The terms “mobile home” and “manufactured home” are used interchangeably by most people — including many real estate professionals. But if you’re investing in manufactured housing communities, that distinction isn’t just semantics. It affects how homes are financed, insured, and valued, and it shapes every due diligence conversation you’ll have before closing a deal.

Here’s what every mobile home park investor needs to know.

The Dividing Line: June 15, 1976

The difference between a “mobile home” and a “manufactured home” comes down to a single date: June 15, 1976.

That’s when the U.S. Department of Housing and Urban Development (HUD) enacted the National Manufactured Housing Construction and Safety Standards Act. Before that date, factory-built homes had no national construction standard — they were built to a patchwork of local codes, or no codes at all. After June 15, 1976, every factory-built home had to meet HUD’s federal construction and safety code to be sold in the United States.

The result:

- Mobile home: A factory-built home constructed before June 15, 1976 (no HUD code)

- Manufactured home: A factory-built home constructed on or after June 15, 1976 under the HUD code

In everyday conversation, people still call everything a “mobile home” — and that’s fine. But in the lending, insurance, and investing world, this pre/post-1976 distinction has real financial consequences.

What the HUD Code Actually Changed

Prior to 1976, factory-built housing quality varied widely. Some manufacturers built solid homes; others cut corners with no accountability. The HUD code standardized:

- Structural load requirements — wind, snow, and roof loads calibrated by geographic climate zone

- Thermal and fire safety standards

- Electrical, plumbing, and HVAC systems

- A permanent HUD data plate on each unit certifying compliance with federal standards

Every manufactured home built after 1976 carries a HUD certification label — a small aluminum plate (roughly 2” × 4”) attached to the exterior, typically near an entry door or rear corner. This label shows a certification number and the state in which the home was manufactured.

If you’re walking a park during due diligence and a home doesn’t have this label, it was built before June 1976 — and it’s classified as a mobile home under federal law, with all the financing and insurance complications that come with it.

How This Distinction Affects Mobile Home Park Investors

Whether you’re acquiring a park directly or investing as a limited partner, the pre-1976 vs. post-1976 breakdown in a park’s home inventory matters across three key areas:

1. Financing Eligibility

Most agency lenders — Fannie Mae, Freddie Mac, and FHA-backed programs — require that a park’s home inventory be predominantly HUD-compliant manufactured homes. Parks with a significant percentage of pre-1976 units may be ineligible for agency debt entirely, pushing operators toward community bank loans or seller financing. Both typically carry higher interest rates and shorter amortization schedules, which directly affects your cash-on-cash returns.

As a practical rule: ask your lender what their pre-1976 home percentage threshold is before you spend time underwriting a deal. A park with 25–30% pre-1976 units is a fundamentally different financing conversation than one with all post-1976 inventory. For a comprehensive look at how lender requirements break down by deal type, see: Mobile Home Park Financing Options in 2026: A Guide to Agency Debt, Community Banks, and Seller Financing.

2. Property Valuation

In most mobile home park valuations, you’re primarily paying for the land and infrastructure — the homes themselves contribute relatively little to total property value. But home age and condition still affects your deal in tangible ways:

- Occupancy potential: Older units are harder to re-rent after vacancies and expensive to replace

- Operating costs: Pre-1976 homes carry higher ongoing maintenance costs — aging electrical panels, failing plumbing, inadequate insulation

- Lot rent potential: Newer manufactured homes support higher lot rents in most markets, which affects your stabilized NOI

3. Insurance Costs and Coverage

Pre-1976 mobile homes are underwritten differently by insurance carriers. Some carriers won’t insure them at all; others will at higher premiums or with significant coverage exclusions. If your park includes any park-owned homes (rather than operating purely as a land-lease community), the age of those homes directly impacts your insurance costs and coverage terms.

📋 The MHP Due Diligence Playbook — 10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — including how to assess home vintage, financing risk, and infill opportunity.

Two decades of hard-won lessons distilled into one free guide. Whether you’re evaluating your first deal or your fiftieth, these insights will sharpen your approach.

