The recent surge in interest rates has definitely got everyone talking given the impact it has across most economic sectors, mobile home park investments being one of them. While the pandemic opened a unique window of opportunity for securing financing at historically low rates, interest rates have now rebounded to more typical levels. At the time of this post, the 10-year US Treasury rate has surpassed the 2.75% mark.

Beyond the obvious consequence of making debt financing more expensive, let’s explore the broader implications of rising interest rates on the overall financing landscape, and on mobile home park investments. One notable effect we’re witnessing pertains to how lenders employ the Debt Service Coverage Ratio (DSCR) to size loans for mobile home park acquisitions.

The Role of Debt Service Coverage Ratio (DSCR)

Lenders typically rely on the DSCR to ensure that the Net Operating Income (NOI), representing income after covering operating expenses; comfortably covers the annual debt service, typically by a margin of 1.25 times. In simple terms, if the annual debt service stands at $50,000, the NOI must amount to $62,500 ($50,000 x 1.25 = $62,500). A higher NOI relative to the annual debt service results in a stronger DSCR, making it more likely for a lender to greenlight the loan.

With interest rates moving from their historically low amount , lenders are factoring these higher rates into their calculations for annual debt service.

Impact of Rising Interest Rates on DSCR

In the example below, let’s investigate how these elevated rates translate into increased debt service, and ultimately affect the DSCR in a mobile home park investment.

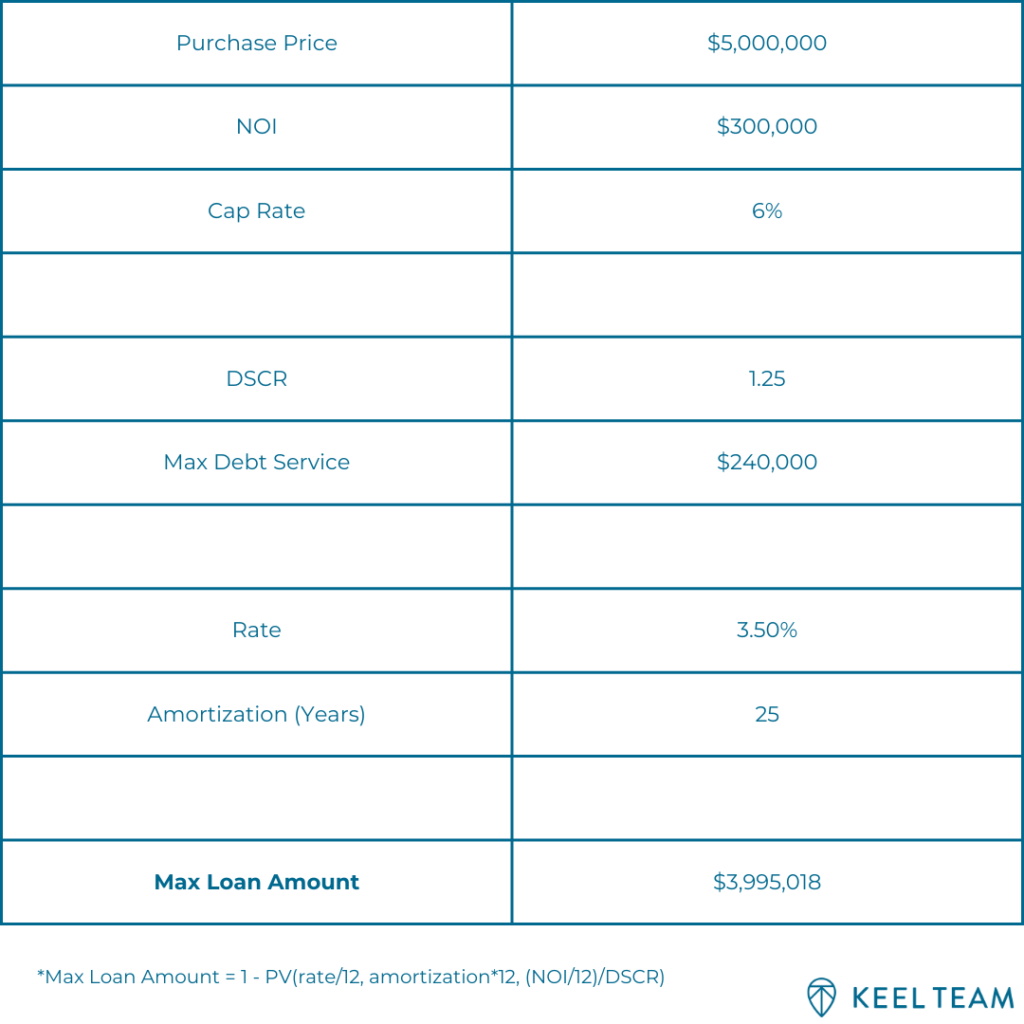

The subject property is a mobile home park with a $5,000,000 purchase price and an NOI of $300,000. This implies a capitalization rate (cap rate) of 6.00% ($300,000 / $5,000,000 = 6.00%).

Assuming a lender insists on a minimum DSCR of 1.25 times, the maximum allowable annual debt service would be $240,000 ($300,000 / 1.25x = $240,000). Lenders would then use their current interest rate and amortization to calculate the maximum loan amount.

Now, let’s rewind the clock 6-12 months ago when interest rates were substantially lower. Assuming an interest rate of 3.50% and a 25-year amortization period, with an annual debt service of $240,000- the maximum loan amount would have been $3,995,018,. This is equivalent to roughly 79.90% Loan-to-Value (LTV) based on the $5,000,000 purchase price.

Below, you’ll find a calculation in which we’ve determined the Max Loan Amount, with the formula for reference.

