Something significant shifted in the mobile home park investment landscape between 2024 and 2026: state legislatures stopped treating manufactured housing communities as a footnote in broader housing policy and started targeting them specifically.

The result is a patchwork of rent control, rent stabilization, and tenant protection laws aimed squarely at manufactured housing communities — and the pace of new legislation is accelerating. If you’re underwriting mobile home park deals today with historical rent growth assumptions, you need to know exactly where you’re buying.

Why Mobile Home Parks Became a Legislative Target

The political logic is straightforward: manufactured home residents are uniquely vulnerable. They typically own their home but rent the land. Moving a manufactured home costs $5,000–15,000+ and often destroys the home’s value. So when lot rents rise significantly, residents can’t “just move” the way apartment tenants can. They’re effectively captive.

National coverage of institutional investors acquiring mobile home parks and raising rents aggressively fueled a wave of tenant organizing and media scrutiny. By 2023–2024, mobile home park reform had become a bipartisan political win — landlord restriction that even conservative legislators could back as protecting “homeowners” (the residents own their home; the frame works).

That political framing is now law in multiple states. Here’s where things stand.

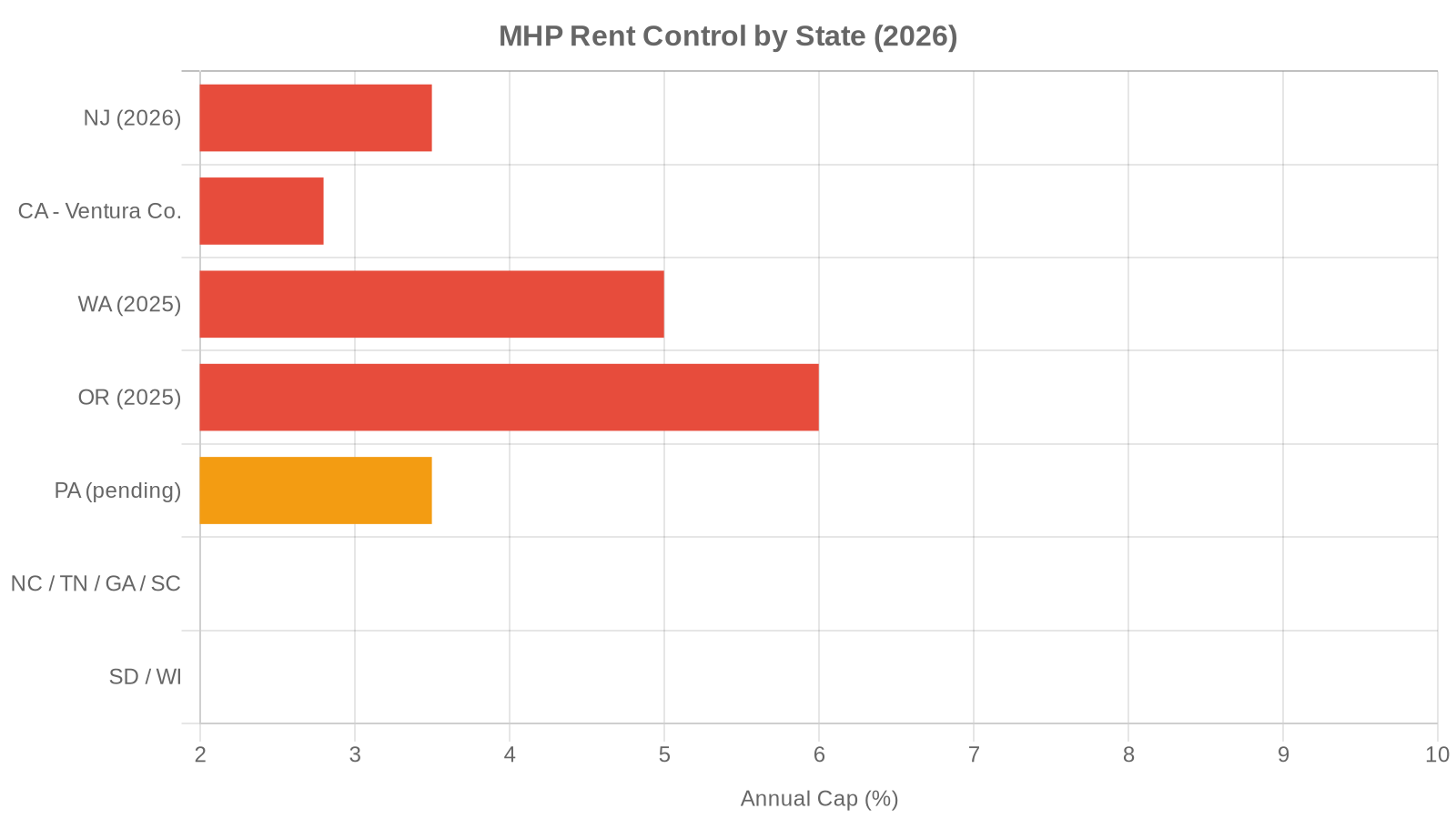

The Restricted States (Active Rent Caps as of 2026)

Washington State moved first at scale, with HB 1217 effective May 2025 capping annual lot rent increases at 5%. Additionally: no increases in the first 12 months of tenancy, and 3 months’ written notice required for any increase. If you own parks in Washington, your annual rent growth ceiling is now 5% — period, regardless of market conditions.

