Vetting a mobile home park syndicator is one of the most important steps a passive investor can take — yet most people don’t know where to start. The deal deck looks polished, the projected returns are attractive, and the operator has a professional website. But none of that tells you whether the person running the deal actually knows what they’re doing.

The right questions, asked before you write a check, can save you from a painful outcome and point you toward operators who genuinely know how to create value in mobile home parks.

This guide covers 15 questions every passive investor should ask a mobile home park syndicator — and what strong answers look like.

Why Vetting a Mobile Home Park Syndicator Matters

In a mobile home park syndication, you’re betting on the operator as much as the asset. The same physical park can generate excellent returns in the hands of an experienced operator and lose money under someone who’s learning on the job.

Unlike direct real estate investing, limited partners in a syndication have no active control. You wire funds, sign the subscription agreement, and wait for quarterly distributions. Your outcome is almost entirely dependent on the judgment, integrity, and capabilities of the general partner.

That’s why operator due diligence is non-negotiable. The questions below are designed to separate experienced operators from novices — and honest sponsors from those who overpromise.

Questions About Track Record and Experience

1. How many mobile home parks have you taken full cycle?

“Full cycle” means the sponsor bought, operated, and sold a property — not just acquired it. Anyone can claim industry experience. The real question is whether they’ve completed deals from acquisition through exit. Look for at least one or two full-cycle transactions before entrusting someone with a meaningful capital commitment.

2. What’s your worst deal — and what happened?

Every experienced operator has a deal that didn’t go as planned. A syndicator who claims a flawless track record either hasn’t done many deals or isn’t being candid. Listen for honest reflection, specific lessons learned, and evidence that they adjusted their process as a result. This question tells you more about character than any pitch deck slide.

3. How many lots are currently under management?

Scale matters in mobile home park investing. An operator managing 500+ lots across multiple parks has built processes, staff, and vendor relationships that a first-timer hasn’t. Ask how many lots they currently manage and how that has grown over time. Growth trajectory matters as much as current scale.

4. Do you operate the parks yourself or use third-party management?

Some operators outsource park management to third-party companies. This isn’t inherently wrong, but it creates an additional layer between you and your investment. Self-managed parks — where the operator directly controls hiring, maintenance, and rent collection — tend to offer tighter oversight and faster problem resolution.

Questions About the Specific Deal

5. Walk me through the business plan in plain language.

Return projections in a pitch deck are easy to generate. The business plan — what the operator will actually do to create value — is what matters. Is the strategy to raise rents to market rates? Fill vacant lots? Convert park-owned homes to tenant-owned? Every mobile home park deal should have a specific, actionable value-add thesis, not just a passive hold.

6. What does the downside scenario look like?

Strong operators stress-test their own deals. Ask what happens if occupancy drops 10%, if rent increases stall, or if exit cap rates expand. If the answer is “we’ve modeled it and returns would be X under those conditions,” that’s a good sign. If the sponsor pivots immediately back to the upside case, that’s a red flag.

7. What’s the current occupancy rate, and why are lots vacant?

Vacant lots are both the biggest risk and the biggest opportunity in mobile home park investing. Ask for the current occupancy figure and a direct explanation of why those lots are empty — and specifically how the operator plans to fill them. Vague answers here deserve more scrutiny.

8. What’s the infrastructure situation?

Water and sewer infrastructure is one of the most common sources of surprise costs in mobile home parks. Ask whether the park is on city water and city sewer, or on a private well or septic system. If it’s on private infrastructure, ask when it was last inspected and what the deferred maintenance estimates are. Experienced operators will have clear, documented answers.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

Questions About the Legal Structure and Fees

9. What are all the fees in this deal?

Mobile home park syndications typically involve multiple fee layers — acquisition fees, asset management fees, disposition fees, and sometimes refinancing fees. These aren’t inherently problematic, but you should understand every one of them before committing capital. Ask for a complete fee schedule and calculate what percentage of total equity those fees represent. For a detailed breakdown, see our guide to mobile home park syndication fees and sponsor compensation.

10. What is the preferred return, and how is it structured?

A preferred return is the minimum annualized return limited partners receive before the general partner takes any profit split. Common structures are 6–8% preferred, with 70/30 or 80/20 splits above that threshold. Ask whether the preferred return is cumulative (unpaid amounts carry forward) or non-cumulative — the difference matters significantly in underperforming scenarios. If you’re unfamiliar with how preferred returns work, our explainer on preferred returns in real estate syndication covers the mechanics in detail.

11. How much is the GP co-investing?

Operators who put their own capital into the deals they sponsor have skin in the game. Ask what percentage of the equity the general partner is contributing personally. Even a modest co-invest signals alignment with LP outcomes. An operator who raises all limited partner capital and contributes nothing of their own is structurally misaligned — they collect fees regardless of performance.

Questions About Communication and Reporting

12. How often will I receive updates, and in what format?

Strong operators report quarterly at a minimum — typically a written narrative plus financial statements. Best-in-class sponsors provide investor portals where limited partners can access documents, distribution history, and deal performance data at any time. Ask to see an example investor update from a prior deal. A detailed, data-rich example is a strong signal. A vague answer about “regular communication” is not.

13. How has actual performance compared to projections on past deals?

Every deal has projections. What separates experienced operators is how their actual results compare to those projections over time. Ask for a summary of past deals showing projected versus delivered returns. Be skeptical of operators who can’t produce this comparison or who attribute every variance to external market factors outside their control.