A Quick Reference: Factory-Built Housing Terminology

The vocabulary in manufactured housing can get confusing quickly. Here’s a breakdown of the terms you’ll encounter:

- Mobile home: Pre-June 15, 1976 factory-built home — no HUD code, harder to finance

- Manufactured home: Post-June 15, 1976 factory-built home — HUD certified, eligible for agency financing programs

- Modular home: Factory-built but installed on a permanent foundation; classified as real property, subject to local building codes (not the HUD code)

- Site-built home: Conventional stick-framed construction; not relevant to mobile home park investing

A common point of confusion: modular homes are often lumped in with manufactured homes, but they’re structurally different. Modular homes sit on permanent foundations, are classified as real property, and follow local codes — just like a site-built house. Manufactured homes sit on a steel chassis and are classified as personal property unless the owner formally converts them through a “titling out” process.

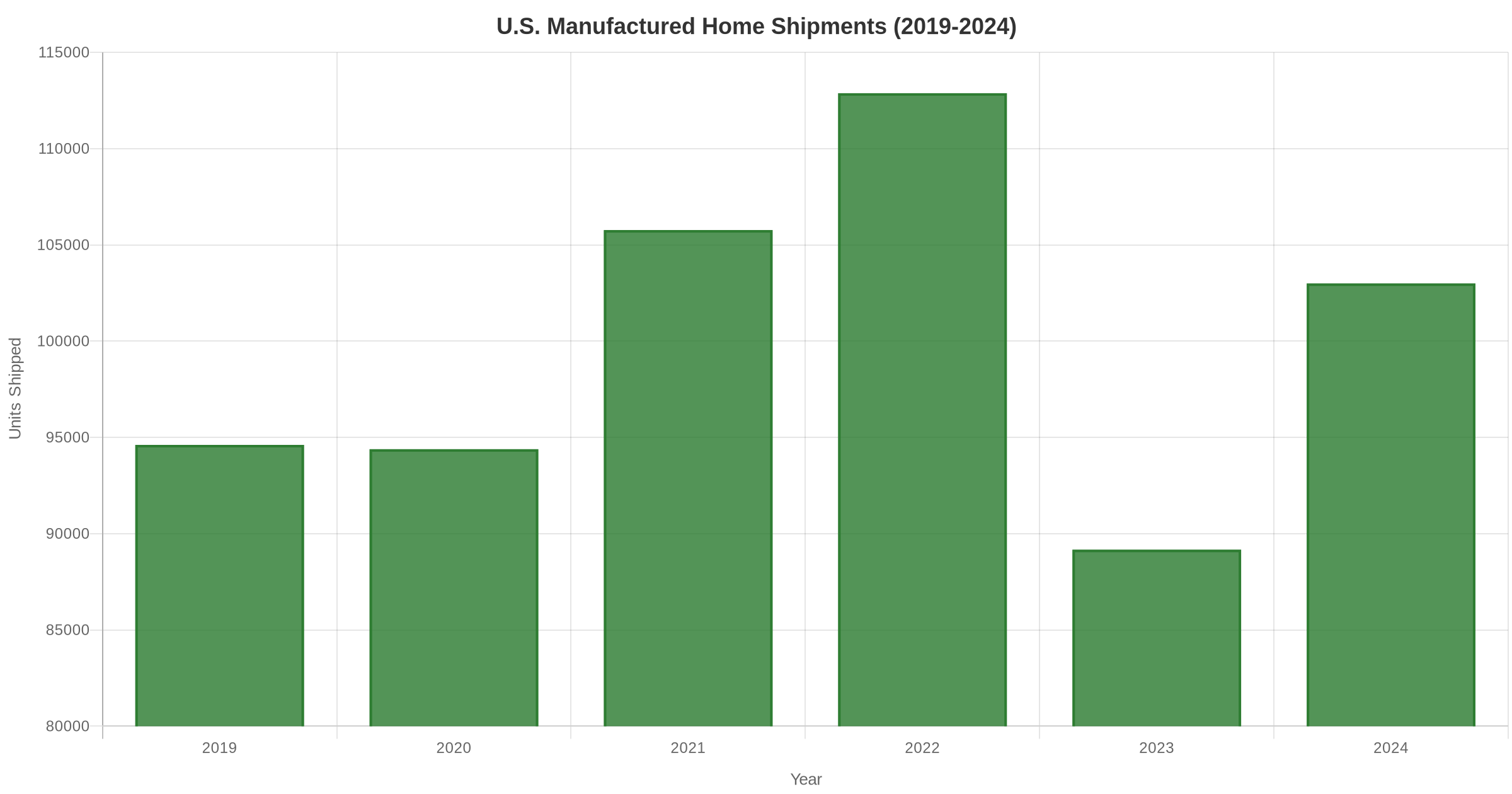

2026 Manufactured Housing Demand: What the Numbers Show

Manufactured housing production rebounded strongly in 2024 after a pullback in 2023. According to data from the Manufactured Housing Institute (MHI) and U.S. Census Bureau, approximately 103,000 manufactured homes were shipped in 2024 — up roughly 15% from the 89,169 units shipped in 2023.

