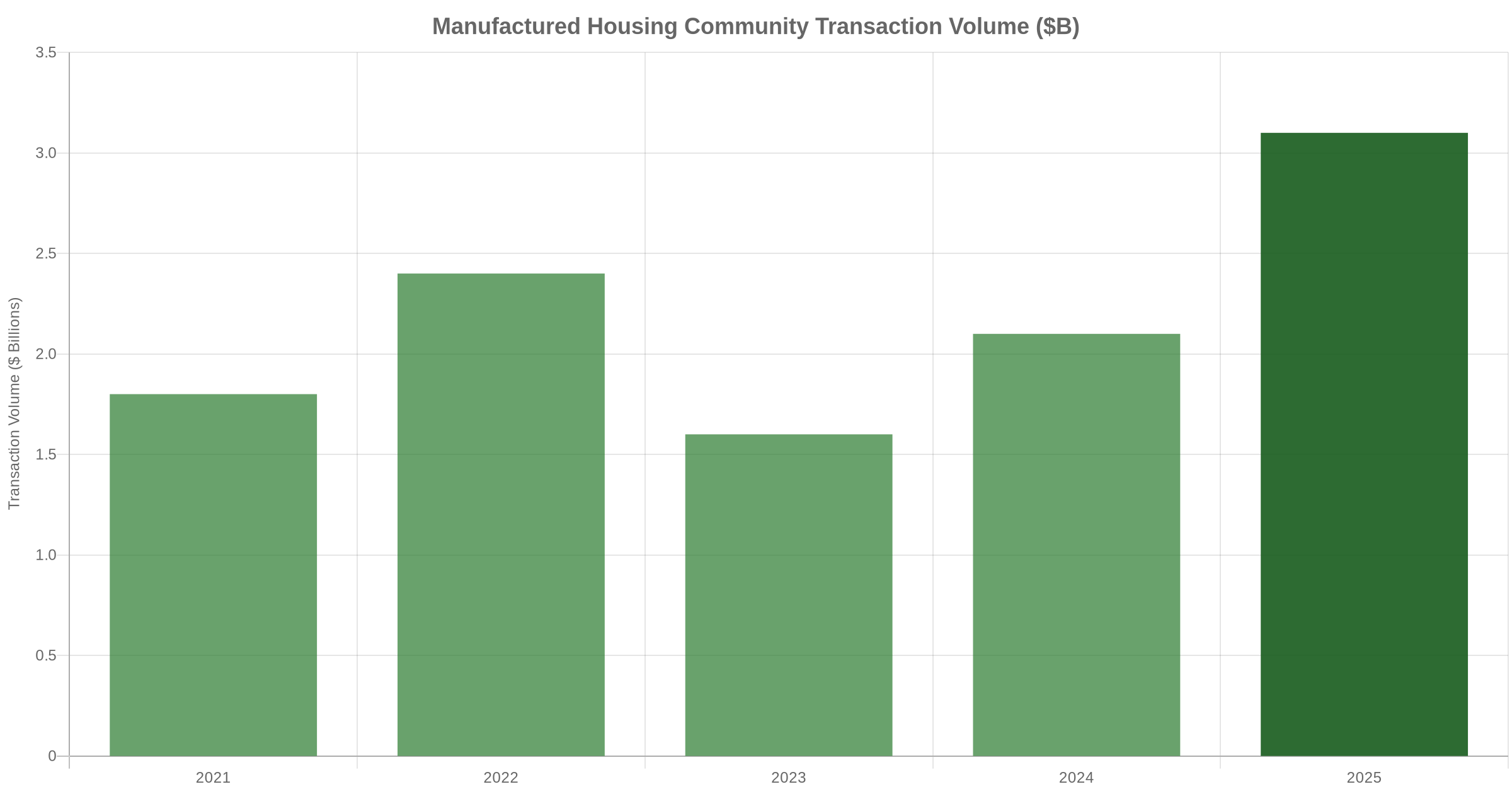

In 2025, transaction volume in manufactured housing communities jumped 47.1% year-over-year, with approximately 460 communities changing hands. That’s not a blip. That’s a structural shift in who’s buying — and why.

For smaller operators and regional buyers, the question isn’t whether institutional capital is here. It’s already here. The question is: what does it mean for valuations, deal flow, and the competitive edge that smaller operators have always held?

Why Private Equity Is Targeting Mobile Home Parks

The reasons are well-documented at this point, but worth spelling out clearly:

- Supply is permanently constrained. There are roughly 45,000 manufactured housing communities in the United States, and almost none are being built. New supply added each year represents roughly 0.04% of existing stock — compared to 3.8% for apartments. Zoning restrictions, NIMBY opposition, and permitting challenges have effectively turned mobile home park land into a fixed asset class.