Questions About the Exit

14. What’s your target hold period, and what triggers an early sale?

Most mobile home park syndications target hold periods of 5–7 years, though this varies based on business plan and market conditions. Ask what the specific exit strategy is — sale to an institutional buyer, a 1031 exchange, or a long-term hold with refinancing. Also ask under what circumstances they would consider selling early. How the general partner thinks about exits reveals their priorities and flexibility.

15. Can I speak with a current or former LP from one of your deals?

References matter. Any operator running a legitimate syndication should be willing to connect you with limited partners from prior deals. If you get pushback on this request, treat it as a meaningful red flag. A brief conversation with a previous investor can validate — or undermine — everything else you’ve heard in the pitch process.

Red Flags to Watch For

Experienced, honest operators give answers that are specific, direct, and acknowledge both successes and failures. They’ve told their story many times and can speak to it confidently without overselling.

Be cautious of operators who:

- Deflect difficult questions or pivot immediately back to return projections

- Can’t point to a single deal that underperformed expectations

- Present deal structures that are difficult to explain simply

- Resist providing references or documentation of past performance

- Project unrealistically high returns without a clear driver behind them

For more on identifying warning signs before you invest, see our detailed post on mobile home park syndication red flags.

How to Use These Questions Effectively

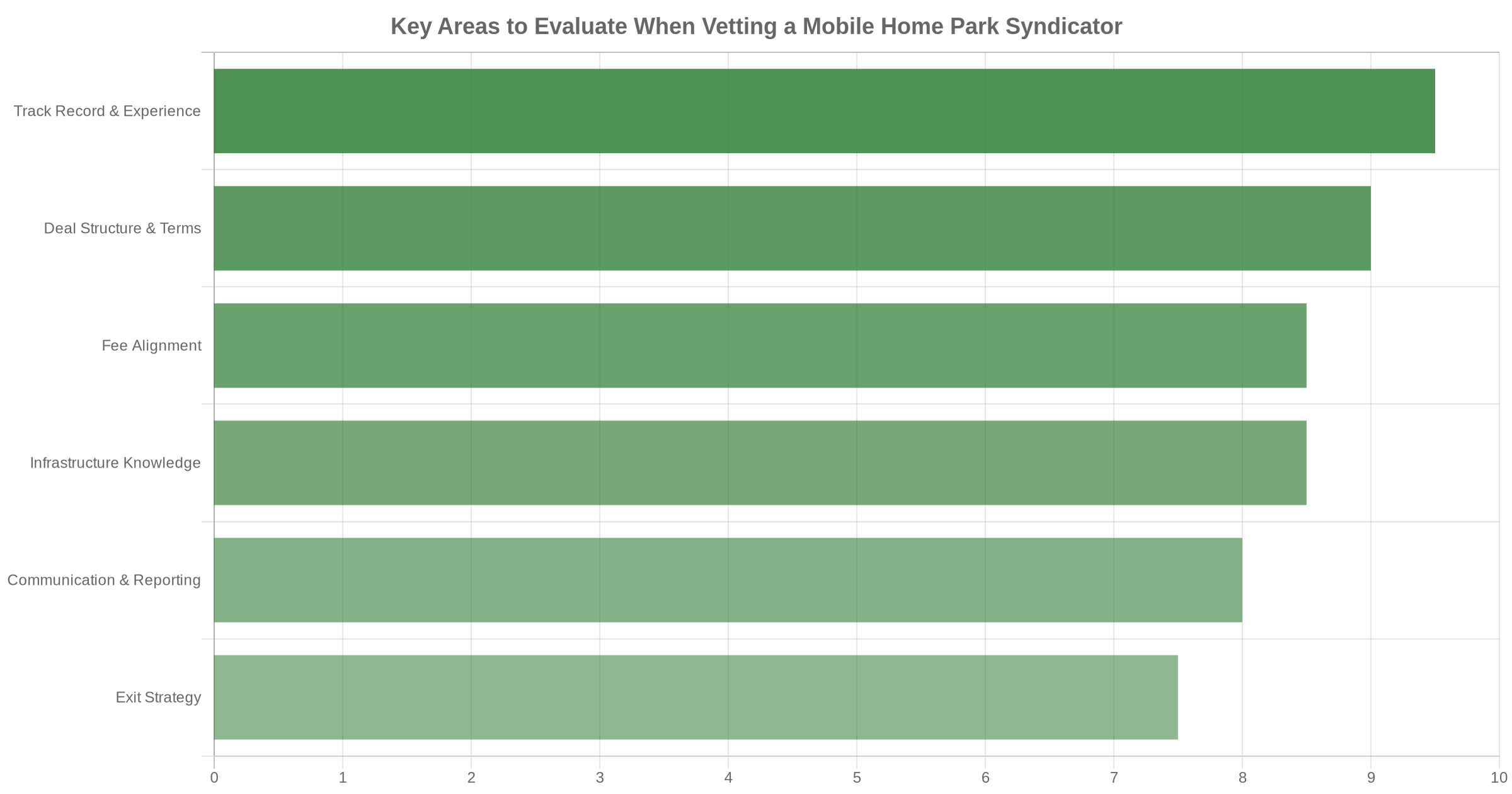

Questions are only useful if you know what to do with the answers. After your conversation, take structured notes and score each area: track record, deal structure, fee alignment, communication quality, and exit strategy. If you’re evaluating multiple deals simultaneously, compare your notes side by side.

The best mobile home park syndicators welcome rigorous due diligence. They’ve built their track record one LP relationship at a time and understand that informed investors become long-term repeat investors. If a syndicator seems bothered by your questions, that tells you something important.

If you’re still building your foundational knowledge of how these deals are structured, our overview of mobile home park syndications is a good place to start before your first conversation with a sponsor.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.