For years, mobile home park investing had a reputation as one of the least regulated real estate asset classes. Lot rents weren’t subject to rent control. Right-of-first-refusal laws were rare. Eviction rules were manageable. You could underwrite deals on 6–8% annual rent growth, value the land, and sleep well.

That era is ending.

In the past 18 months, a wave of state legislation has reshaped the mobile home park investing landscape — and not all investors have updated their underwriting models to account for it. If you’re still stress-testing deals the way you did in 2022, you’re carrying regulatory risk you’re not pricing for.

Here’s what’s actually happening, state by state, and what it means for your next deal.

The States That Moved First

Washington state fired the first shot. House Bill 1217, signed into law and effective May 7, 2025, caps annual lot rent increases at 5% for all manufactured home communities. Park owners cannot raise rents in the first 12 months of a new tenancy and must provide three months of written notice before any increase.

For investors who had been underwriting Washington deals at 6–8% annual rent growth — the prevailing assumption for value-add parks — this was a deal-breaker. Overnight, deals that worked at $3M didn’t work at $2.6M. Buyers under LOI had to renegotiate or walk.

New Jersey followed in early 2026. A law effective March 1, 2026 caps mobile home park lot rent increases at 3.5% per year. Any increase above that requires approval from the state Department of Community Affairs, with the owner demonstrating that current income is insufficient to cover operating costs.

California is, as usual, a legislative pile-on. AB 1543 (introduced 2026) would cap all California mobile home park lot rents at the lower of 5% or CPI+3%. SB 1092 expands right-of-first-refusal laws. AB 768 adds additional rent protections. California investors have been navigating local rent control for years — but a statewide cap would be a different magnitude of constraint entirely.

Florida: The Surprise Move

Florida has historically been one of the most investor-friendly states in the country. No income tax, landlord-friendly courts, strong population growth, limited rent control history. Mobile home park investors treated Florida as a safe harbor while the coasts went sideways.

SB 1550 and HB 703, targeted for July 1, 2026, would change that calculus significantly. If passed, these bills would:

- Require park owners to provide detailed written justification — including actual invoices and supporting evidence — for any rent increase

- Double the grace period for late rent payments to 10 days

- Prohibit electronic payments as the sole payment method

- Increase state relocation compensation for displaced residents to $11,500+ for multi-section homes

The invoice requirement is the one rattling operators. It effectively creates a quasi-regulatory hearing process for routine rent increases. The operational overhead of documenting every utility cost increase, insurance premium, and maintenance expense as justification for a $25/month rent bump is not trivial.

The Right-of-First-Refusal Creep

Twelve states now have Right of First Refusal (ROFR) laws for manufactured home communities. These laws require park owners to notify residents — or a qualified nonprofit or resident organization — before accepting any offer to sell, giving them an opportunity to match the price.

In practice, residents almost never exercise ROFR. They rarely have the capital or organizational capacity to close a purchase. But the law still adds 30–60 days to the acquisition timeline, creates uncertainty that makes sellers nervous, and in some states triggers additional notice and documentation requirements.

For investors doing direct-to-owner acquisitions from long-term “mom and pop” owners, ROFR can be a significant deal-killer. A 70-year-old owner who wants to close quietly in 45 days doesn’t want to notify a resident committee and wait. Some deals fall apart entirely because sellers won’t go through the process.

What This Means for Your Underwriting

If you’re acquiring mobile home park deals in 2026, your underwriting model needs to account for regulatory risk in a way it probably didn’t two years ago. Here’s a framework worth building into every deal:

