When mobile home park investors talk about infill, their eyes light up. And it makes sense — filling a vacant lot is pure math. Add $400/month in lot rent, multiply by 12, divide by a cap rate, and you’ve created $40,000+ in equity on a single lot. Do that 20 times and you’ve built a multi-million dollar value-add.

The pitch is beautiful. The execution is where things fall apart.

Investors who bought mobile home parks specifically for the infill upside are often sitting on vacant lots 12, 18, even 24 months later — still bleeding cash, still trying to figure out why their “easy” value-add isn’t materializing. Here’s the real story about why infill is the hardest easy thing in manufactured housing.

The Numbers Don’t Lie — But They Don’t Help Either

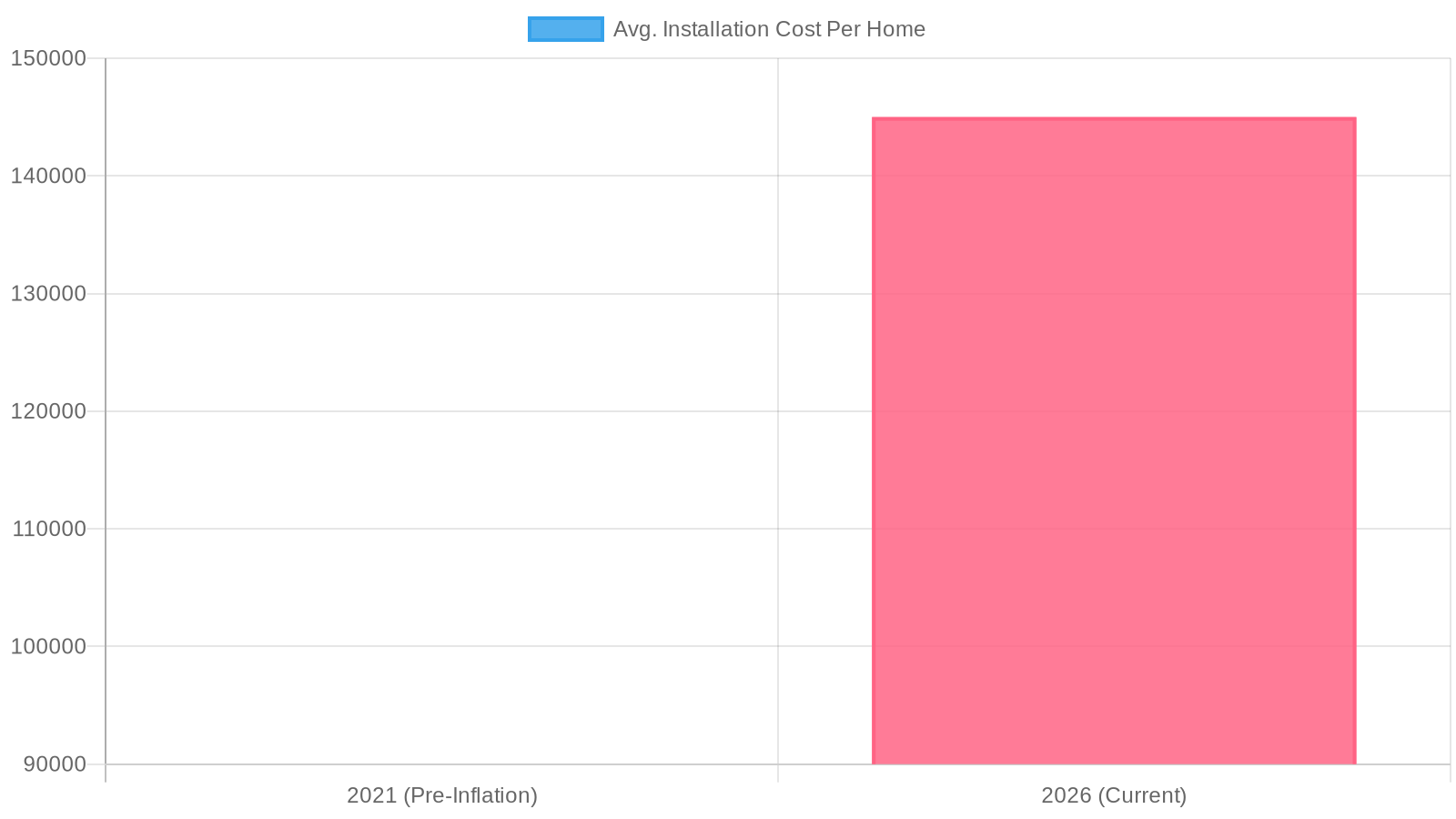

Let’s start with the home cost problem. In 2021, you could install a new single-wide manufactured home for $80,000–$95,000 all-in. Transport, setup, permits, utility connections — you might clear $100K on a bad day.