- Occupancy is near historic highs. National occupancy in manufactured housing communities sits around 94%, up from 86.5% a decade ago. Demand is outpacing supply across most Sun Belt and Midwest markets.

- Lot rent is rising. National average lot rent reached approximately $752 per month in 2026, up roughly 7% year-over-year. For institutional buyers underwriting at scale, that trajectory is highly attractive.

- The affordability tailwind isn’t going away. With over 20 million Americans living in manufactured housing — and single-family home prices still elevated — the demand side of this equation remains structurally strong.

Institutional players — private equity funds, manufactured housing REITs like Sun Communities and Equity LifeStyle Properties, and family offices — have all increased their exposure to manufactured housing. The combination of stable net operating income, low tenant turnover (approximately 2.2% annually versus 47% for apartments), and recession-resilient demand makes mobile home parks a compelling institutional allocation.

Cap Rate Compression: What the Data Shows

The clearest signal of institutional money flowing into any asset class is cap rate compression — and manufactured housing has seen it significantly.

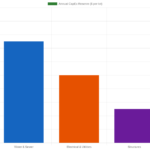

In 2026, cap rates for manufactured housing communities broadly break down as follows:

- Premium assets (well-located, 200+ lots, city utilities, strong rent growth markets): 4.0–5.0%

- Stabilized assets (90%+ occupied, solid utilities, mid-size markets): 5.0–7.0%

- Value-add assets (below-market rents, deferred maintenance, occupancy upside): 7.0–9.5%

That premium tier — 4 to 5 cap — is where institutional buyers are most active. A decade ago, 5.5–6.5% was the going rate for a well-leased, institutional-quality manufactured housing community. Institutional demand has compressed those rates by 100–150 basis points in many markets.

For a deeper look at cap rate mechanics in mobile home parks, see our guide: Mobile Home Park Cap Rates Explained: What’s a Good Cap Rate in 2026?

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

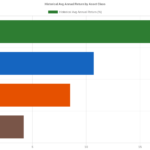

Where Institutional Capital Is Concentrating

Not all markets have been affected equally. Institutional buyers have been most aggressive in:

- Sun Belt metros — Florida, the Carolinas, Georgia, and Tennessee, where population migration is sustaining above-average rent growth. Florida lot rents have grown 5.5–11% annually in recent years.

- Midwest markets — Michigan, Ohio, and Indiana, where per-unit acquisition costs remain lower and value-add opportunities are more prevalent. New home shipments in the Midwest grew 17% year-over-year in 2025.

- Markets near major population centers — Institutional buyers want proximity to employment, services, and population density — the same fundamentals that support long-term lot rent growth.

Importantly, fragmented rural markets with sub-50-lot mobile home parks are still largely off the institutional radar. The economies of scale that make portfolio management attractive to a private equity fund don’t apply to a 35-lot park in a small rural market — and that gap represents an ongoing opportunity for operators who can work at that scale.

How Smaller Operators Are Competing and Winning

The good news for regional operators: institutional buyers have real limitations that smaller operators do not.

Speed and Flexibility

A private equity fund with multiple approval layers, investment committee sign-offs, and compliance requirements cannot move as fast as a regional operator who can underwrite a deal, negotiate terms, and close in 60 days. Motivated sellers — especially older owners looking for a straightforward exit — often value speed and simplicity over maximum price. Being able to say “I’ll close in 45 days, no contingencies” is a genuine competitive advantage.

Off-Market Relationships

The best mobile home park deals are built through direct relationships with owners — not auction processes. Off-market deal sourcing requires consistent outreach, patience, and trust built over time. Institutional buyers compete primarily in brokered deal flow. Operators who are actively building relationships with park owners in target markets access inventory that never hits the market at all.

Operational Presence and Community Care

A fund managing 50+ communities across 8 states cannot provide the same on-the-ground operational focus that a regional operator with 5–10 parks in contiguous markets delivers. Sellers who care about their residents’ wellbeing — and many long-time owners do — will sometimes accept a lower price to sell to a buyer they trust to manage the community responsibly.

Targeting the Value-Add Tier

Institutional buyers are largely chasing stabilized assets at compressed cap rates. The 7–9.5% value-add tier — mobile home parks with deferred maintenance, below-market rents, or occupancy upside — requires hands-on asset management, tolerance for execution risk, and operational expertise. These are exactly the deals that experienced smaller operators are best equipped to execute.