What’s driving the rebound:

- Affordability pressure: Average new site-built home prices exceeded $400,000 in 2024. Manufactured homes average $120,000–$160,000 — less than half the cost

- Rental housing shortage: Manufactured housing communities fill an affordability gap that conventional apartment construction can’t address at this price point

- Institutional validation: Major REITs including Sun Communities and Equity LifeStyle Properties have continued expanding their manufactured housing portfolios, adding credibility and liquidity to the asset class

More than 20 million Americans currently spend over 30% of their income on housing costs. Manufactured housing remains one of the few viable paths to affordable homeownership and stable rental housing at scale. To understand what this structural demand means for investment returns, see: Affordable Housing Demand and What It Means for Mobile Home Park Investors.

What to Check During a Mobile Home Park Acquisition

When you’re evaluating a park to acquire, here’s how to apply the mobile home vs. manufactured home distinction in practice:

- Request a lot-by-lot inventory — including home year, size (single vs. double-wide), and ownership status (park-owned vs. tenant-owned)

- Flag all pre-1976 units — calculate them as a percentage of total occupied lots

- Assess structural condition on older homes — deferred maintenance on pre-1976 homes is often significant and costly to remediate

- Confirm lender tolerance early — get your lender’s pre-1976 threshold before spending weeks underwriting a deal that won’t qualify

- Budget for infill if needed — replacing aged units with new manufactured homes typically costs $40,000–$80,000 per unit installed; this belongs in your proforma from day one

A high percentage of aged homes isn’t automatically a deal-killer. Parks with significant pre-1976 inventory can represent genuine value-add opportunities — if the infill math works and you go in clear-eyed about the financing constraints. The key is knowing exactly what you’re buying before you close.

For a complete checklist of everything to verify during due diligence, see: Mobile Home Park Due Diligence Checklist: 25 Things to Verify Before You Buy.

📋 Ready to Evaluate Your Next Deal? Get the MHP Due Diligence Playbook — the complete system for analyzing mobile home park acquisitions with confidence. 10 video modules, a 55-page master checklist, and 9 ready-to-use templates.

Frequently Asked Questions

Is it offensive to call a manufactured home a “mobile home”?

In everyday conversation, most residents and owners don’t take offense — the terms are widely interchangeable. The industry has largely shifted to “manufactured home” and “manufactured housing community” (MHC) as more accurate terminology in professional and financial contexts, but colloquially “mobile home park” remains the common shorthand.

Can you physically move a manufactured home?

Technically yes — the steel chassis makes manufactured homes transportable. In practice, moving one costs $5,000–$15,000 or more and is rarely done after initial installation. Most homes stay in place indefinitely, which is one reason tenant turnover in manufactured housing communities is dramatically lower than in apartment complexes (roughly 2% annually vs. 47% for apartments).

Are manufactured homes eligible for traditional mortgage financing?

It depends on how the home is titled. Manufactured homes installed on a permanent foundation that have been converted to real property can qualify for FHA, VA, or conventional mortgage financing. Homes on leased land within a mobile home park are typically financed through chattel loans (personal property loans), which carry higher interest rates and shorter terms than traditional mortgages.

How do I confirm a home’s HUD compliance during due diligence?

Look for the HUD certification label — a small aluminum plate (roughly 2” × 4”) attached to the exterior, usually near an entry door or rear corner. It will display a certification number and the state of manufacture. Absence of this label is a clear indicator the home predates June 1976. County records and VIN lookups on the home’s title can also verify vintage.

Does the percentage of pre-1976 homes affect a park’s cap rate?

Not as a direct line item, but yes — indirectly. Parks with high pre-1976 home percentages tend to have higher operating costs, lower lot rent potential, and constrained financing options, all of which compress NOI and affect the prices buyers are willing to pay. It’s one reason thorough home-inventory due diligence is part of every serious acquisition process. See our guide to mobile home park cap rates for more on how NOI and market conditions drive valuation.

10 video modules, a 55-page master checklist, and 9 ready-to-use templates that walk you through every step of evaluating a mobile home park deal — from the first site visit to closing day.

Get the top 20 lessons from two decades of mobile home park investing — free.