In 2026? You’re looking at $130,000–$160,000 per unit, minimum. Some markets are pushing $170K with labor and permitting. The homes cost more, the labor costs more, the permits take longer, and the utility connections at older parks often require infrastructure upgrades just to support the new load.

That capital outlay changes everything. You’re not talking about cheap infill anymore. You’re talking about deploying $2–3 million to fill 20 vacant lots — before a single dollar in new lot rent comes in.

The Financing Wall That Nobody Talks About

Here’s the thing that kills most infill programs: residents can’t get affordable home financing.

Understanding the difference between lot rent vs. park-owned homes matters here. About 76% of manufactured homes in the US are titled as chattel — personal property, like a car — rather than real estate. That classification means buyers can’t access conventional mortgages through Fannie Mae or Freddie Mac. Instead, they’re stuck with “chattel loans” from a handful of specialized lenders.

Chattel loan terms in 2026:

- Interest rates: 7–10%+

- Shorter amortization periods (15–20 years vs. 30)

- Stricter credit requirements

- Geographic restrictions — many lenders won’t touch small towns or rural markets

- Slow underwriting: 4–8 weeks minimum

A resident who could comfortably qualify for a $200K conventional mortgage often can’t get a $95K chattel loan approved. The math just doesn’t work for them. And if they can’t finance the home, you can’t fill the lot.

The Timeline Problem Is Real

Even when financing works, infill takes time — a lot of it. A typical infill timeline (best case) looks like this:

- Purchase agreement with a manufactured home dealer: 2–4 weeks

- Lender approval for the resident’s home financing: 4–8 weeks

- Home production and delivery scheduling: 6–12 weeks

- Site prep and utility connections: 2–4 weeks

- Setup, skirting, stairs, final inspection: 2–3 weeks

Add it up and you’re looking at 4–6 months per lot under ideal conditions. Hit any snag — a permit delay, a lender rejection, a supply chain hiccup — and you’re at 8–14 months. Meanwhile, those vacant lots are paying property taxes and contributing zero to your NOI.

What Actually Works: Strategies Operators Use to Break Through

The operators who succeed at infill aren’t waiting for the financing market to fix itself. They’re building systems around the problem.

Rent-to-Own Programs

The most effective infill strategy is bringing homes into the park on a park-owned basis, then placing residents on lease-option terms. The resident pays a combined lot-rent-plus-home-payment — say $850/month total — and earns the right to purchase the home after 24–36 months at a predetermined price.

This bypasses the chattel loan problem on day one, fills the lot in 60–90 days instead of 6+ months, and creates a resident who’s highly motivated to maintain the home because they’re working toward ownership. Yes, it ties up capital — but it’s capital that generates income, and the resident eventually buys the home off your balance sheet.

Dealer Partnerships

Don’t source homes on the open market. Build a direct relationship with a regional manufactured home retailer — Clayton Homes, Palm Harbor, or a strong regional dealer — and structure an exclusive or preferred arrangement. Better pricing through volume. Priority delivery scheduling. Pre-screened home options that fit your specific lot sizes and utility configurations. The best park operators have a dealer on speed dial. The struggling ones are starting from scratch with every lot.

Financing Concierge Service

If you’re going to rely on resident-financed infill, you need to become the expert in getting your residents financed — or hire someone who is. Rather than sending residents to one lender, use a shotgun approach: simultaneously submit to 5–6 chattel lenders (21st Mortgage, Triad Financial, Cascade, Credit Human, CommunityWest) and take the best offer. Add a $500–$1,000 referral bonus for existing residents who bring in qualified new neighbors.

Know What You’re Buying Before You Close

One of the most important things you can do before acquiring a mobile home park with vacant lots is understand why those lots are vacant. Sometimes it’s a financing problem. Sometimes it’s infrastructure — no utility hookups, undersized water lines. Sometimes the lots are physically unsuitable for installation. Sometimes the park’s local lending reputation is already damaged with chattel lenders.

A thorough due diligence process surfaces these issues before you close, not after. If you’re building your acquisition checklist, the Keel Team Due Diligence Playbook walks through the key inspection and underwriting questions used on every deal — including an infill feasibility assessment.

Infill Is Still the Best Play — If You Do It Right

None of this is meant to talk you out of infill. Filling vacant lots is still one of the most powerful value-creation levers in mobile home park investing. The parks that create the most equity over time are almost always the ones that executed a disciplined infill program.

But “disciplined” is the key word. You need a real plan, realistic timelines, multiple financing pathways, and enough capital cushion to absorb the lag between investment and income. The investors who think infill is passive get humbled quickly. The investors who treat it like a full operational program — with systems, partnerships, and patience — create real wealth.

Know what you’re getting into. Build your systems before you close. And don’t underestimate the financing wall — it’s real, it’s frustrating, and the operators who solve it outperform everyone else.

Keel Team acquires and operates mobile home parks across the Southeast and Midwest. We share what’s actually working in value-add manufactured housing — not the highlight reel.