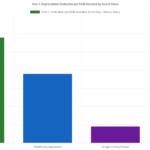

What Cap Rate Compression Means for Existing Owners

The flip side of compressed cap rates is significant appreciation for existing mobile home park owners. A park generating $500,000 in net operating income that traded at a 7.5% cap rate in 2018 implied a value of $6.67 million. At a 5.5% cap rate today — with the same income stream — that same asset implies a value closer to $9.1 million. That’s a 36% increase in implied value with zero operational improvement.

For passive investors in mobile home park syndications, cap rate movement can be a significant driver of equity returns at exit — independent of the income the asset generated during the hold period. Sponsors who acquired stabilized assets at 6.5–7% caps five to seven years ago are now exiting into a market where institutional buyers are competing hard for those assets.

To understand how this translates into investor returns, see: What Returns Can You Expect from Passive Mobile Home Park Investments?

Risks Worth Watching in 2026

Institutional attention on a formerly fragmented asset class brings scrutiny along with capital. A few risks worth monitoring:

- Regulatory pressure. As institutional buyers acquire mobile home parks and raise rents aggressively, political attention on manufactured housing communities has increased. Several states are advancing tenant protection legislation, right-of-first-refusal requirements, and rent increase notification laws. Operators who stay ahead of these requirements will be better positioned long-term than those who react after the fact.

- Compressed entry yields. Buying a premium asset at a 4.5% cap rate requires a strong thesis on rent growth or value-add upside to hit meaningful return targets. Investors underwriting at compressed caps with optimistic rent assumptions are carrying real execution risk if market conditions shift.

- Liquidity differences from public markets. Unlike manufactured housing REITs, direct mobile home park investments and syndications are illiquid. The transaction market, while growing, is still comparatively thin — which means exits take time and are subject to buyer availability.

The Bottom Line for Investors and Operators in 2026

Private equity and institutional capital have permanently elevated manufactured housing as an asset class. That’s largely good news — it validates the fundamentals, creates deeper exit markets, and raises professional standards across the industry.

But it also means the era of acquiring well-located, stabilized mobile home parks at 7–8% cap rates in competitive markets is largely over. The opportunity has shifted toward off-market deal sourcing, value-add execution, and markets where institutional buyers aren’t yet dominant.

Operators who combine direct owner relationships, operational expertise, and disciplined underwriting will continue to find strong deals — even in an environment where large funds are actively competing. The key is not competing where institutional buyers are strongest. It’s competing where they aren’t.

For a broader look at where the best mobile home park investment markets are in 2026, see our guide: Best Markets for Mobile Home Park Investing in 2026: A State-by-State Guide.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Frequently Asked Questions

Is private equity buying mobile home parks bad for residents?

It depends heavily on the operator. Some institutional buyers prioritize aggressive rent increases over community investment, which can pressure residents. Responsible operators — institutional or otherwise — invest in infrastructure, maintain transparent communication, and uphold community standards. Regulatory trends in many states are also establishing minimum protections for residents regardless of ownership type.

Can smaller investors still compete with private equity for mobile home park deals?

Yes — but the strategy matters. Smaller operators and regional investors have real advantages in speed, flexibility, off-market access, and value-add execution. Competing head-to-head for the same brokered, stabilized assets that institutional buyers target is increasingly difficult. Focusing on direct owner relationships, smaller markets, and value-add opportunities is where independent operators continue to find strong returns.

How has private equity affected mobile home park cap rates?

Cap rates for premium manufactured housing communities have compressed from roughly 5.5–6.5% a decade ago to 4.0–5.0% in 2026. Stabilized assets trade in the 5–7% range, while value-add opportunities with execution risk still trade at 7–9.5%. The compression has been most pronounced in Sun Belt markets with strong population and rent growth.

What drove the increase in mobile home park transaction volume in 2025?

Several factors converged: institutional recognition of manufactured housing fundamentals (low supply, high occupancy, rising lot rents), cap rate compression attracting sellers who can now exit at strong valuations, and aging park owners reaching natural exit points. The 47.1% jump in 2025 also reflected pent-up demand from the slower 2023 acquisition market as well as genuine structural interest from private equity allocators.

Should passive investors worry about private equity crowding out returns?

For passive investors in mobile home park syndications, institutional presence is a double-edged sword. It creates strong exit optionality — institutional buyers represent a deep pool of potential acquirers at sale. However, it also means entry prices are higher, which requires stronger operational execution to hit return targets. Evaluating a GP’s ability to source deals off-market and execute value-add business plans is more important than ever when underwriting a passive investment.

Get the top 20 lessons from two decades of mobile home park investing — free.