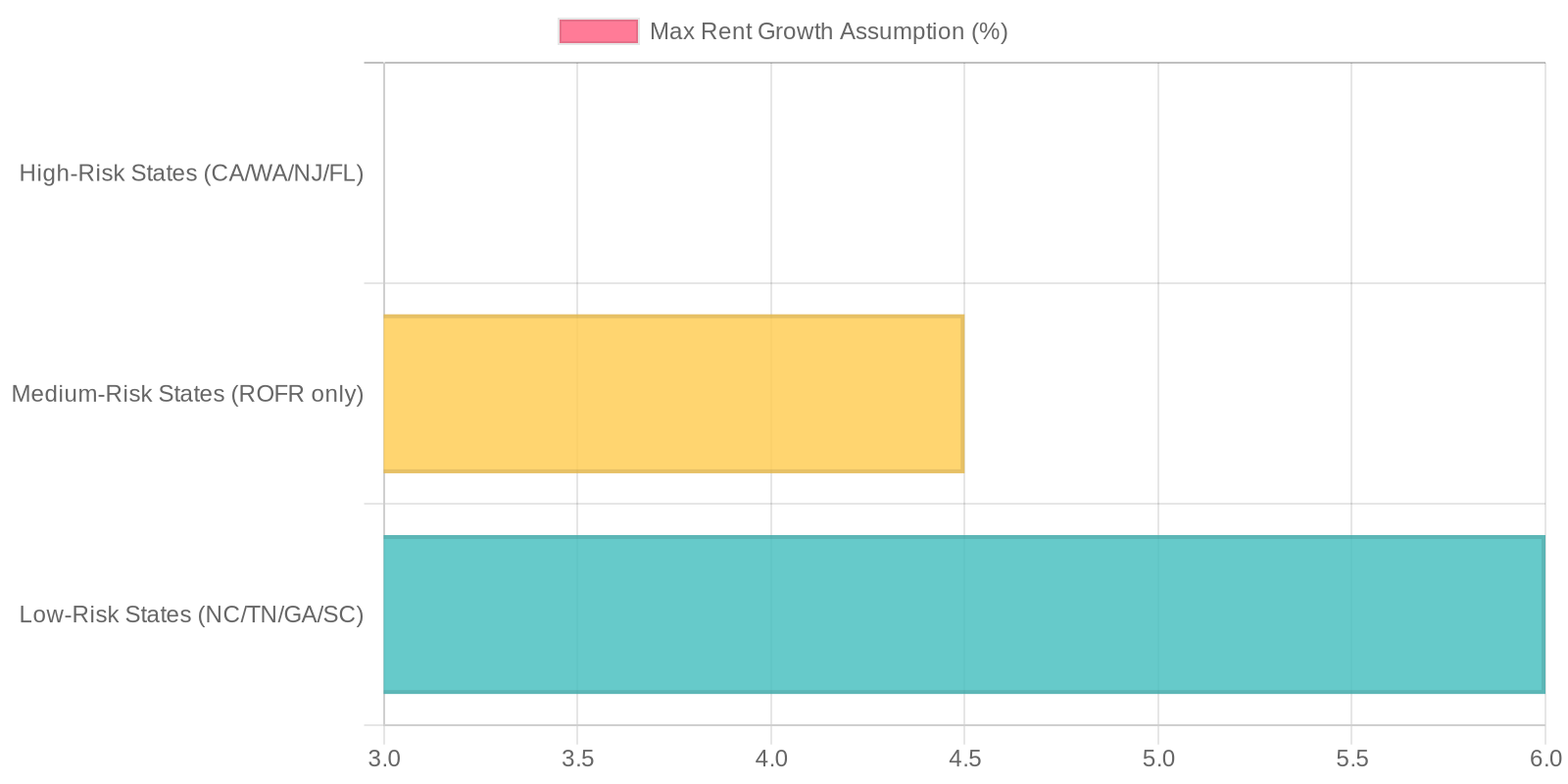

- Low regulatory risk states (no rent control, no ROFR, no active legislation): Underwrite at market rent growth, typically 5–7% annually depending on submarket

- Medium regulatory risk states (ROFR laws present, no rent caps): Underwrite at 4–5%, add 30–60 days to deal timeline

- High regulatory risk states (active rent cap legislation or existing rent control): Underwrite at 3% max. Run a stress test at 2% and make sure the deal still works.

Regulatory risk isn’t binary — it’s a spectrum. A bill that’s been introduced in a state legislature isn’t the same as a bill that’s passed. But in states where advocacy groups are active and the political climate is moving against landlords, you want to stress-test early, not after you’ve closed.

This regulatory risk assessment is one of the due diligence layers we walk through in the Keel Team Due Diligence Playbook — alongside infrastructure, utility systems, and occupancy verification — because it directly affects long-term hold value.

The Southeast Advantage — and Its Limits

As of early 2026, North Carolina, Tennessee, Georgia, and South Carolina have no statewide ROFR requirements and no active rent control legislation targeting manufactured home communities. That’s not a coincidence — it’s a competitive moat, and it’s one of the primary reasons we concentrate acquisitions in these markets.

The combination of favorable landlord law, strong population growth, and affordable housing demand makes the Southeast the clearest value-add opportunity in the country right now. Investors who’ve been burned by California rent control or Washington’s new caps are actively relocating capital here.

That capital migration creates two dynamics:

- More sophisticated competition for the best deals in NC and TN — so source off-market or get outbid

- Better exit multiples when you’re ready to sell, because buyer demand is increasing

But here’s what doesn’t get said enough: the window isn’t permanent. Advocacy groups are actively lobbying NC and TN legislatures. Legislative sessions happen every year. The parks I’d be most concerned about buying today are the ones that only work at 7%+ annual rent growth in states with active tenant advocacy movements.

The Bottom Line

Regulatory risk is now a first-class underwriting variable in mobile home park investing. It’s no longer sufficient to look at rent rolls, infrastructure condition, and location. You need to know what’s happening in the statehouse.

Map your target markets against the regulatory landscape. Stress-test your rent growth assumptions. And if you’re finding that deals in highly regulated states aren’t penciling out anymore — you’re not doing the math wrong. The math is telling you something real.

Stick to markets where the rules favor long-term investors. Right now, that increasingly means the Southeast.

Keel Team focuses on acquiring mobile home parks in North Carolina, Tennessee, and select Southeast markets. We publish research and analysis on the manufactured housing space to help investors make better decisions.