New Jersey went even tighter: 3.5% annual cap, effective March 1, 2026. Exceeding it requires DCA approval with documented justification. New Jersey operators who bought expecting 5–7% annual increases just had their model fundamentally repriced.

Oregon has layered restrictions — state law generally caps rent increases at 7% plus inflation or 10% (whichever is lower), and a 2025 bill targeting communities with 30+ spaces tightened that further to 6% annually.

Pennsylvania passed HB 1250 through the House in June 2025, tying increases to CPI for the Northeast with a 2–4% band. Awaiting Senate action, but with bipartisan support, likely to pass.

New York, Florida, and Michigan each have active bills at various stages that would impose new transparency requirements, right-to-purchase provisions, or justification mandates. Florida’s SB 1550, if enacted, allows courts to scrutinize increases beyond base costs — a mechanism that could functionally cap aggressive rent growth even without a stated percentage cap.

The Safe Harbors (For Now)

Here’s the good news for operators focused on the right geographies:

North Carolina, Tennessee, Georgia, South Carolina, South Dakota, and Wisconsin — none of these states have mobile home park-specific rent control legislation in effect or advancing in 2026.

Tennessee has explicitly preempted local rent control ordinances. North Carolina is broadly landlord-friendly from a regulation standpoint — though North Carolina’s Mobile Home Park Act includes tenant protection provisions that operators should understand before closing a deal there. South Dakota and Wisconsin trend politically away from property regulation. Georgia and South Carolina are similarly positioned.

This creates a real, measurable regulatory arbitrage opportunity. Operators buying in NC and TN today are acquiring assets in markets where:

- No rent cap constrains NOI growth

- No right-of-first-refusal requirements complicate exits

- No mandatory justification process delays increases

That won’t last forever. As restricted-state capital looks for new homes, it will flow toward these markets. The window is open, but it won’t be open indefinitely.

How to Protect Your Portfolio — Whether You’re in a Restricted State or Not

If you own parks in rent-controlled states:

Don’t panic, but do update your underwriting. Here’s what actually matters:

1. Model your NOI growth at the cap, not at historical trends. If you’re at 5% max, run your DCF at 5% and stress-test it at 3% (accounting for political pressure to tighten further). If the deal still works, you’re fine. If it only works at 7%+ annual growth, you have a problem.

2. Shift your value-add strategy from rent growth to expense reduction. Water submetering, renegotiating trash and maintenance contracts, filling vacant lots — these improve NOI without triggering rent cap provisions. A solid grasp of what drives mobile home park lot rent growth in your market helps identify which levers to prioritize.

3. Sell park-owned homes to tenants. Resident-owned homes reduce your management intensity, improve the community profile (which reduces regulatory scrutiny), and the sales proceeds can be reinvested in markets without restrictions.

If you’re acquiring new parks:

Make regulatory environment a first-filter screening criteria, not an afterthought. Before you run any numbers on a deal, answer: what state is this in, what does the current rent regulation landscape look like, and what’s the legislative trajectory?

A 10% higher purchase price in a regulatory-safe market is almost always better than a 10% discount in a market where your rent growth is being capped below your cost of capital. Regulatory risk should be evaluated alongside the physical and financial due diligence you’d run on any deal — our Mobile Home Park Due Diligence Playbook now includes a dedicated regulatory review checklist for exactly this reason.

The Longer Game

Rent control is a lagging indicator. It follows years of vocal tenant organizing, media coverage, and political momentum. The states where organizing is most active today — California, New York, Massachusetts, Illinois — are where the next wave of legislation will likely land. The states where that organizing is weakest — the Southeast, Plains states, mountain West outside of Colorado — are where the regulatory environment will stay favorable longest.

This isn’t a statement about whether mobile home park rent control is good or bad policy. It’s an observation about where the risk concentrates — and a case for investing in geographies where that risk doesn’t exist today.

At Keel Team, our acquisition strategy has been deliberately focused on the Southeast and Southeast-adjacent markets for years, partly because of operational economics and partly because we’ve watched the regulatory environment in other regions become increasingly inhospitable to the kind of patient, value-add investing we do.

The geography choice is, itself, part of the underwriting.

Andrew Keel is the founder of Keel Team Real Estate Investments. Keel Team acquires mobile home parks in the Southeast and Midwest, focusing on city-utilities communities with genuine value-add potential. Learn more at keelteam.com.