Decreasing Loan Amount to Maintain DSCR

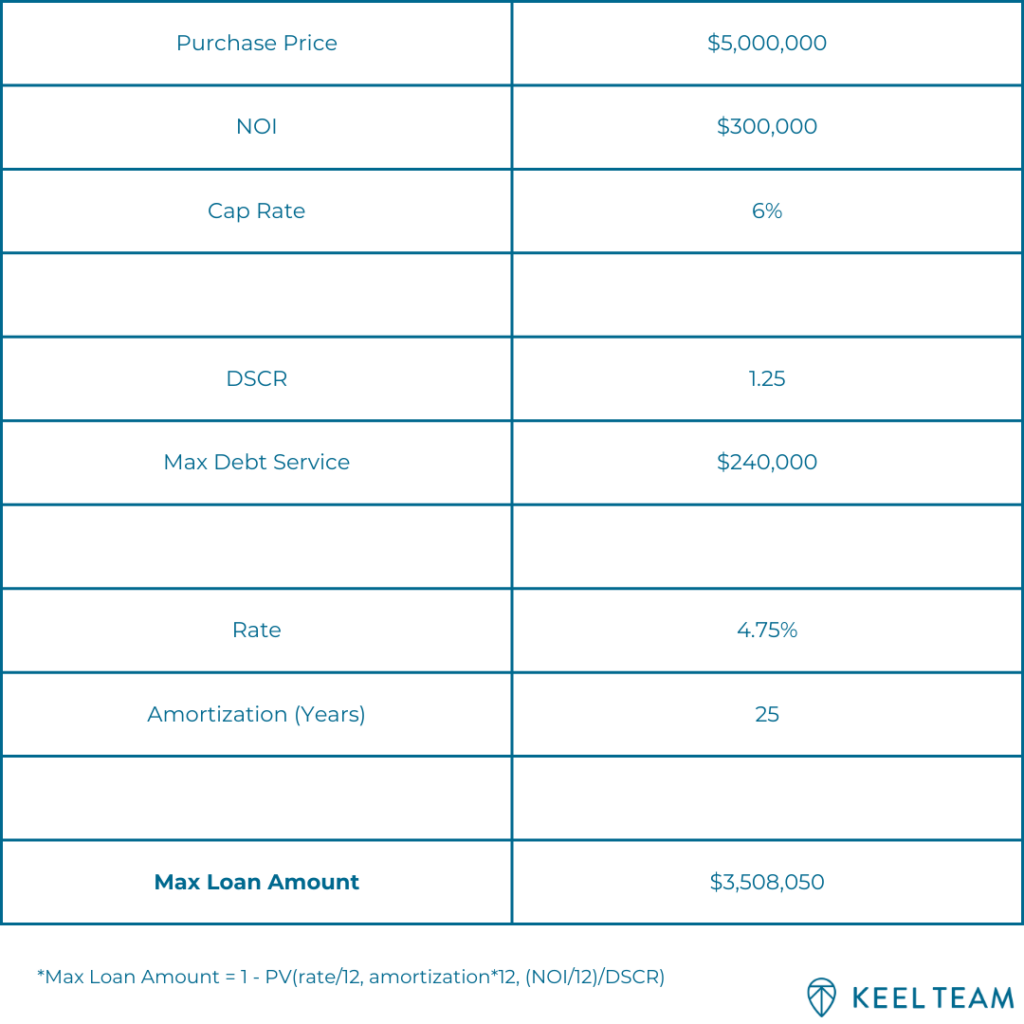

Now, if we assume today’s rates have climbed to 4.75%, while keeping all other variables constant, the annual debt service would surge to $276,413 causing our DSCR to drop from 1.25x to 1.10x, in this example.

In essence, a 1.25% increase in interest rates resulted in an annual debt service hike of $36,413, pushing our DSCR below the 1.25x threshold that most lenders require. To align with this 1.25x DSCR at the higher interest rate, lenders would need to reduce the loan amount so that the debt service drops to a level where the DSCR can once again meet the 1.25x requirement.

If we adhere to the 4.75% interest rate and keep all other factors unchanged but lower the loan amount to achieve a lower annual debt service, the maximum loan amount for the mobile home park acquisition would be $3,508,050. This allows us to maintain the $240,000 annual debt service and meet our 1.25x DSCR. This revised loan amount translates to approximately 70.16% LTV.

Wrapping Up!

In summary, by increasing the interest rate while keeping all other factors constant, the 1.25% interest rate hike (4.75% vs. 3.50%) necessitates a decrease in loan proceeds of $487,018 ($3,995,018 vs. $3,508,050) for your mobile home park investment, which accounts for nearly 10% of the total purchase price of your mobile home park.

When determining loan sizes for mobile home park investments, lenders often grapple with predicting interest rates 45-60 days into the future when the deal is set to close. Consequently, it’s not surprising if lenders are on the side of caution, leaning toward the higher end of the rate spectrum in anticipation of further interest rate increases.

As with any investment, it’s important to consult with financial and legal professionals to potentially make informed investment decisions and possibly reap the benefits of the mobile home park asset class. Stay tuned for more mobile home park investing guidelines from this blog!

Are you interested in learning more about passive mobile home park investing? Reach out to us today to explore this niche asset class and potentially reap the benefits of this historical buffer against inflation and rising costs.

Disclaimer:

The information provided is for informational purposes only and should not be considered investment advice, nor a guarantee of any kind. There are no guarantees of profitability, and all investment decisions should be made based on individual research and consultation with registered financial and legal professionals. We are not registered financial or legal professionals and do not provide personalized investment recommendations.